The Odd Selloff in Visa (V): A Notable Drop That Defies Its Stable Uptrend

Pct Price Change: -2.15%

- https://finance.yahoo.com/quote/V/

- www.marketbeat.com/instant-alerts/filing-hf-advisory-group-llc-buys-2833-shares-of-visa-inc-v-2026-08-09/

- www.zacks.com/stock/news/2971107/wall-street-raises-visa-outlook-after-strong-q3-buy-hold-or-sell

- www.marketbeat.com/instant-alerts/filing-legacy-wealth-management-llc-ms-reduces-holdings-in-visa-inc-v-2026-08-09/

- www.marketbeat.com/instant-alerts/filing-goalvest-advisory-llc-has-304-million-stock-holdings-in-visa-inc-v-2026-08-09/

- www.marketbeat.com/instant-alerts/filing-cardano-risk-management-bv-raises-position-in-visa-inc-v-2026-08-09/

- seekingalpha.com/news/4629666-key-deals-this-week-bending-spoons-advanced-micro-devices-visa-prologis-and-more

- www.futunn.com/403

- www.tradingkey.com/analysis/stocks/us-stocks/262090861-brent-crude-pullback-ai-demand-validation-dow-record-high-cpi-in-focus-tech-earnings-support-inflation-tradingkey

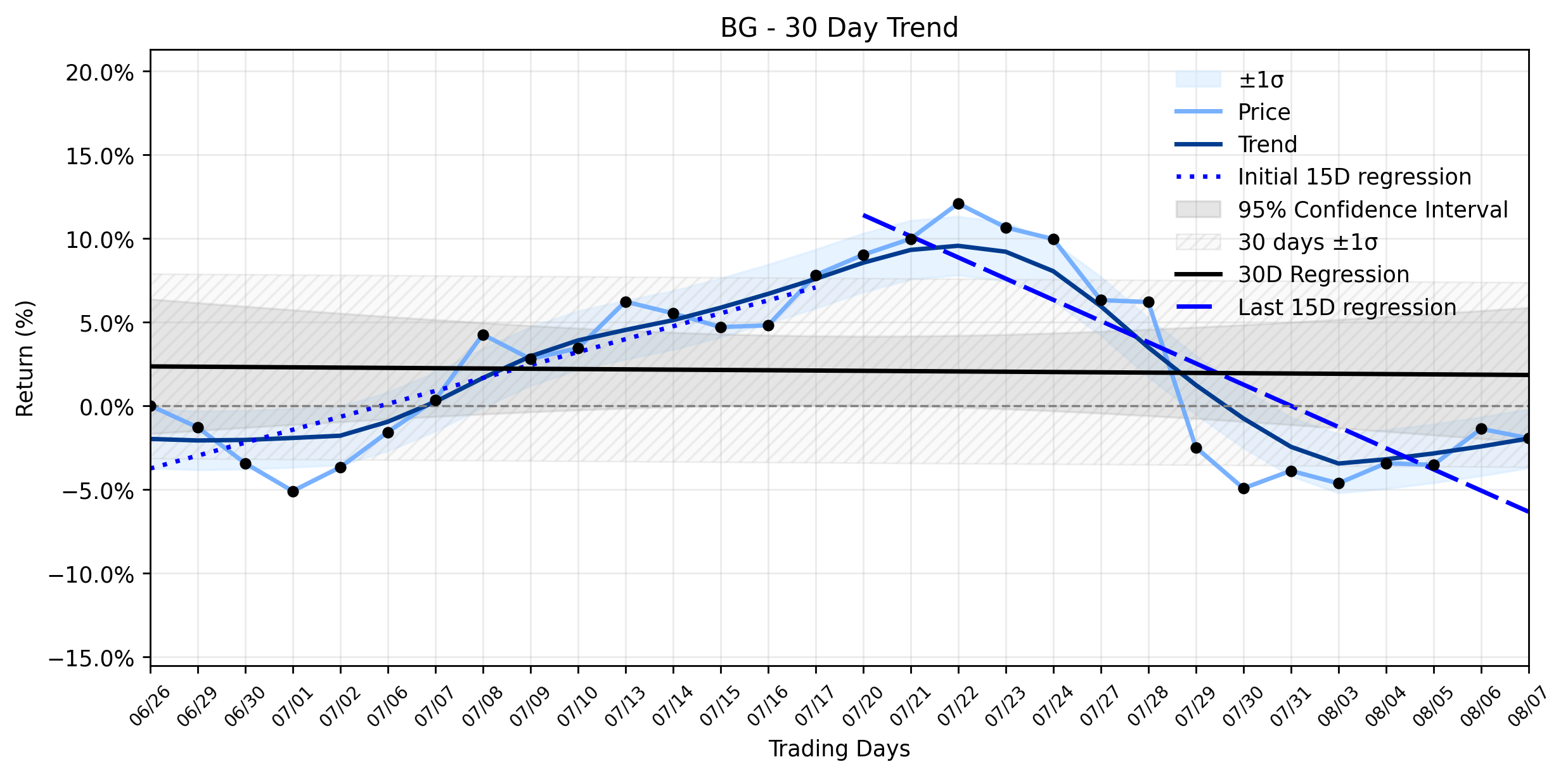

Bunge Global SA (BG) Sees a Pullback: Is This Emerging Downtrend an Undervalued Opportunity or a Warning from the Titans?

Pct Price Change: -0.57%

- https://finance.yahoo.com/quote/BG/

- simplywall.st/stocks/us/food-beverage-tobacco/nyse-bg/bunge-global/news/why-bunge-global-bg-could-be-24-undervalued-after-raising-fu

- www.marketscreener.com/news/bunge-posts-q2-earnings-beat-on-strong-crush-margins-raises-2026-outlook-ce7f51d2de8cf620

- www.stocktitan.net/sec-filings/BG/8-k-bunge-global-sa-reports-material-event-d2b7d148f603.html

- www.marketbeat.com/instant-alerts/filing-bunge-global-sa-bg-holdings-trimmed-by-the-manufacturers-life-insurance-company-2026-08-04/

- www.marketbeat.com/instant-alerts/filing-janus-henderson-group-plc-lowers-holdings-in-bunge-global-sa-bg-2026-08-07/

- www.gurufocus.com/news/9003715/bunge-global-sa-bg-director-christopher-mahoney-buys-6500-shares

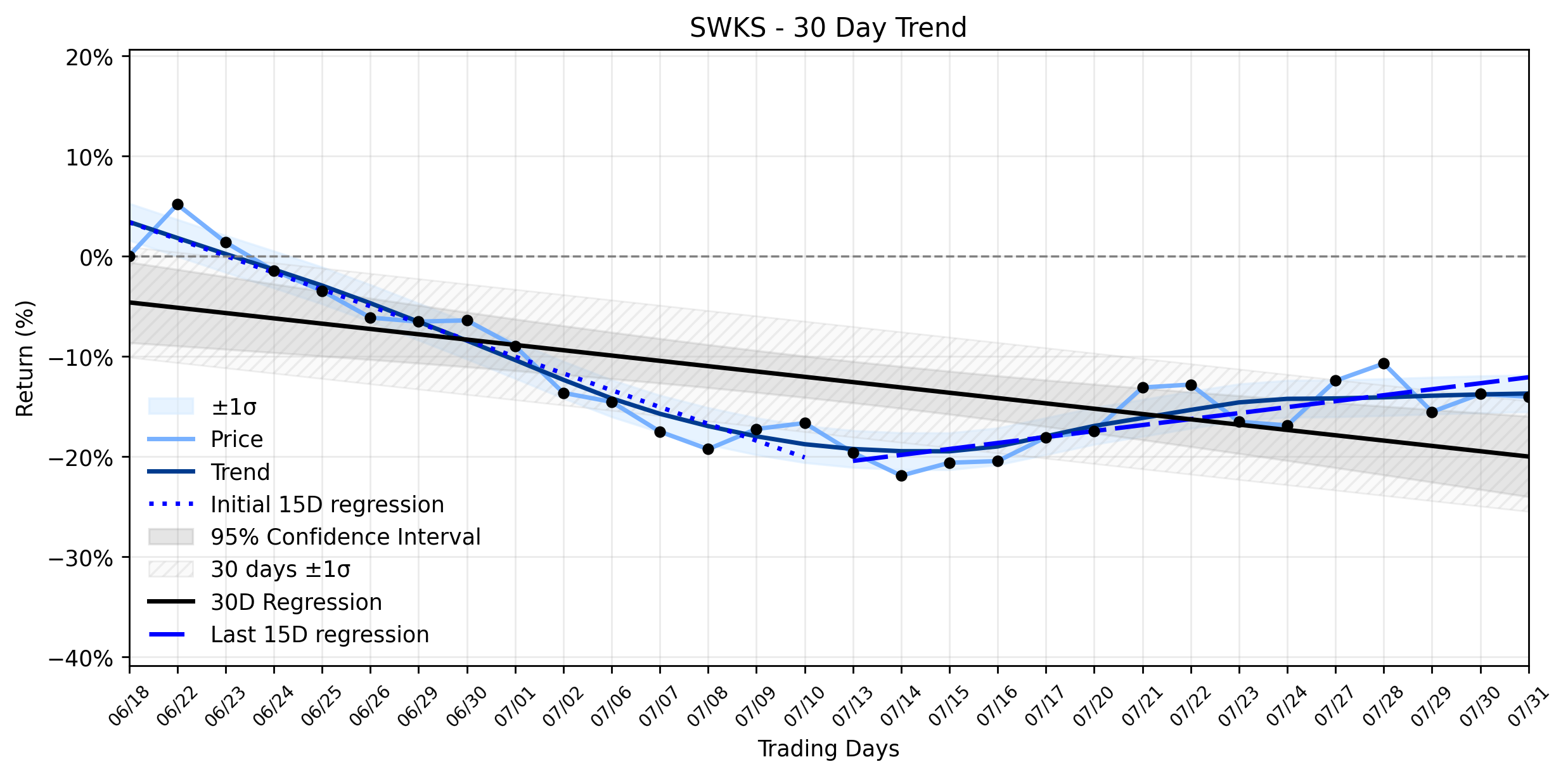

Skyworks Solutions (SWKS) Sees Powerful Rally: Is This the Breakout After a Strategic Pivot?

Pct Price Change: 5.66%

- https://finance.yahoo.com/quote/SWKS/

- www.stocktitan.net/news/SWKS/

- www.barchart.com/story/news/3510145/skyworks-solutions-nasdaqswks-exceeds-q2-expectations-but-stock-drops

- simplywall.st/stocks/us/semiconductors/nasdaq-swks/skyworks-solutions/news/skyworks-solutions-swks-buyback-and-dividend-shift-put-valua

- www.ocbj.com/oc-homepage/skyworks-qorvo-deal-ahead-of-schedule/

- www.marketscreener.com/news/skyworks-solutions-inc-announces-an-equity-buyback-for-2-000-million-worth-of-its-shares-ce7f51d2db8bfe27

- kalkinemedia.com/us/news/announcements/skyworks-solutions-halts-dividends-and-launches-2-billion-stock-buyback-program-through-2029

- www.stocktitan.net/sec-filings/SWKS/8-k-skyworks-solutions-inc-reports-material-event-80f1c71dda0a.html

- www.sahmcapital.com/news/content/how-investors-may-respond-to-skyworks-solutions-swks-suspending-its-dividend-while-launching-a-major-buyback-2026-08-01

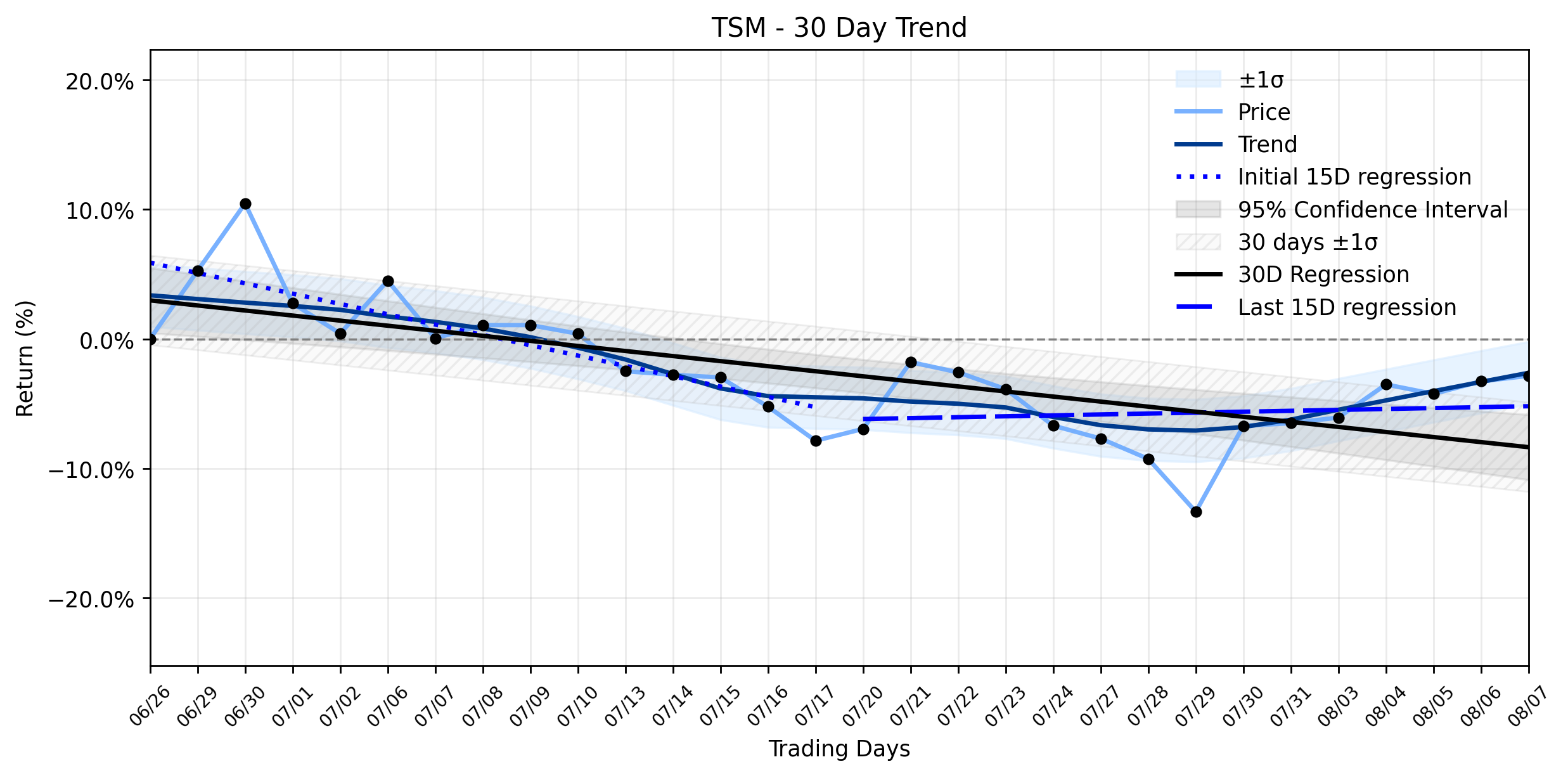

Taiwan Semiconductor (TSM) Sees Peculiar Uptick Amidst Stable Downtrend: What Record Revenue and AI Expansion Really Mean?

Pct Price Change: 0.44%

- https://finance.yahoo.com/quote/TSM/

- www.gurufocus.com/news/9020521/tsm-reports-record-july-revenue-of-nt46758-billion

- www.gurufocus.com/news/9020509/taiwan-semiconductor-tsm-reports-strong-july-revenue-growth-amid-ai-demand

- seekingalpha.com/news/4629700-tsmc-monthly-sales-jump-45-as-ai-chip-demand-stays-strong

- www.marketbeat.com/instant-alerts/filing-hennion-walsh-asset-management-inc-increases-holdings-in-taiwan-semiconductor-manufacturing-company-ltd-tsm-2026-08-09/

- www.marketbeat.com/instant-alerts/filing-taiwan-semiconductor-manufacturing-company-ltd-tsm-shares-sold-by-hf-advisory-group-llc-2026-08-09/

- wccftech.com/tsmc-1-4nm-fabs-longtan-expansion-landowner-reversal/

- www.taipeitimes.com/News/front/archives/2026/08/10/2003862220

InterDigital (IDCC) Surges: What's Fueling the Accelerating Uptrend Despite Lingering Doubts?

Pct Price Change: 4.92%

- https://finance.yahoo.com/quote/IDCC/

- simplywall.st/stocks/us/software/nasdaq-idcc/interdigital/news/why-interdigital-idcc-is-up-130-after-raising-2026-guidance

- www.sahmcapital.com/news/content/interdigital-idcc-could-be-33-below-fair-value-as-it-lifts-2026-outlook-2026-08-04

- www.marketbeat.com/instant-alerts/filing-interdigital-inc-idcc-shares-acquired-by-reinhart-partners-llc-2026-08-08/

- www.marketbeat.com/instant-alerts/insider-selling-interdigital-nasdaqidcc-cto-sells-1500-shares-of-stock-2026-08-07/

- www.stocktitan.net/sec-filings/IDCC/form-4-inter-digital-inc-insider-trading-activity-5d6aeb97d7ff.html

- simplywall.st/stocks/us/software/nasdaq-idcc/interdigital/news/interdigital-idcc-could-be-33-below-fair-value-as-it-lifts-2

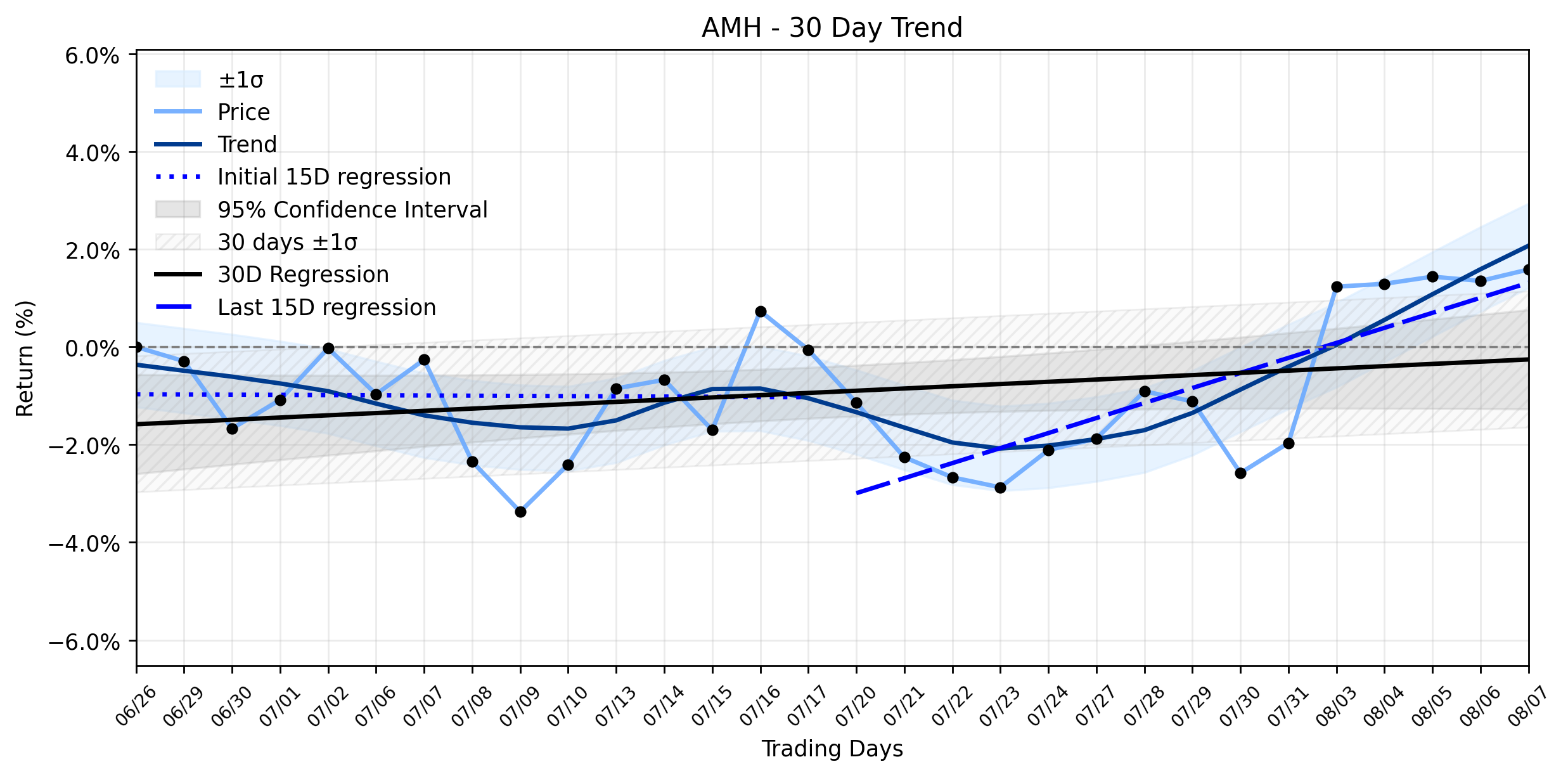

American Homes 4 Rent (AMH): Why Big Players Are Quietly Climbing Aboard an Accelerating Uptrend

Pct Price Change: 0.23%

- https://finance.yahoo.com/quote/AMH/

- www.fool.com/earnings/call-transcripts/2026/08/07/american-homes-4-rent-amh-q2-2026-earnings-call-transcript/

- www.prnewswire.com/news-releases/amh-reports-second-quarter-2026-financial-and-operating-results-302839489.html

- news.stocktradersdaily.com/news_release/101/Trading_Systems_Reacting_to_AMH_Volatility_080826093201_1786239121.html

- public.com/stocks/amh/forecast-price-target

- www.marketbeat.com/stocks/NYSE/AMH/forecast/

Herbalife Nutrition (HLF) Soars 7.3%: Unpacking the Potential Downside Amidst a Stable Downtrend

Pct Price Change: 7.30%

- https://finance.yahoo.com/quote/HLF/

- ir.herbalife.com/news-events/press-releases/detail/952/herbalife-reports-second-quarter-net-sales-growth-marks

- seekingalpha.com/article/4933805-herbalife-ltd-2026-q2-results-earnings-call-presentation

- www.marketbeat.com/instant-alerts/wall-street-zen-downgrades-herbalife-nysehlf-to-hold-2026-08-08/

- ir.herbalife.com/news-events/press-releases/detail/951/herbalife-announces-planned-cfo-transition

- www.marketbeat.com/instant-alerts/herbalife-nysehlf-releases-earnings-results-misses-estimates-by-003-eps-2026-08-07/

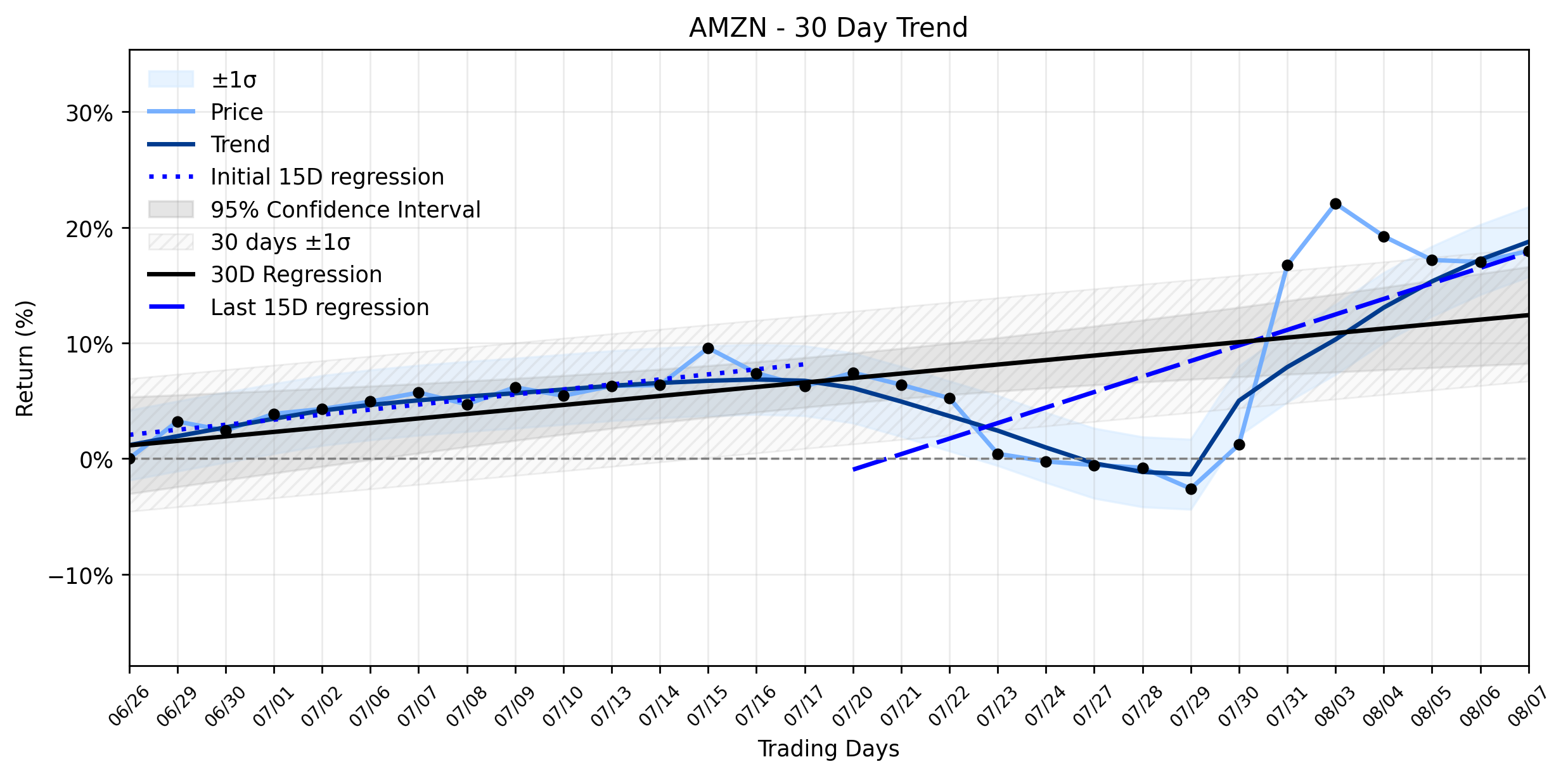

Amazon (AMZN) Continues Its Stable Uptrend: What the $220 Billion AI Bet Means for Investors' Next Move

Pct Price Change: 0.82%

- https://finance.yahoo.com/quote/AMZN/

- www.fool.com/investing/2026/08/08/jeff-bezos-amazon-just-raised-its-ai-spending-to-2/

- www.fool.com/investing/2026/08/09/jeff-bezos-amazon-stock-billion-surged-still-buy/

- stocktwits.com/news-articles/markets/equity/amzn-stock-turns-positive-for-2026-on-aws-momentum-analyst-calls-ceo-jassy-s-shareholder-letter-most-impactful-yet/cZJ0dSnRItb

- www.fool.com/investing/2026/08/08/amazons-stock-just-soared-15-heres-why-now-is-just/

- www.fool.com/investing/2026/08/07/amazon-stock-analysis-buy-or-sell-my-final-verdict/

- www.aboutamazon.com/news/company-news/amazon-news-today-top-stories-company

Exelon (EXC) Defies Its Stable Downtrend: What's Really Powering This Modest Gain Amidst Shifting Data Center Ambitions?

Pct Price Change: 0.64%

- https://finance.yahoo.com/quote/EXC/

- public.com/stocks/exc/forecast-price-target

- www.marketbeat.com/stocks/NASDAQ/EXC/forecast/

- www.perplexity.ai/finance/EXC?comparing=EXC,SO,EIX,AEP,PCG,PEG

- stockanalysis.com/stocks/exc/

- www.marketbeat.com/instant-alerts/filing-pacer-advisors-inc-cuts-stock-position-in-exelon-corporation-exc-2026-08-06/

- www.fool.com/earnings/call-transcripts/2026/08/04/exelon-exc-q2-2026-earnings-call-transcript/

- www.marketbeat.com/instant-alerts/filing-exelon-corporation-exc-stake-reduced-by-janus-henderson-group-plc-2026-08-06/

- www.exeloncorp.com/newsroom/exelon-reports-second-quarter-2026-results

- seekingalpha.com/news/4622307-exelon-slides-after-slashing-data-center-forecast-as-consumers-push-back-against-development

- www.tdworld.com/utility-business/news/55395407/exelon-weeds-out-data-center-pipeline

- www.exeloncorp.com/newsroom

- www.stocktitan.net/news/EXC/com-ed-marks-350-million-in-distributed-generation-rebates-with-k0z1stgvnpue.html

- www.zacks.com/stock/news/2967499/heres-why-exelon-exc-is-a-strong-value-stock

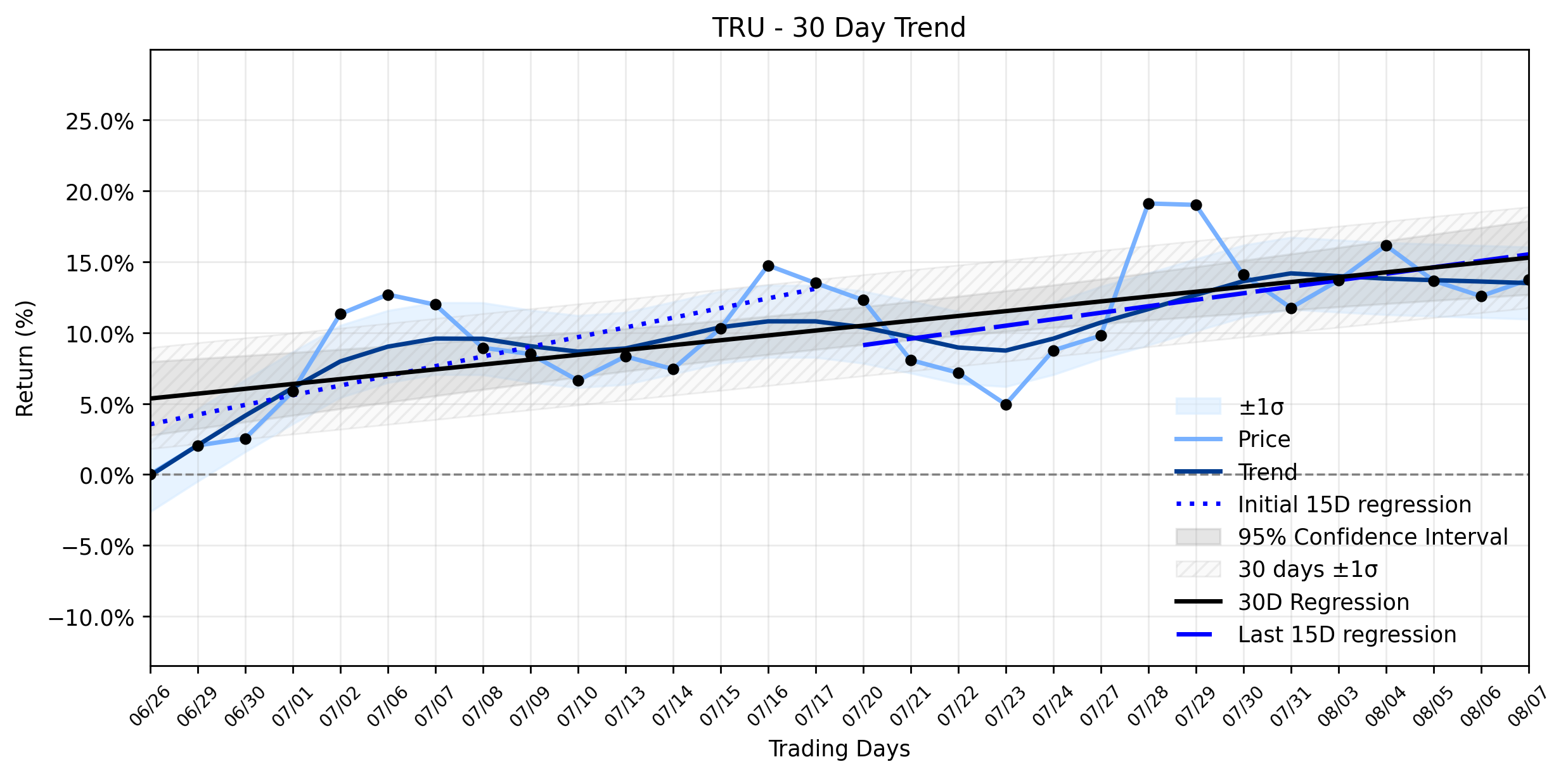

TransUnion (TRU) Ascends on Strong Earnings: Is a Sustained Uptrend Shift Underway?

Pct Price Change: 1.04%

- https://finance.yahoo.com/quote/TRU/

- www.marketbeat.com/instant-alerts/filing-transunion-tru-shares-acquired-by-bank-of-america-corp-de-2026-08-08/

- www.marketbeat.com/instant-alerts/transunion-nysetru-downgraded-to-hold-rating-by-wall-street-zen-2026-08-09/

- newsroom.transunion.com/

- www.dividendinvestor.com/dividend-news/20260805/transunion-nyse-tru-declared-a-dividend-of-$0.1250-per-share/

- www.investing.com/news/company-news/transunion-declares-0125-quarterly-dividend-93CH-4841038

- thefintechtimes.com/transunion-warns-lenders-on-private-student-loan-risk-after-us-rules/

Disney (DIS) Charts a Subtle Uptick: Is This the Unseen Opportunity in the Kingdom's Accelerating Ascent?

Pct Price Change: 0.22%

- https://finance.yahoo.com/quote/DIS/

- www.gurufocus.com/news/9020050/dis-looks-79-undervalued-on-gf-value

- www.marketbeat.com/instant-alerts/filing-the-walt-disney-company-dis-shares-sold-by-newedge-advisors-llc-2026-08-08/

- seekingalpha.com/news/4625842-disney-shares-rise-after-q3-profit-beats-estimates-on-parks-strength

- www.vantagemarkets.com/market-analysis/dis-stock-price-today-disney-shares-rally-q3-earnings-beat-august-7-2026/

- investor.wedbush.com/wedbush/article/stockstory-2026-8-5-disney-nysedis-misses-q2-cy2026-revenue-estimates

- www.investing.com/analysis/disney-stock-buybacks-margins-and-2027-guidance-fuel-bullish-case-200685392

- seekingalpha.com/news/4626444-disney-targets-at-least-9b-of-fy-2026-buybacks-while-outlining-spring-2027-disney-ecosystem

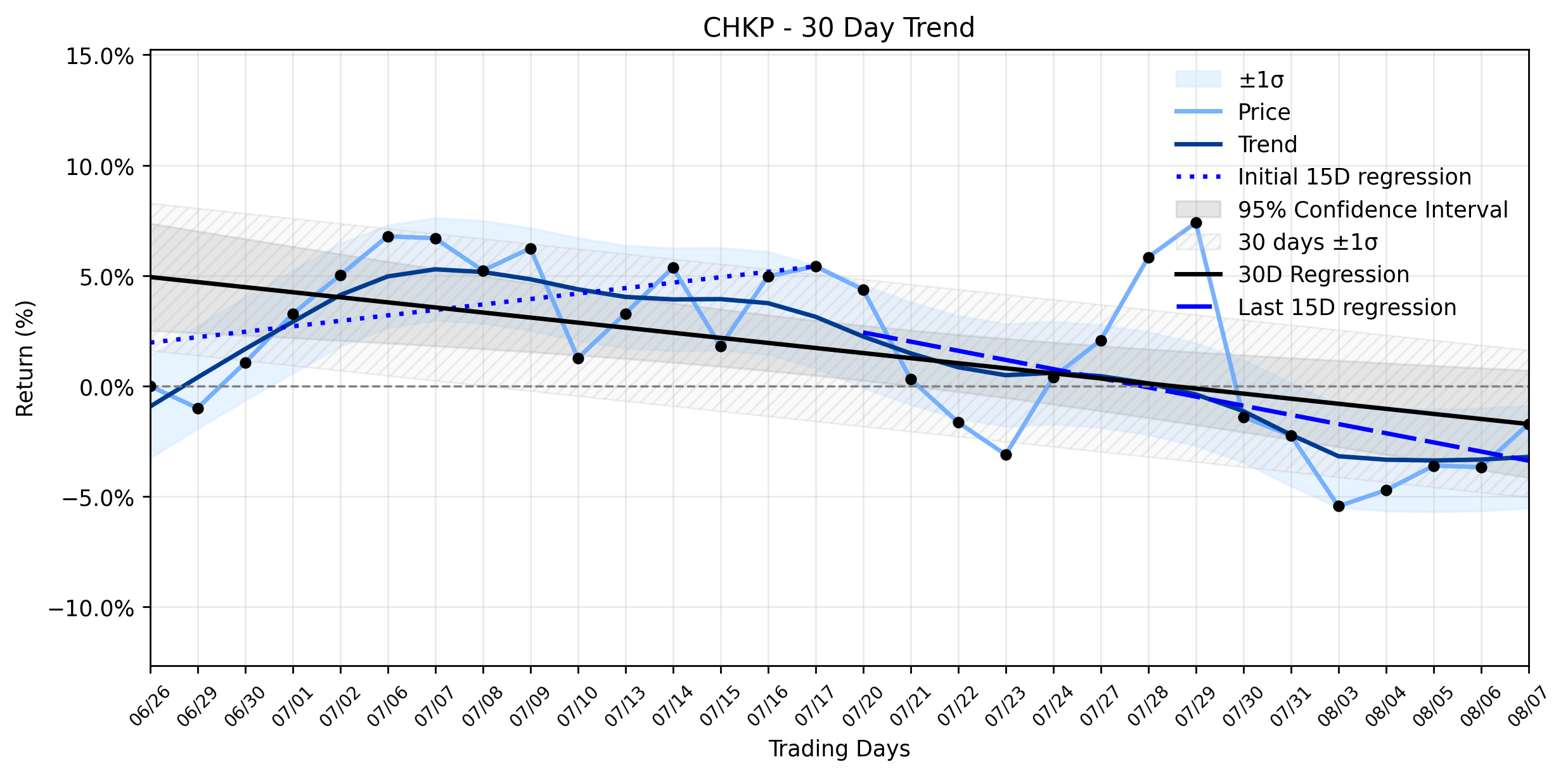

Check Point Software (CHKP) Stages Impressive Gain: Is Its Underappreciated AI Edge Finally Stabilizing a Downtrend?

Pct Price Change: 2.03%

- https://finance.yahoo.com/quote/CHKP/

- www.tradingview.com/news/tradingview:b396ea9344eb4:0-check-point-software-technologies-ltd-stock-12-month-price-target-cut-to-143-7-implies-12-upside/

- kalkinemedia.com/us/news/top-stories/can-check-point-software-nasdaqchkp-sustain-its-cybersecurity-edge

- www.prnewswire.com/news-releases/check-point-software-named-a-visionary-leader-in-the-2026-frost-radar-for-enterprise-risk-mitigation-and-management-platforms-302840981.html

- www.stocktitan.net/news/CHKP/check-point-software-named-a-visionary-leader-in-the-2026-frost-6rj5nqts6kz3.html

- www.itweb.co.za/article/check-points-new-ai-network-firewall-closes-ai-blind-spot-everywhere/j5alrvQArnEvpYQk

- securityboulevard.com/2026/08/check-point-puts-ai-traffic-controls-into-its-existing-firewalls/

- seekingalpha.com/news/4621413-check-point-software-falls-after-mixed-q2-results

Progressive (PGR) Sees Quiet Pullback: Is the "Growth Machine" Primed for an Upside Reversal Despite Recent Headwinds?

Pct Price Change: 0.00%

- https://finance.yahoo.com/quote/PGR/

- www.fool.com/investing/2026/08/08/progressives-combined-ratio-widened-to-871-last-qu/

- www.investing.com/news/transcripts/earnings-call-transcript-progressive-beats-q2-2026-estimates-but-shares-fall-93CH-4835121

- www.zacks.com/stock/news/2967429/progressive-pgr-q2-earnings-taking-a-look-at-key-metrics-versus-estimates

- finance.biggo.com/news/US_PGR_2026-08-04

- simplywall.st/stocks/us/insurance/nyse-pgr/progressive/news/progressives-bundled-robinson-strategy-could-be-a-game-chang

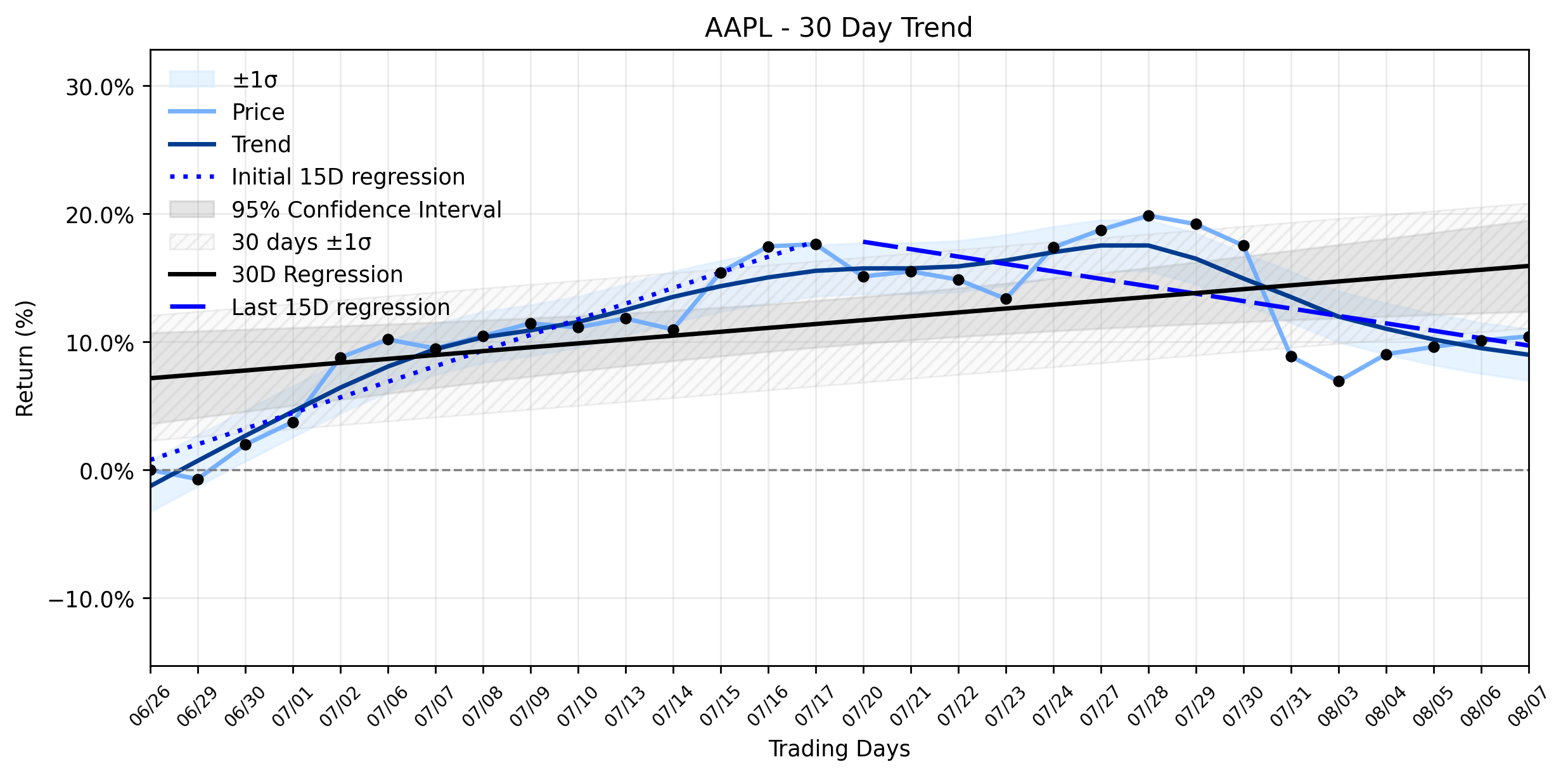

Apple (AAPL) Posts Subtle Uptick: A Quiet Trigger Amidst a Looming Trend Reversal?

Pct Price Change: 0.29%

- https://finance.yahoo.com/quote/AAPL/

- www.marketbeat.com/stocks/NASDAQ/AAPL/earnings/

- www.fool.com/investing/2026/08/09/apple-added-about-15-trillion-in-market-value-in-a/

- www.macrumors.com/2026/07/30/apple-3q-2026-earnings/

- 247wallst.com/investing/2026/08/07/apples-capex-strategy-worked-but-other-pressures-are-mounting-now/

- 247wallst.com/investing/2026/08/07/prediction-can-apple-stock-reach-400-this-year/

- www.apple.com/newsroom/2026/07/apple-reports-third-quarter-results/

- 247wallst.com/investing/2026/08/03/apples-predictable-august-news-vacuum-tells-you-exactly-what-to-expect-this-month/

- www.marketbeat.com/instant-alerts/filing-apple-inc-aapl-stock-position-decreased-by-goepper-burkhardt-llc-2026-08-08/

- www.moomoo.com/403

Mondelez International (MDLZ) Takes a Quiet Pullback: Is This the Calm Before the Next Ascent in a Stable Uptrend?

Pct Price Change: -0.22%

- https://finance.yahoo.com/quote/MDLZ/

- kalkinemedia.com/us/stocks/consumer/mondelez-nasdaqmdlz-in-focus-as-snacking-demand-meets-a-cautious-tape

- www.marketbeat.com/instant-alerts/filing-mondelez-international-inc-mdlz-shares-bought-by-pensiondanmark-pensionsforsikringsaktieselskab-2026-08-08/

- www.marketbeat.com/instant-alerts/filing-czech-national-bank-raises-stake-in-mondelez-international-inc-mdlz-2026-08-08/

- www.tastingtable.com/2228851/best-selling-company-2026-not-hershey-ferrero/

- ir.mondelezinternational.com/news-and-events/financial-news/

- www.zacks.com/stock/news/2966430/mondelez-mdlz-reliance-on-international-sales-what-investors-need-to-know

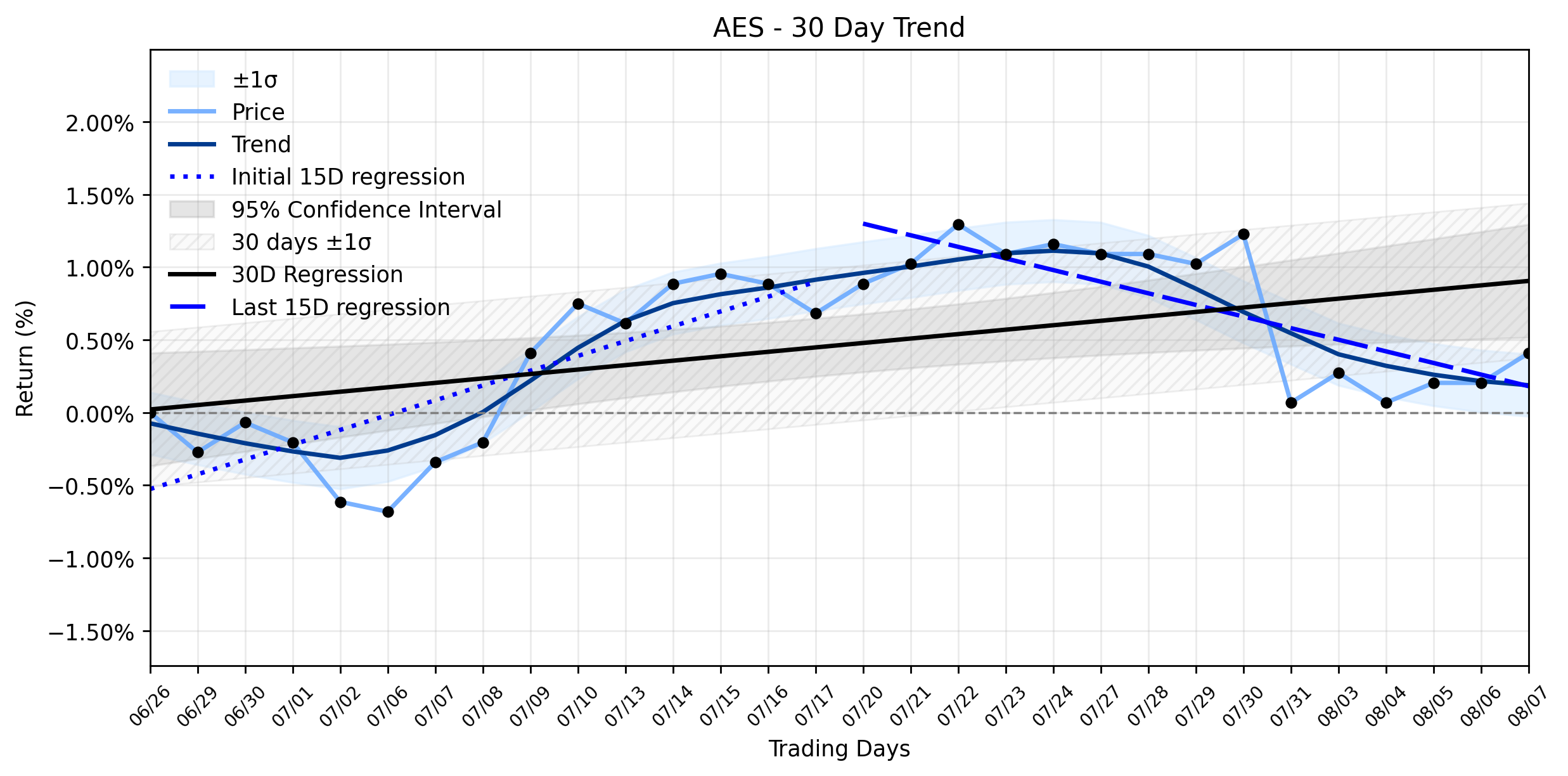

AES Corporation (AES): The 'Efficient' Truth Behind a Minor Gain and an Emerging Downtrend – Is the Acquisition the Only Play?

Pct Price Change: 0.20%

- https://finance.yahoo.com/quote/AES/

- ca.investing.com/news/earnings/the-aes-earnings-missed-by-013-revenue-topped-estimates-4776097

- www.prnewswire.com/news-releases/aes-stockholders-approve-acquisition-by-global-infrastructure-partners-and-eqt-led-consortium-302812261.html

- www.forbes.com/sites/davidblackmon/2026/08/02/opponents-of-the-aes-deal-are-fighting-the-wrong-battle/

- www.perplexity.ai/finance/AES

- morganhilltimes.com/virginia-firm-drops-plans-for-battery-storage-site-in-coyote-valley/

- public.com/stocks/aes/forecast-price-target

Costco (COST) Experiences a Quiet Pullback: Is This the Setup for its Next Ascent Amidst a Stable Uptrend?

Pct Price Change: -0.14%

- https://finance.yahoo.com/quote/COST/

- www.crosstimbersgazette.com/2026/08/08/costco-files-documents-for-possible-store-in-flower-mound/

- www.fox9.com/news/costco-opening-7-new-stores-august-more-locations-planned-expansion-continues-see-where?taid=6a5698d7acbde00001f24ea3&utm_campaign=trueanthem&utm_medium=trueanthem&utm_source=twitter

- www.mashed.com/2232735/costco-product-price-cuts-august-2026/

- www.marketbeat.com/instant-alerts/filing-chesley-taft-associates-llc-cuts-stake-in-costco-wholesale-corporation-cost-2026-08-08/

- www.tribtoday.com/news/business/2026/08/us-stocks-jump-as-employers-cut-23000-jobs-raising-hopes-that-rate-hikes-can-wait/

- www.fool.com/investing/2026/08/09/stock-market-investors-bad-news-federal-reserve/

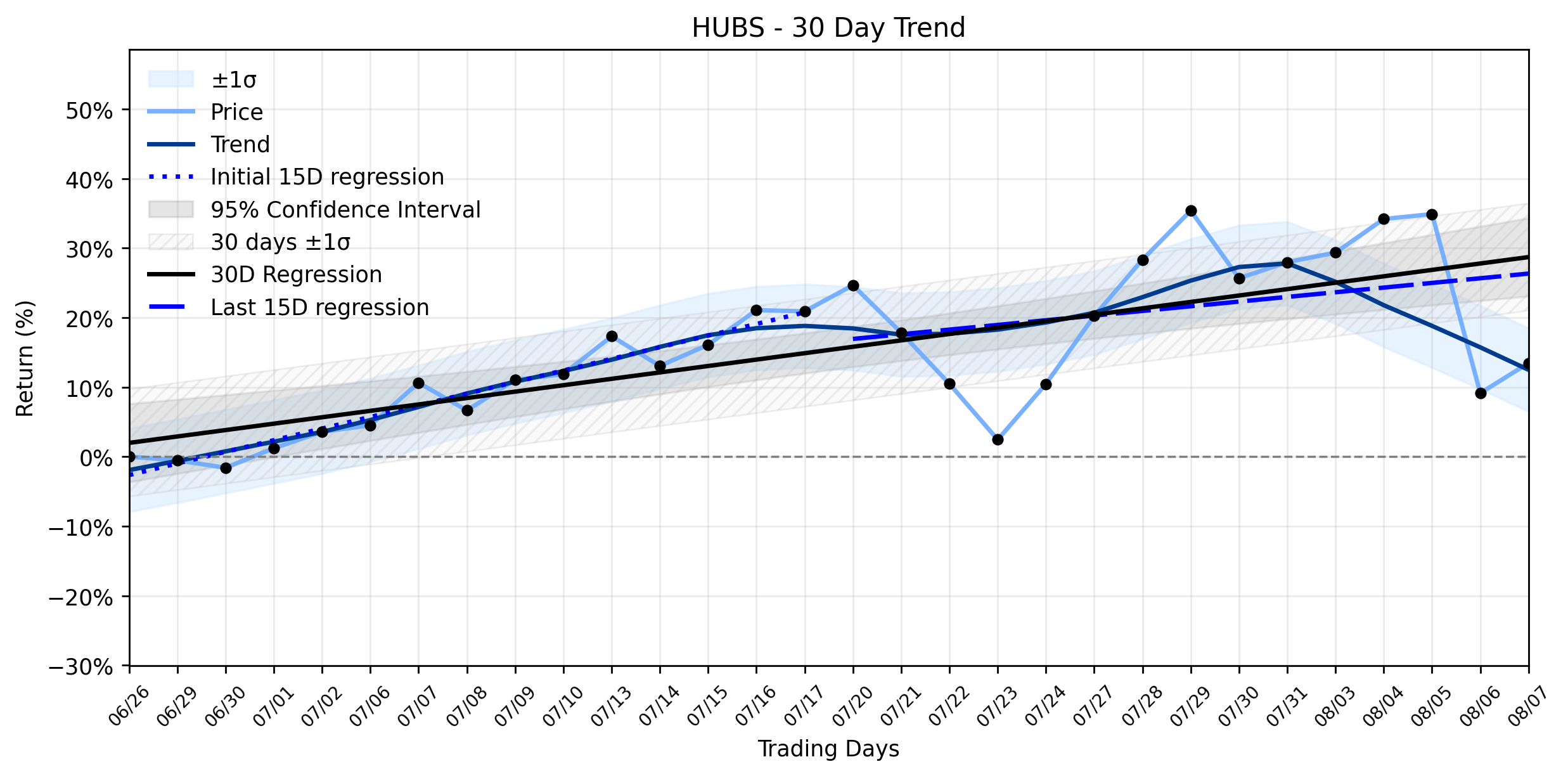

HubSpot (HUBS) Stages a Surprising Surge: Is the Market Re-evaluating Its Customer Growth Woes After a Major Plunge?

Pct Price Change: 3.96%

- https://finance.yahoo.com/quote/HUBS/

- www.fool.com/investing/2026/08/08/hubspot-just-cut-its-own-customer-growth-forecast/

- investor.wedbush.com/wedbush/article/stockstory-2026-8-5-hubspots-nysehubs-q2-cy2026-sales-beat-estimates-but-stock-drops-202

- simplywall.st/stocks/us/software/nyse-hubs/hubspot/news/hubspot-hubs-stock-reels-from-slower-customer-growth-despite

- www.marketbeat.com/instant-alerts/hubspot-q2-earnings-call-highlights-2026-08-08/

- www.stocktitan.net/sec-filings/HUBS/8-k-hubspot-inc-reports-material-event-698836f8e527.html

Zebra Technologies (ZBRA) Ignites an Accelerating Uptrend: Is Smart Money Fueling a Breakout, or Just Testing the Waters?

Pct Price Change: 3.36%

- https://finance.yahoo.com/quote/ZBRA/

- www.inkworldmagazine.com/breaking-news/zebra-technologies-announces-q2-2026-results/

- www.zacks.com/stock/news/2967765/zbra-q2-earnings-beat-estimates-on-sales-growth-outlook-raised

- www.zebra.com/us/en/about-zebra/newsroom/press-releases/2026/zebra-technologies-announces-second-quarter-2026-results.html

- www.marketbeat.com/earnings/reports/2026-8-4-zebra-technologies-co-stock/

- www.gurufocus.com/news/9018627/zebra-technologies-corp-zbra-shares-surge-34-what-gf-score-of-81-tells-investors

- seekingalpha.com/article/4930255-zebra-changed-its-stripes-460-stampede-is-just-beginning

- www.fool.com/investing/2026/08/04/zebra-technologies-stock-jumped-20-today/

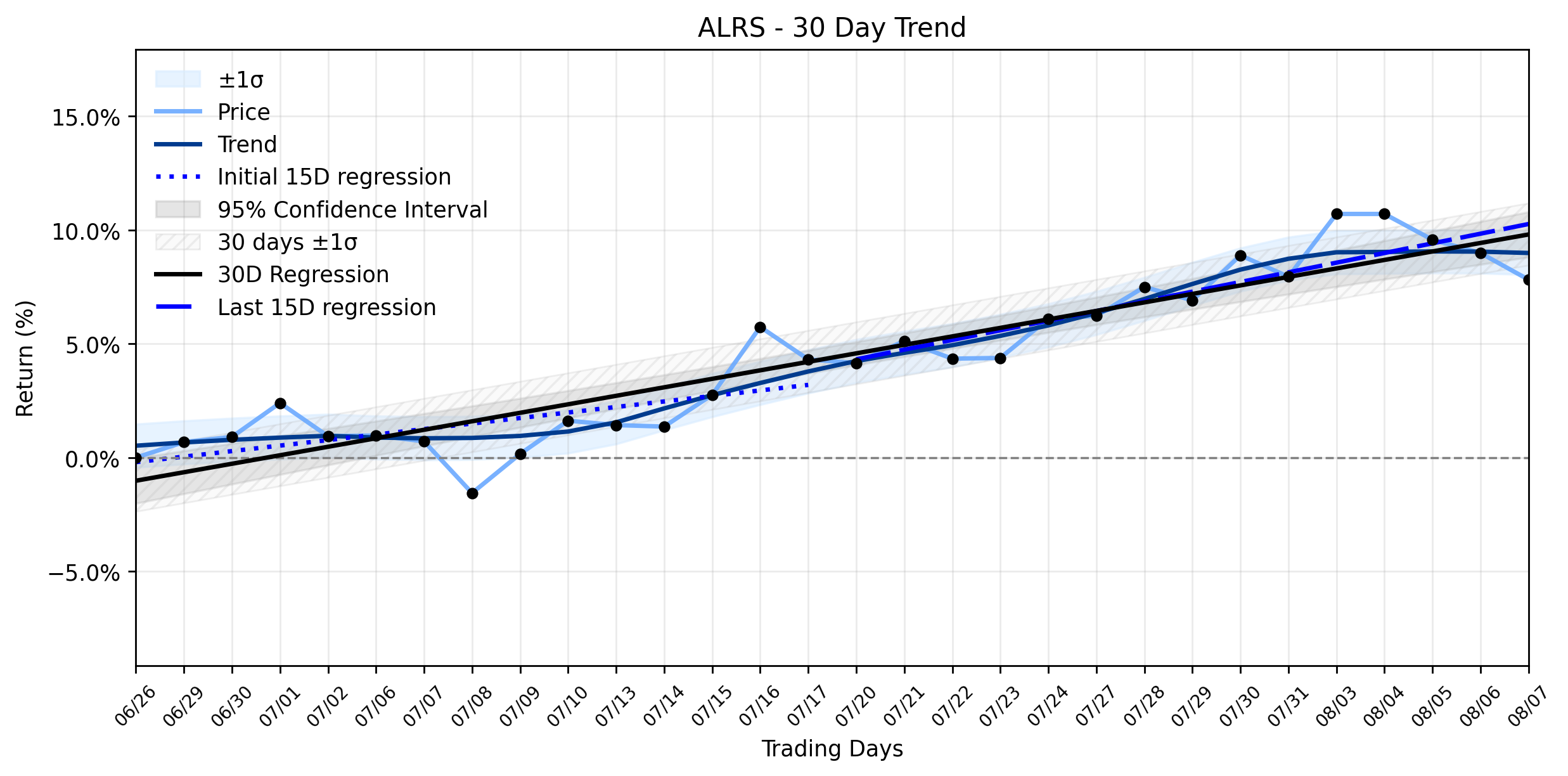

Alerus Financial (ALRS) Takes a Pullback: Is This Undervalued Gem Facing a Reality Check or a Buying Opportunity?

Pct Price Change: -1.07%

- https://finance.yahoo.com/quote/ALRS/

- www.marketbeat.com/instant-alerts/alerus-financial-nasdaqalrs-sets-new-12-month-high-still-a-buy-2026-08-05/

- www.investing.com/news/analyst-ratings/raymond-james-raises-alerus-financial-stock-price-target-on-credit-cleanup-93CH-4830567

- www.fool.com/earnings/call-transcripts/2026/08/07/alerus-financial-alrs-q2-2026-earnings-call-transcript/?source=iedfolrf0000001

- seekingalpha.com/news/4622202-alerus-forecasts-2026-net-interest-margin-of-about-3_7-percentminus-3_8-percent-as-credit

- seekingalpha.com/article/4931713-alerus-financial-strong-profitability-but-limited-upside-at-current-valuation

- news.stocktradersdaily.com/news_release/23/ALRS_and_the_Role_of_Price-Sensitive_Allocations_080826090201_1786237321.html

América Móvil (AMX) Slides Further: Is This Downtrend Accelerating Towards a Reversal or Deeper Abyss?

Pct Price Change: -0.71%

- https://finance.yahoo.com/quote/AMX/

- news.stocktradersdaily.com/news_release/12/AMX_Volatility_Zones_as_Tactical_Triggers_080826095802_1786240682.html

- www.zacks.com/stock/news/2969743/after-plunging-9-in-4-weeks-heres-why-the-trend-might-reverse-for-amer-movil-amx

- www.investing.com/news/transcripts/earnings-call-transcript-america-movil-posts-q2-2026-revenue-beat-eps-miss-93CH-4806602

- www.stocktitan.net/sec-filings/AMX/6-k-america-movil-sab-de-cv-current-report-foreign-issuer-1b2086537319.html

- support.levelblue.com/first-dry/America-Movil-Targets-Steady-Growth-Maintains-7-Billion-Capex-Plan-21-12305

- www.rcrwireless.com/20260423/5g/america-movil-capex

- dukecountry.fm/2026/05/27/mexican-telecoms-giant-america-movil-targets-steady-growth-holds-capex-at-7-billion/

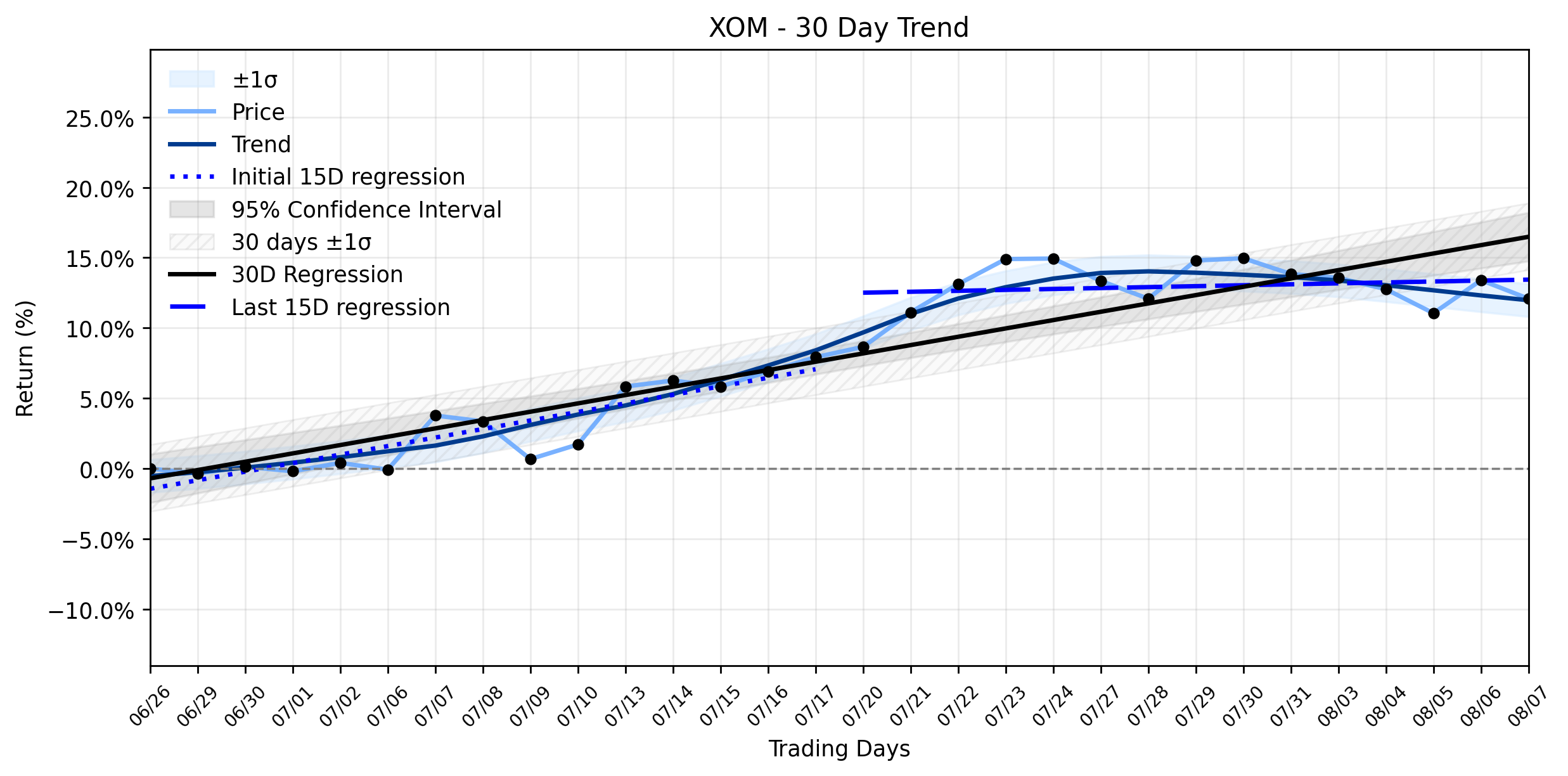

ExxonMobil (XOM) Takes a Dip: Is This the Inevitable Slowdown of a Weakening Uptrend, or Just a Market Misread?

Pct Price Change: -1.16%

- https://finance.yahoo.com/quote/XOM/

- www.marketbeat.com/instant-alerts/exxonmobil-nysexom-trading-down-13-should-you-sell-2026-08-07/

- www.fool.com/investing/2026/08/07/exxons-profit-fell-short-its-dividend-didnt/

- www.zacks.com/stock/news/2971125/xom-q2-earnings-call-highlights-refining-strength-and-guyana-cash-flow

- corporate.exxonmobil.com/what-we-do/delivering-industrial-solutions

- corporate.exxonmobil.com/what-we-do/delivering-industrial-solutions/carbon-capture-and-storage/rethinking-how-co2-moves-at-scale

- seekingalpha.com/article/4932618-exxonmobil-beyond-the-ev-narrative-and-strategic-reserve-rebuilding

X4 Pharmaceuticals (XFOR) Ignites a Powerful Rally: Is This Breakout a Hidden Vulnerability in Disguise?

Pct Price Change: 11.27%

- https://finance.yahoo.com/quote/XFOR/

- www.marketbeat.com/instant-alerts/x4-pharmaceuticals-nasdaqxfor-releases-earnings-results-beats-expectations-by-005-eps-2026-08-06/

- www.zacks.com/stock/news/2970490/x4-pharmaceuticals-xfor-reports-q2-loss-beats-revenue-estimates

- simplywall.st/stocks/us/pharmaceuticals-biotech/nasdaq-xfor/x4-pharmaceuticals/news/x4-pharmaceuticals-xfor-stock-rallies-on-revenue-traction-de/amp

- www.stocktitan.net/news/XFOR/x4-pharmaceuticals-reports-second-quarter-2026-financial-results-and-1ia0cs41eysa.html

- www.biospace.com/press-releases/x4-pharmaceuticals-reports-second-quarter-2026-financial-results-and-provides-corporate-update

- simplywall.st/stocks/us/pharmaceuticals-biotech/nasdaq-xfor/x4-pharmaceuticals/news/x4-pharmaceuticals-xfor-stock-rallies-on-revenue-traction-de

- www.marketbeat.com/stocks/NASDAQ/XFOR/

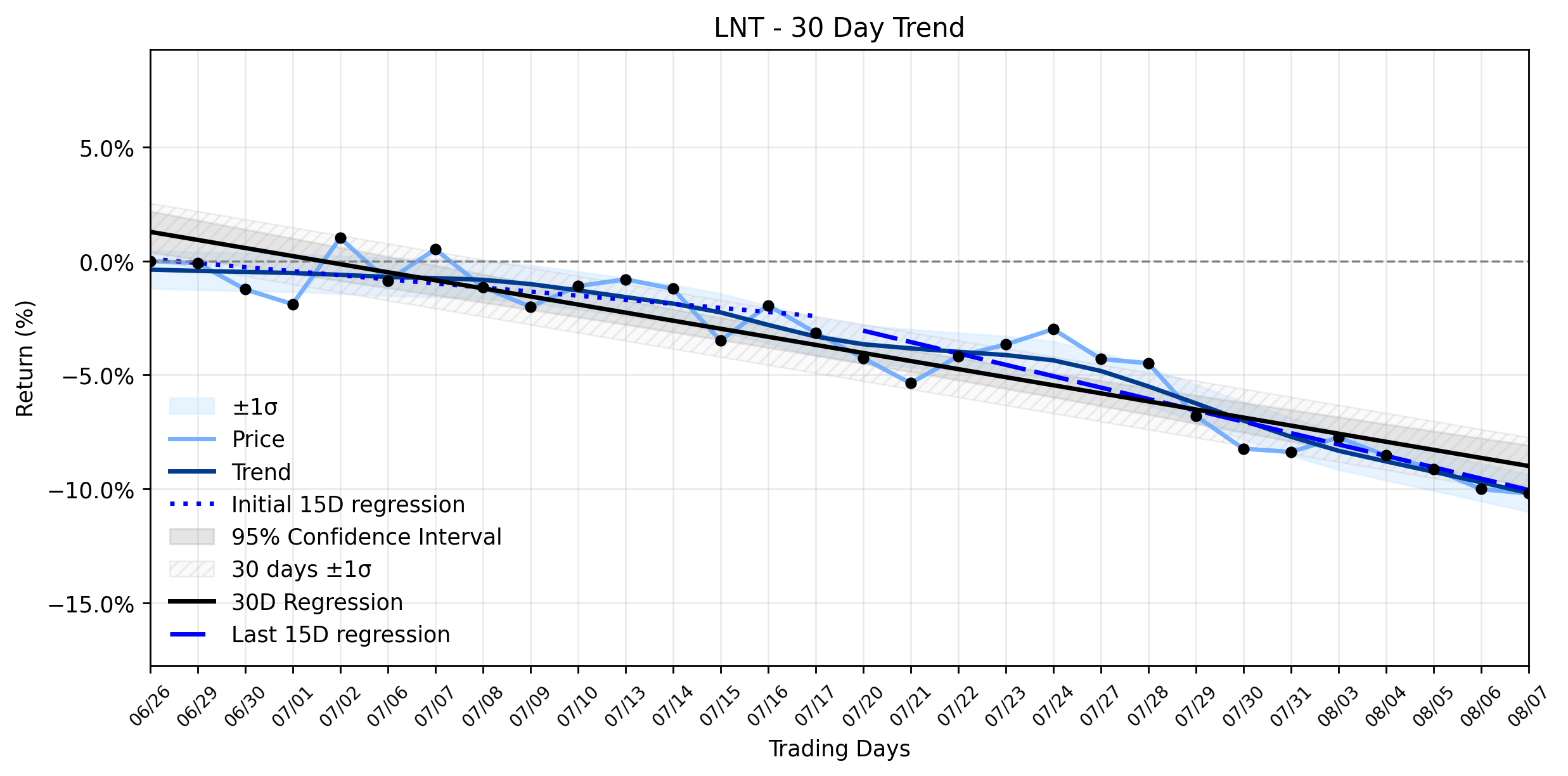

Alliant Energy (LNT): A Subtle Retreat Amidst Reaffirmed Guidance – What's Overlooked in the Downtrend's Stabilization?

Pct Price Change: -0.22%

- https://finance.yahoo.com/quote/LNT/

- simplywall.st/stocks/us/utilities/nasdaq-lnt/alliant-energy/news/alliant-energy-lnt-reaffirmed-2026-guidance-is-the-upside-al

- www.tradingview.com/news/zacks:c91240f08094b:0-alliant-energy-q2-earnings-lag-estimates-revenues-increase-y-y/

- www.zacks.com/stock/news/2966123/alliant-energy-q2-earnings-lag-estimates-revenues-increase-yy

- www.sahmcapital.com/news/content/alliant-energy-lnt-stock-faces-flat-earnings-and-margin-compression-2026-08-01

- www.marketbeat.com/instant-alerts/filing-segall-bryant-hamill-llc-invests-210-million-in-alliant-energy-corporation-lnt-2026-08-05/

- www.marketbeat.com/stocks/NASDAQ/LNT/forecast/

- robinhood.com/us/en/stocks/LNT/

- stockanalysis.com/stocks/lnt/forecast/

- news.stocktradersdaily.com/news_release/24/Liquidity_Mapping_Around_LNT_Price_Events_080826064002_1786185602.html

Unveiling the Forces Behind CAE's (CAE) Impressive Gain Amidst a Shifting Analyst Landscape

Pct Price Change: 1.53%

- https://finance.yahoo.com/quote/CAE/

- www.zacks.com/stock/news/2970841/cae-cae-q1-earnings-on-the-horizon-analysts-insights-on-key-performance-measures

- www.stocktitan.net/news/CAE/advisory-cae-s-fy2027-q1-financial-results-conference-call-and-h869b88ruupi.html

- www.marketbeat.com/instant-alerts/cae-cae-expected-to-release-earnings-on-wednesday-2026-08-05/

- site.financialmodelingprep.com/market-news/cae-inc-tsx-cae-nasdaq-stock-listing-transformation

- seekingalpha.com/article/4923509-cae-upgraded-to-strong-buy-on-turnaround-progress

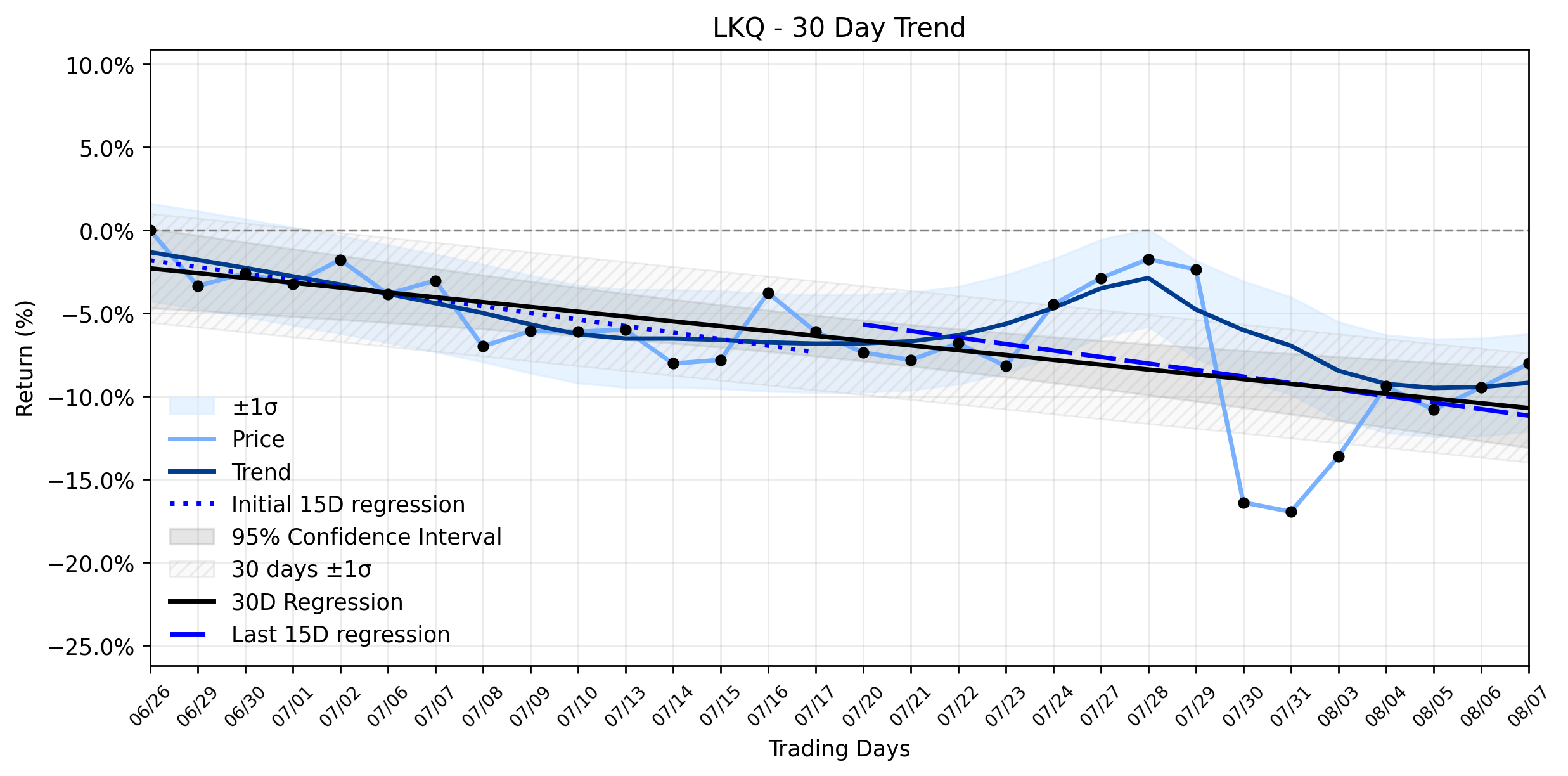

LKQ Corporation (LKQ): Is Yesterday's Notable Rally a Sign of Strength or a Glimpse into Deeper Vulnerability?

Pct Price Change: 1.59%

- https://finance.yahoo.com/quote/LKQ/

- simplywall.st/stocks/us/retail/nasdaq-lkq/lkq

- seekingalpha.com/article/4930463-lkq-stock-north-america-improved-but-europe-still-drag

- rvbusiness.com/lkq-announces-solid-execution-for-second-quarter-2026/

- www.marketscreener.com/news/lkq-corporation-revises-earnings-guidance-for-the-fiscal-year-2026-ce7f50dbd88ef022

- www.globenewswire.com/news-release/2026/07/30/3335904/8053/en/lkq-corporation-announces-results-for-second-quarter-2026.html

- markets.chroniclejournal.com/chroniclejournal/article/stockstory-2026-8-6-lkqs-q2-earnings-call-our-top-5-analyst-questions

- markets.financialcontent.com/stocks/article/stockstory-2026-8-6-lkqs-q2-earnings-call-our-top-5-analyst-questions

- www.collisionrepairmag.com/news/recycling/article/15831967/used-and-aftermarket-parts-usage-rates-reach-record-levels

- stockinvest.us/stock/LKQ

- www.tipranks.com/news/3-dividend-stocks-with-5-yield-to-buy-in-august-2026-according-to-analysts

American Tower (AMT) Rises: What's Fueling the Stable Uptrend Beneath the Surface of Shifting Investor Tides?

Pct Price Change: 0.78%

- https://finance.yahoo.com/quote/AMT/

- www.idcnova.com/news/American-Tower-bullish-on-US-spectrum-deployment-opportunities

- kalkinemedia.com/us/stocks/infrastructure-and-real-estate/american-tower-nyseamt-moves-as-data-center-demand-climbs-today

- www.marketbeat.com/instant-alerts/filing-sarasin-partners-llp-lowers-holdings-in-american-tower-corporation-amt-2026-08-07/

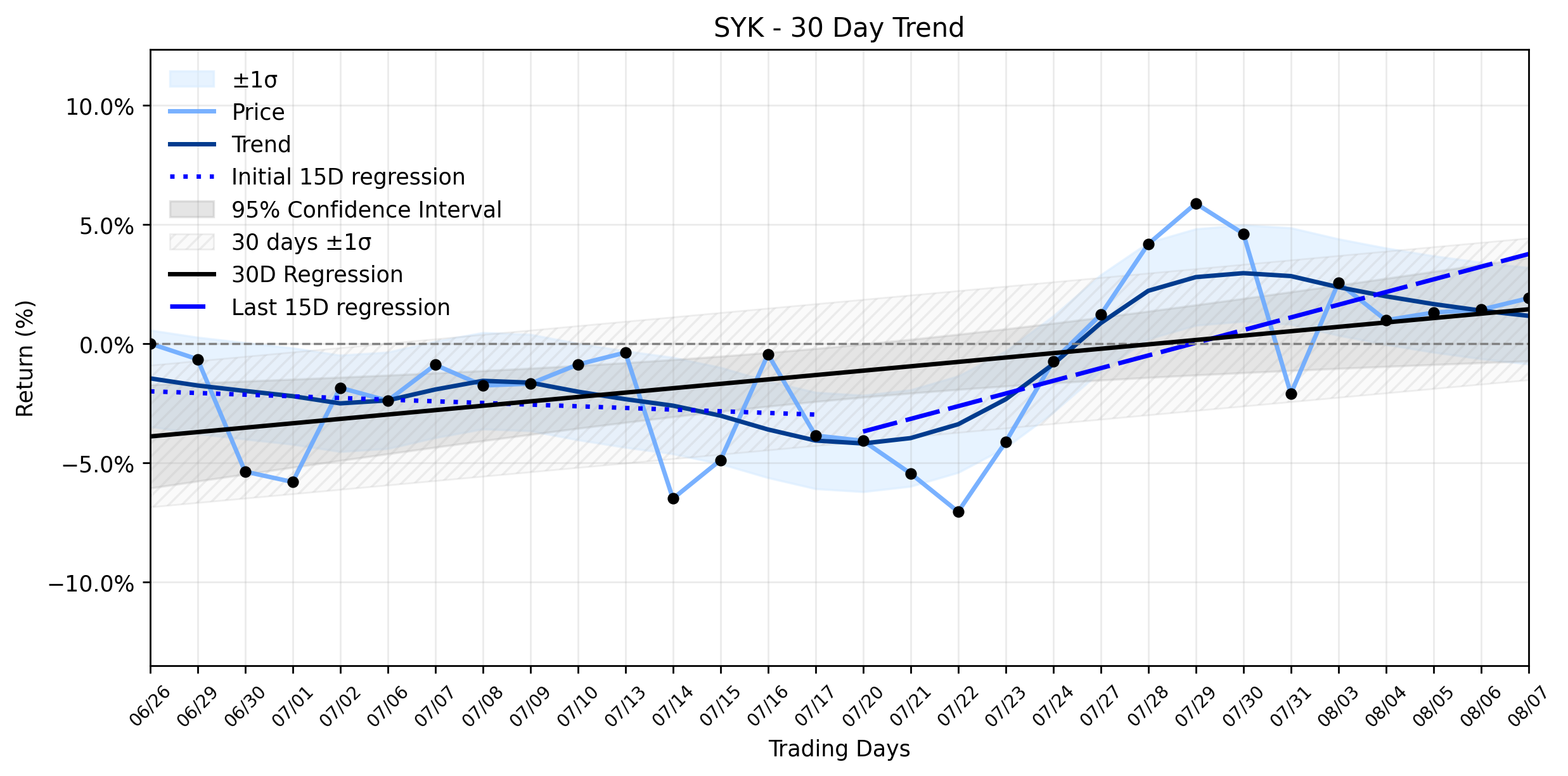

Stryker (SYK) Stages Gentle Advance as Robotics Innovation Fuels Stable Uptrend

Pct Price Change: 0.47%

- https://finance.yahoo.com/quote/SYK/

- www.marketbeat.com/instant-alerts/filing-stryker-corporation-syk-shares-acquired-by-professional-advisory-services-inc-2026-08-08/

- www.marketbeat.com/instant-alerts/filing-trust-point-inc-raises-holdings-in-stryker-corporation-syk-2026-08-08/

- investors.stryker.com/press-releases/news-details/2026/Stryker-declares-an-0-88-per-share-quarterly-dividend-cabaf911d/default.aspx

- www.stryker.com/us/en/about/news/index.html

- www.medtechdive.com/news/stryker-catching-up-on-orders-manufacturing-after-cyberattack/826725/

Darden Restaurants (DRI) Ignites an Uptrend Recovery: Is Insider Activity a Green Light or a Red Flag for This Culinary Colossus?

Pct Price Change: 1.34%

- https://finance.yahoo.com/quote/DRI/

- kalkinemedia.com/us/news/announcements/darden-restaurants-olive-garden-president-john-w-wilkerson-reports-august-2026-stock-option-exercise-and-sales

- ca.investing.com/news/stock-market-news/olive-garden-president-wilkerson-sells-18m-darden-restaurants-stock-93CH-4787370

- public.com/stocks/dri/forecast-price-target

- www.marketbeat.com/stocks/NYSE/DRI/forecast/

- www.investing.com/equities/dardem-rest

- www.stocktitan.net/news/DRI/

- www.seafoodsource.com/news/foodservice-retail/foot-traffic-rises-at-darden-s-upscale-chains-company-raises-fiscal-2026-outlook

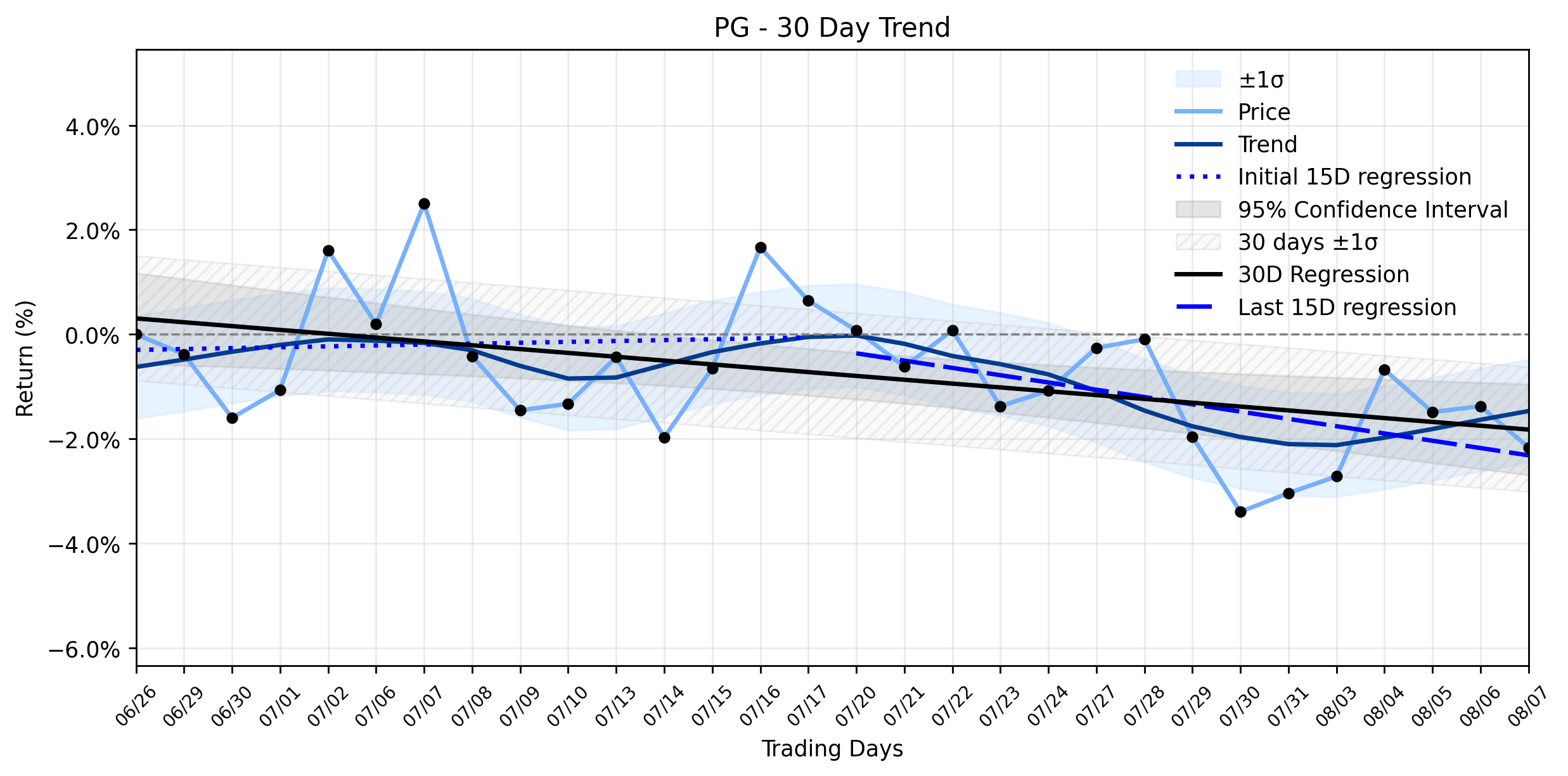

Hedge Funds Eye Procter & Gamble (PG) as Argus Downgrade Fuels Stable Downtrend: Is a Deeper Pullback Looming?

Pct Price Change: -0.80%

- https://finance.yahoo.com/quote/PG/

- ca.investing.com/news/stock-market-news/argus-downgrades-procter--gamble-stock-rating-to-hold-on-growth-93CH-4786859

- www.marketbeat.com/instant-alerts/procter-gamble-nysepg-stock-rating-lowered-by-argus-2026-08-07/

- simplywall.st/stocks/us/household/nyse-pg/procter-gamble/news/procter-gamble-pg-is-buying-thorne-for-38-billion-to-push-in

- www.barchart.com/story/news/3667266/a-3-8-billion-reason-why-procter-gamble-stock-is-in-focus-today

- www.sahi.com/blogs/pg-health-q1-results-2027

- www.stocktitan.net/overview/PG/

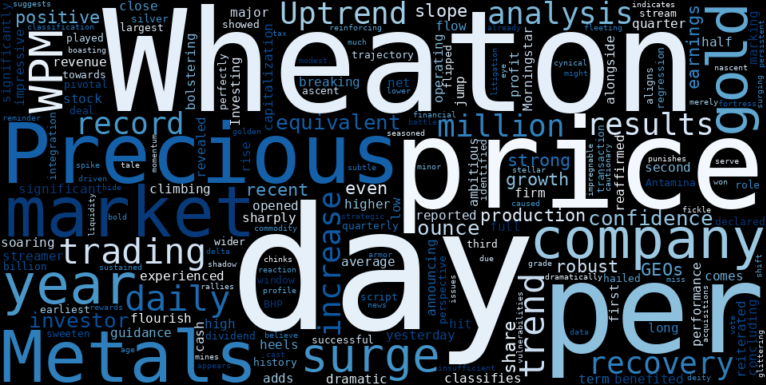

Wheaton Precious Metals (WPM) Sees Major Jump: Is This Uptrend Recovery a Red Flag for the Unwary?

Pct Price Change: 7.10%

- https://finance.yahoo.com/quote/WPM/

- ca.investing.com/news/company-news/wheaton-precious-metals-q2-2026-slides-record-revenue-major-deals-93CH-4787502

- global.morningstar.com/en-gb/news/alliance-news/1786090855527040500/wheaton-precious-net-profit-surges-amid-sharply-higher-gold-price

- www.morningstar.com/news/alliance-news/1786090855527040500/wheaton-precious-net-profit-surges-amid-sharply-higher-gold-price

- ca.investing.com/news/company-news/wheaton-precious-metals-corp-wpm-q2-2026-earnings-call-highlights-record-revenue-and--4787922

- seekingalpha.com/article/4933288-wheaton-precious-metals-corp-wpm-ca-q2-2026-earnings-call-transcript

- www.tradingview.com/news/urn:summary_document_transcript:quartr.com:3987900:0-wpm-record-breaking-h1-2026-with-strong-growth-major-streaming-deals-and-robust-financial-outlook/

- www.dividendinvestor.com/dividend-news/20260806/wheaton-precious-metals-corp-nyse-wpm-declared-a-dividend-of-$0.1950-per-share/

- www.tradingkey.com/news/market-movers/262089548-market-movers-wpm-20260807

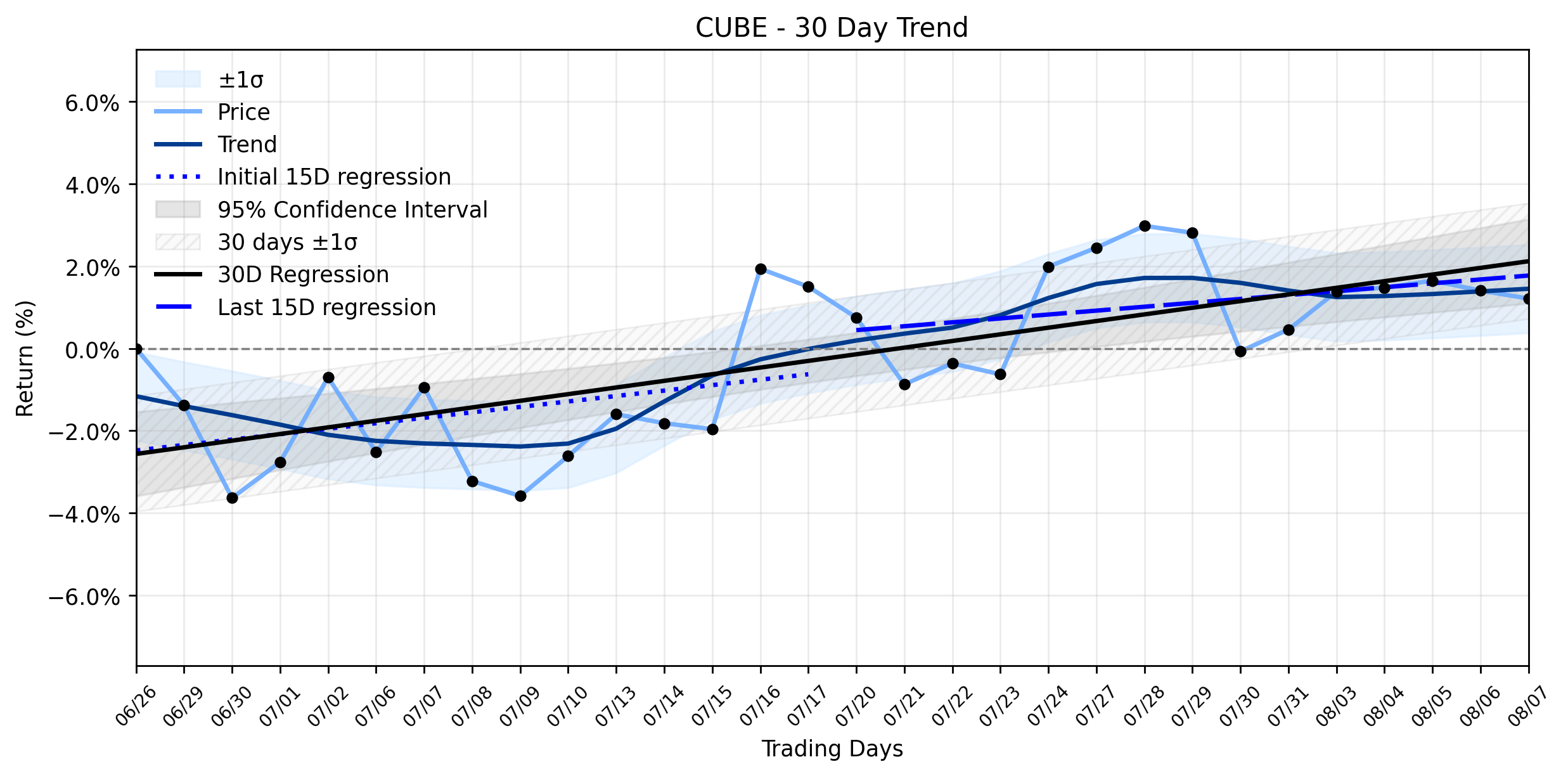

CubeSmart (CUBE) Takes a Modest Dip: Unpacking the Paradox of Missed Earnings and Raised Hopes

Pct Price Change: -0.19%

- https://finance.yahoo.com/quote/CUBE/

- www.marketbeat.com/instant-alerts/cubesmart-nysecube-given-consensus-rating-of-hold-by-brokerages-2026-08-07/

- www.mychesco.com/a/news/business/finance/cubesmart-raises-2026-outlook-as-storage-demand-improves/

- simplywall.st/stocks/us/real-estate/nyse-cube/cubesmart/news/will-strong-q2-results-buybacks-and-higher-guidance-change-c

- www.fool.com/earnings/call-transcripts/2026/08/07/cubesmart-cube-q2-2026-earnings-call-transcript/

- www.stocktitan.net/news/CUBE/

Southern Copper (SCCO) Sees Major Jump Amid Copper's Record Surge: Is This the Setup for a New Commodity Era?

Pct Price Change: 3.12%

- https://finance.yahoo.com/quote/SCCO/

- connectore.org/posts/copper-weekly-brief-7th-august-2026/

- www.mining.com/web/copper-market-crunch-brews-as-us-and-china-compete-for-metal/

- www.straitstimes.com/business/copper-heads-for-record-high-close-on-tighter-global-market

- news.metal.com/newscontent/104049346-copper-prices-near-record-high-amid-supply-tightness-and-strong-demand

- kalkinemedia.com/us/stocks/metal-and-mining/why-southern-copper-nysescco-keeps-drawing-market-attention-this-week

- www.finanzen.net/nachricht/rohstoffe/southern-copper-scco-is-a-top-ranked-growth-stock-should-you-buy-15857641

- www.marketbeat.com/instant-alerts/filing-beacon-investment-advisory-services-inc-raises-position-in-southern-copper-corporation-scco-2026-08-08/

- www.stocktitan.net/sec-filings/SCCO/form-4-southern-copper-corp-insider-trading-activity-869f9aee42c1.html

- www.cruxinvestor.com/posts/copper-deficit-deepens-on-chile-storms-drc-export-ban-what-confirms-the-rally

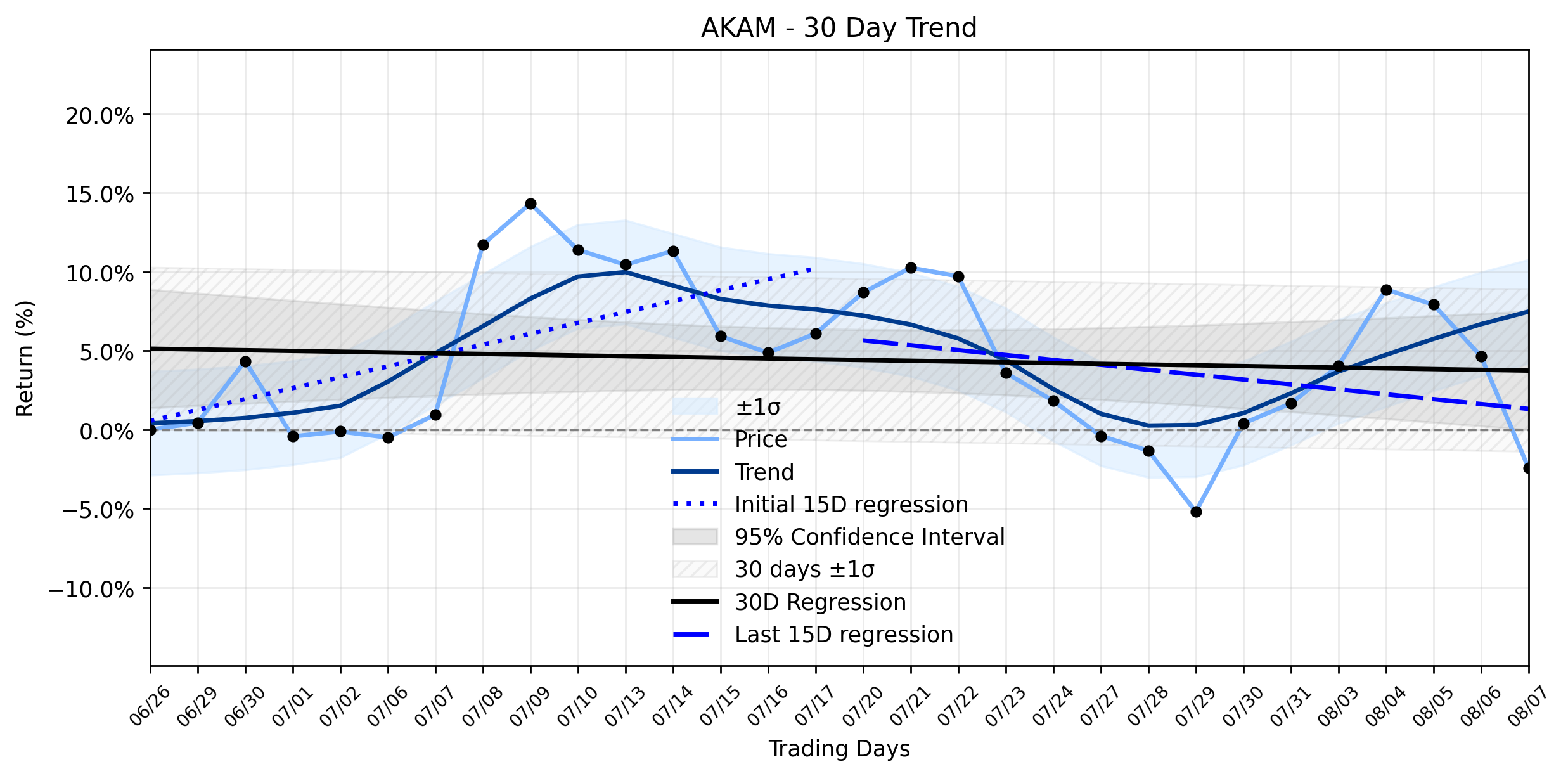

Akamai (AKAM) Takes a Textbook Tumble: Can a $600M AI Deal Halt the Downtrend's Fragile Stabilization?

Pct Price Change: -6.76%

- https://finance.yahoo.com/quote/AKAM/

- www.marketbeat.com/instant-alerts/akamai-technologies-nasdaqakam-given-new-14000-price-target-at-piper-sandler-2026-08-07/

- www.investing.com/news/transcripts/earnings-call-transcript-akamai-tops-q2-2026-estimates-as-stock-jumps-12-93CH-4844578

- www.marketbeat.com/instant-alerts/akamai-technologies-nasdaqakam-trading-down-63-following-analyst-downgrade-2026-08-07/

- investingnews.com/akamai-reports-second-quarter-2026-financial-results/

- seekingalpha.com/article/4933138-akamai-technologies-strong-ai-led-growth-turbulent-profitability

- seekingalpha.com/news/4628707-akamai-anticipates-low-teens-revenue-growth-in-2027-backed-by-2_8b-cis-commitments

- seekingalpha.com/news/4628230-akamais-q2-results-feature-rapid-growth-in-its-new-cloud-infrastructure-services-business

- markets.financialcontent.com/stocks/article/stockstory-2026-8-7-why-akamai-akam-shares-are-trading-lower-today

Liberty Media's Formula One (FWONA) Defies Revenue Plunge with a Sharp Rise: Is the Uptrend Stabilizing or is Vulnerability Brewing?

Pct Price Change: 2.96%

- https://finance.yahoo.com/quote/FWONA/

- thejudge13.com/2026/08/07/f1-revenue-plunges-15-as-cancelled-races-leave-liberty-media-244-million-short/

- www.gurufocus.com/news/9013308/is-liberty-media-corp-fwona-facing-challenges-after-q2-earnings-miss-gf-score-83100

- www.libertymedia.com/investors/news-events/press-releases/detail/587/liberty-media-corporation-reports-second-quarter-2026

- www.marketbeat.com/instant-alerts/filing-liberty-media-corporation-liberty-formula-one-series-a-fwona-shares-sold-by-amundi-2026-08-08/

- www.marketbeat.com/instant-alerts/liberty-media-corporation-liberty-formula-one-series-c-nasdaqfwonk-given-new-10500-price-target-at-wells-fargo-company-2026-08-07/

- www.gurufocus.com/news/9015108/fwona-swot-analysis-liberty-media-corps-financial-resilience-revealed-in-10q-filing

- www.gurufocus.com/news/9013951/a-look-at-liberty-media-corp-fwona-after-32-gain-gf-value-9444-vs-price-9126

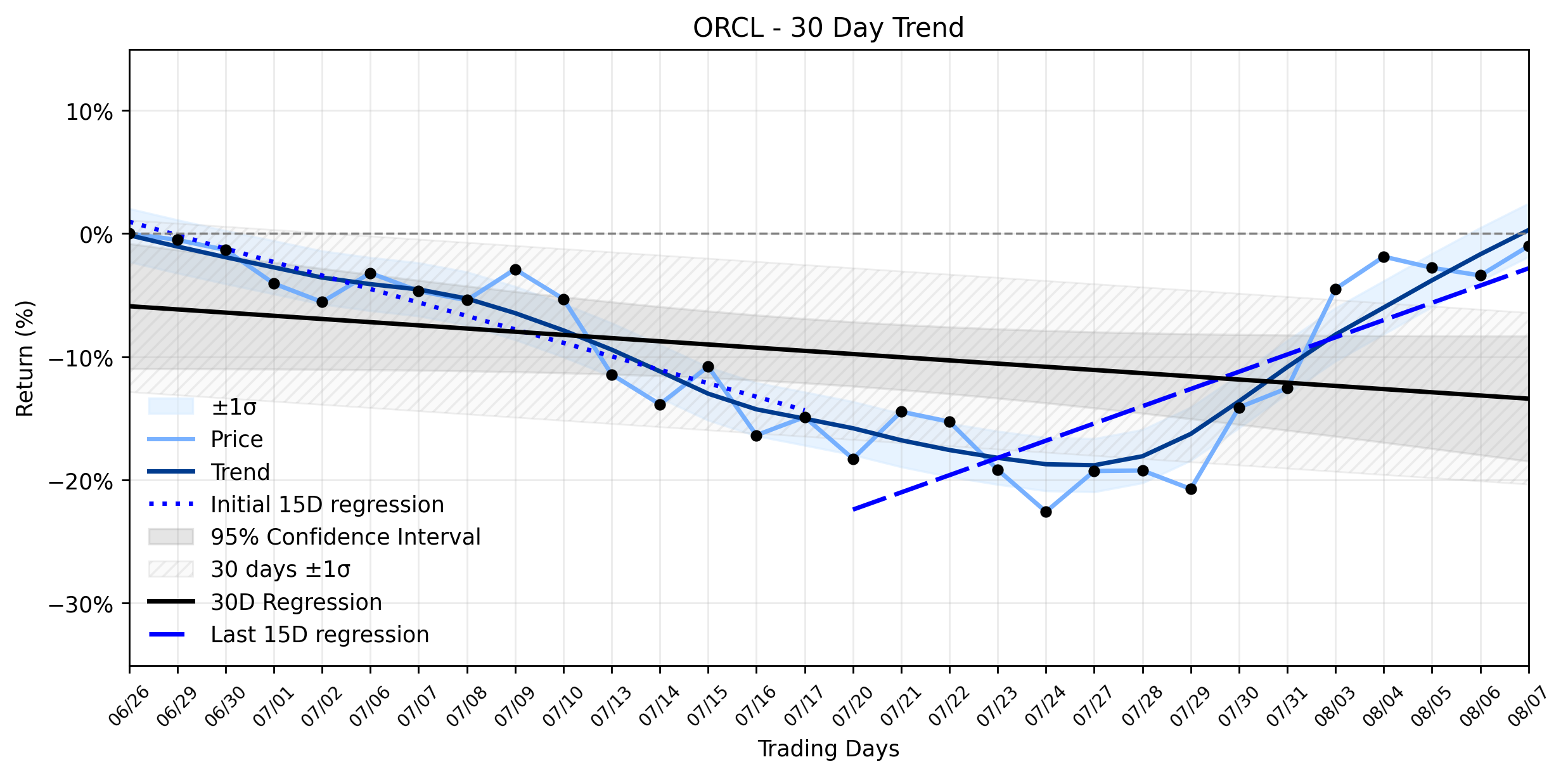

Oracle (ORCL) Stages a Notable Rally: Is Smart Money Betting on AI Growth, or Just a Debt-Fueled Mirage?

Pct Price Change: 2.47%

- https://finance.yahoo.com/quote/ORCL/

- simplywall.st/stocks/us/software/nyse-orcl/oracle/news/oracle-orcl-could-be-26-below-fair-value-as-contract-news-re

- www.fool.com/investing/2026/08/07/oracle-surges-whats-driving-the-sudden-rally/

- www.tradingkey.com/analysis/stocks/us-stocks/262073122-oracle-orcl-stock-forecast-august-4-2026-638b-backlog-recovery-google-tradingkey

- www.barchart.com/story/news/3718939/the-curious-case-of-oracle-stock-the-better-the-business-gets-the-more-investors-worry

- www.marketbeat.com/instant-alerts/oracle-nyseorcl-stock-price-up-24-time-to-buy-2026-08-07/

- 247wallst.com/investing/2026/08/03/oracle-is-still-down-28-this-year-what-will-it-take-to-get-orcl-stock-back-to-200/

- www.thestreet.com/investing/stocks/orcl-oracle-nbis-nebius-michael-burry-shorts

Okta (OKTA) Stages Powerful Rally: Is AI-Driven Growth a Confirmation, or Just a Mirage Amidst Overvaluation?

Pct Price Change: 3.35%

- https://finance.yahoo.com/quote/OKTA/

- www.zacks.com/stock/news/2970695/zacks-industry-outlook-palo-alto-networks-fortinet-and-okta

- seekingalpha.com/article/4929695-okta-the-next-growth-phase-may-come-from-non-human-origins

- www.zacks.com/stock/news/2970440/why-okta-okta-dipped-more-than-broader-market-today?cid=CS-ZC-FT-fundamental_analysis%7Cyseop_template_6v1-2970440

- investor.okta.com/news-and-events/news-releases/default.aspx

- www.stockwatch.com/News/Item/U-b20260801555265-U!OKTA-20260801/U/OKTA

- www.gurufocus.com/news/9018581/okta-inc-okta-shares-surge-34-what-gf-score-of-73-tells-investors

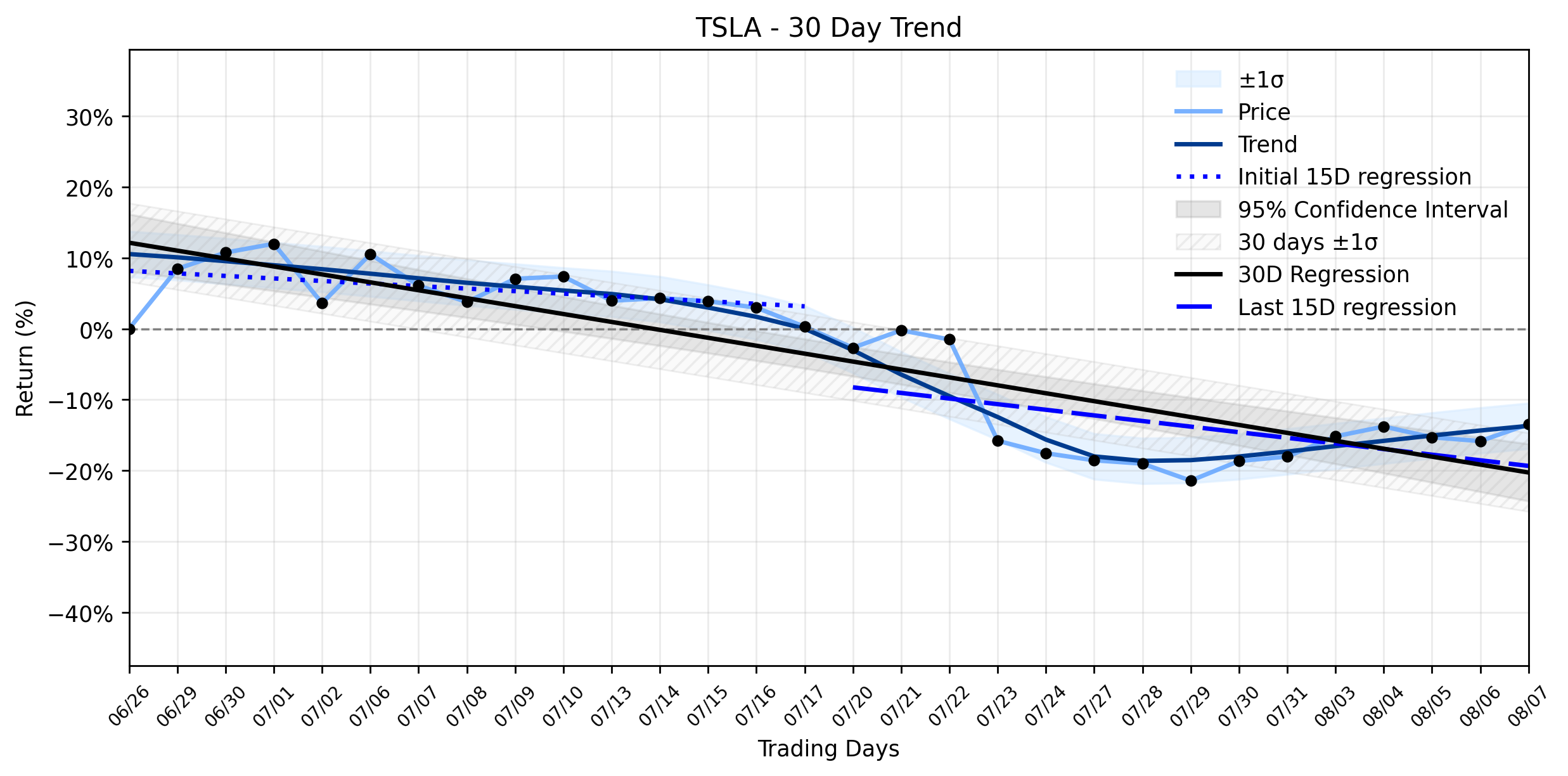

The Quiet Battle: Is Tesla (TSLA)'s Impressive Gain Masking a Deeper Trend Shift?

Pct Price Change: 2.83%

- https://finance.yahoo.com/quote/TSLA/

- www.marketbeat.com/instant-alerts/tesla-nasdaqtsla-trading-up-28-whats-next-2026-08-07/

- www.wfaa.com/article/money/business/houston-tesla-fort-bend-county/285-a4c1442f-258b-4371-90c4-57d9469ff7ae

- www.tradingkey.com/news/market-movers/262089226-market-movers-tsla-20260807

- www.zacks.com/stock/news/2970680/the-zacks-analyst-blog-highlights-tesla-and-spacex

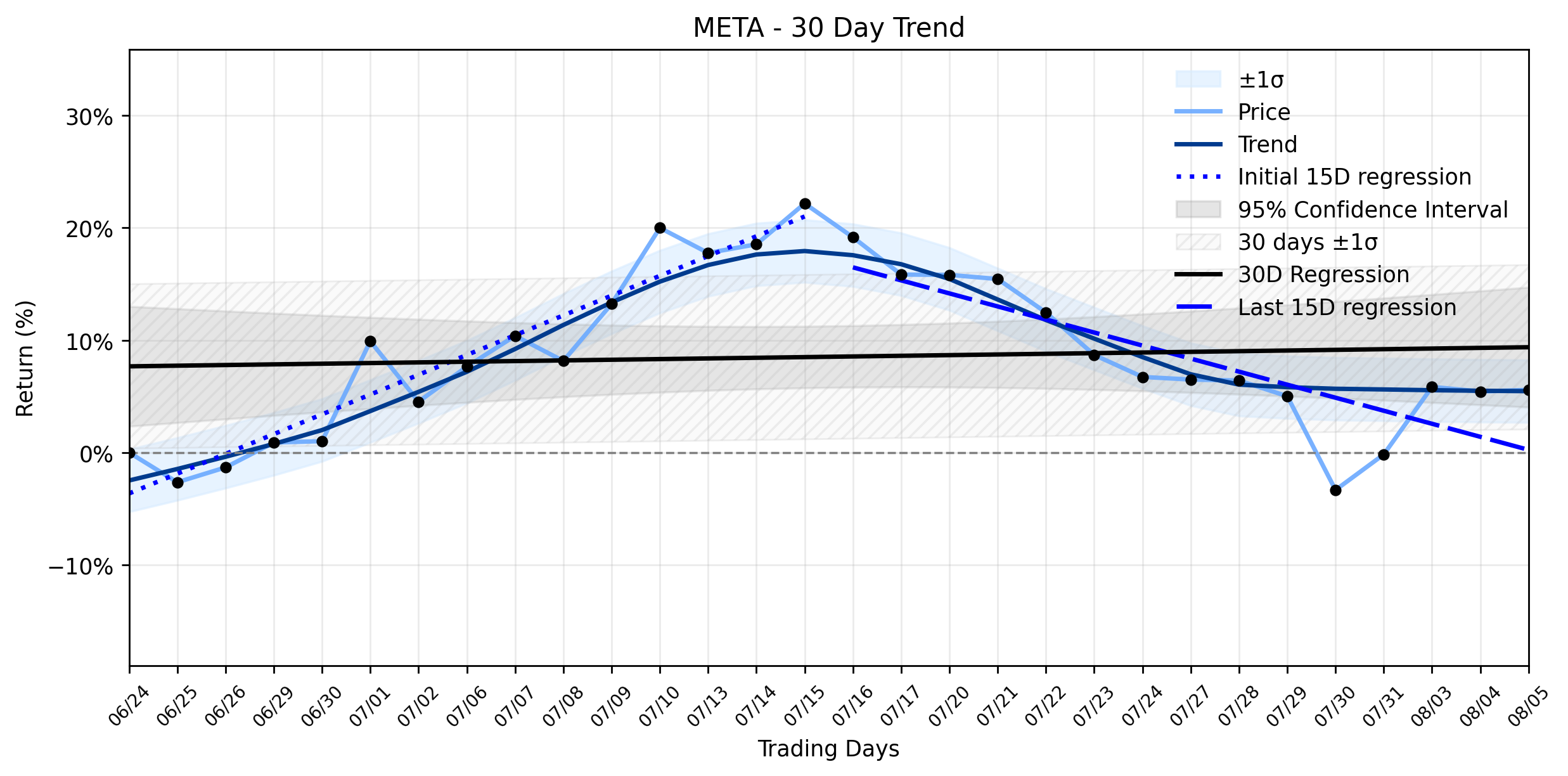

Meta Platforms (META) Navigates a $942 Million Legal Minefield: An AI Efficiently Distills Why the Stock Saw a Gentle Advance Amidst a Stabilizing Downtrend

Pct Price Change: 0.37%

- https://finance.yahoo.com/quote/META/

- gizmodo.com/meta-officially-ruled-a-public-nuisance-judge-orders-it-to-pay-567-million-2000795880

- www.malwarebytes.com/blog/uncategorized/2026/08/meta-ordered-to-pay-942-million-over-harm-to-children

- thedailyrecord.com/2026/08/07/meta-ordered-to-pay-567m-in-nm-for-teen-mental-health-fund/

- wtaq.com/2026/08/07/explainer-how-could-new-mexicos-567-million-ruling-change-meta/

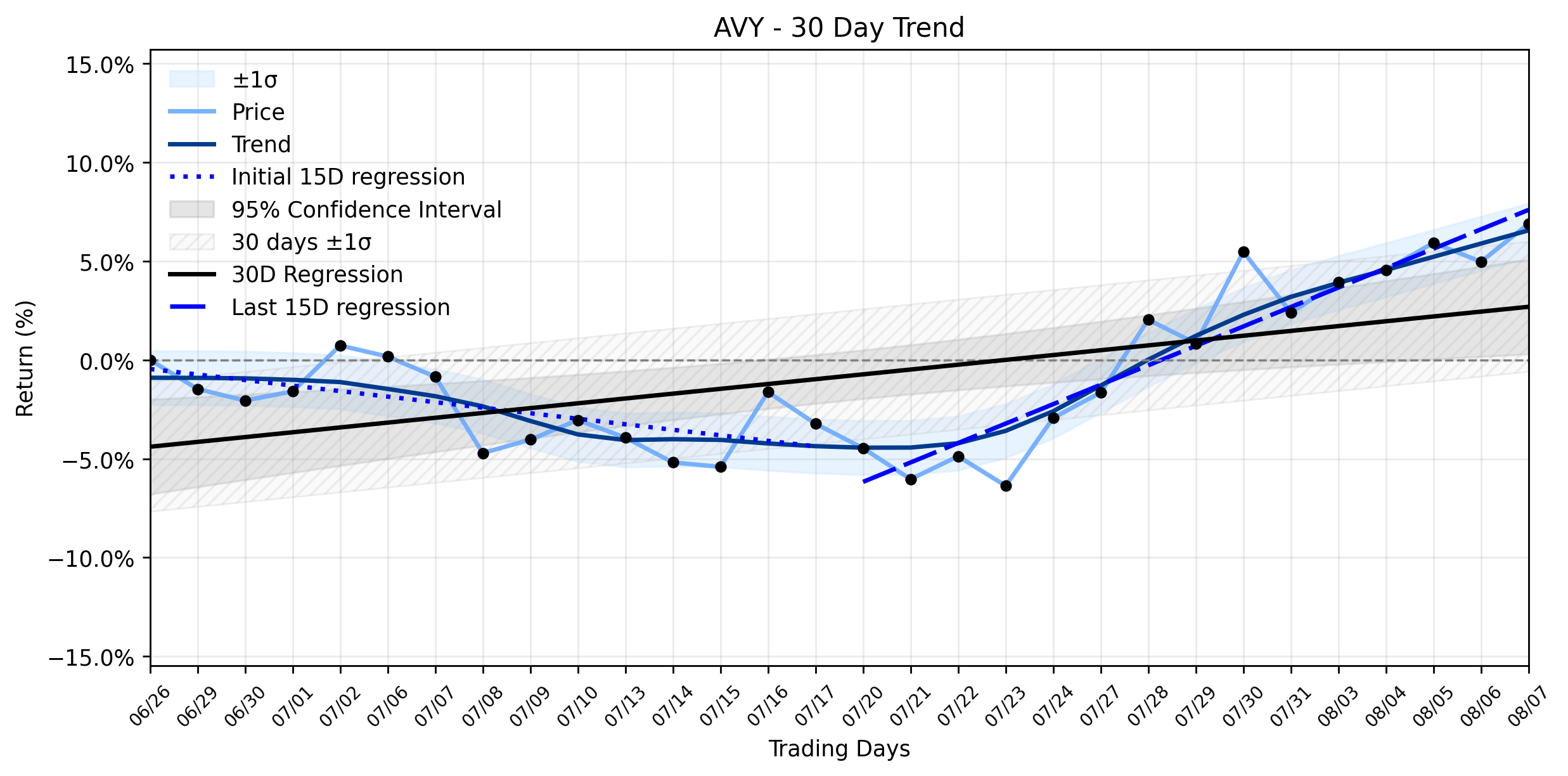

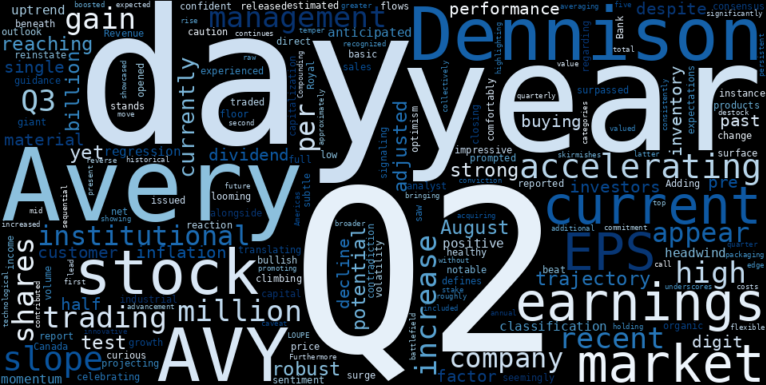

Avery Dennison (AVY) Stages a Notable Rally: Is the "Uptrend Recovery" Strong Enough to Conquer Q3 Headwinds?

Pct Price Change: 1.83%

- https://finance.yahoo.com/quote/AVY/

- www.marketbeat.com/instant-alerts/avery-dennison-nyseavy-updates-q3-2026-earnings-guidance-2026-07-30/

- www.marketbeat.com/instant-alerts/filing-avery-dennison-corporation-avy-shares-sold-by-bank-of-america-corp-de-2026-08-07/

- markets.chroniclejournal.com/chroniclejournal/article/stockstory-2026-8-6-the-5-most-interesting-analyst-questions-from-avery-dennisons-q2-earnings-call

- www.averydennison.com/en/home/news/press-releases/avery-dennison-announces-q2-2026-results.html

- simplywall.st/stocks/us/materials/nyse-avy/avery-dennison/news/avery-dennison-avy-stock-drops-as-margin-gains-meet-prebuy-r

- seekingalpha.com/news/4622043-avery-dennison-anticipates-10-to-10_30-in-2026-adjusted-eps-on-3-percent-to-4-percent-organic

- www.fool.com/earnings/call-transcripts/2026/08/03/avery-dennison-avy-q2-2026-earnings-call-transcript/

- www.marketscreener.com/news/avery-dennison-corporation-provides-earnings-guidance-for-the-full-year-2026-ce7f50dada8afe20

- www.barchart.com/stocks/quotes/AVY/analyst-ratings

- public.com/stocks/avy/forecast-price-target

- www.marketbeat.com/stocks/NYSE/AVY/

- www.tipranks.com/stocks/avy/forecast

- www.investing.com/equities/avery-dennison-consensus-estimates

Targa Resources (TRGP) Takes a Sudden Tumble: Why Record Earnings Couldn't Halt a Fragile Downtrend

Pct Price Change: -4.24%

- https://finance.yahoo.com/quote/TRGP/

- www.marketbeat.com/instant-alerts/targa-resources-nysetrgp-given-new-28200-price-target-at-wells-fargo-company-2026-08-07/

- www.marketbeat.com/instant-alerts/td-cowen-issues-positive-forecast-for-targa-resources-nysetrgp-stock-price-2026-08-07/

- www.marketbeat.com/instant-alerts/targa-resources-nysetrgp-posts-quarterly-earnings-results-beats-estimates-by-071-eps-2026-08-07/

- www.globenewswire.com/news-release/2026/08/06/3340017/14074/en/Targa-Resources-Corp-Reports-Record-Second-Quarter-2026-Financial-Results.html

- www.industrialinfo.com/news/article/ngl-demand-pushes-targa-to-add-permian-pipelines-processing--361127

- seekingalpha.com/news/4628216-targa-expects-2026-adjusted-ebitda-toward-top-end-of-5_7b-5_9b-range-as-permian-volumes-rise

- www.investing.com/news/analyst-ratings/raymond-james-raises-targa-resources-stock-price-target-on-strong-results-93CH-4845670

- simplywall.st/stocks/us/energy/nyse-trgp/targa-resources/news/is-targa-resources-trgp-undervalued-after-strong-q2-earnings

- www.gurufocus.com/news/9013885/targa-resources-corp-trgp-shares-surge-31-what-gf-score-of-74-tells-investors

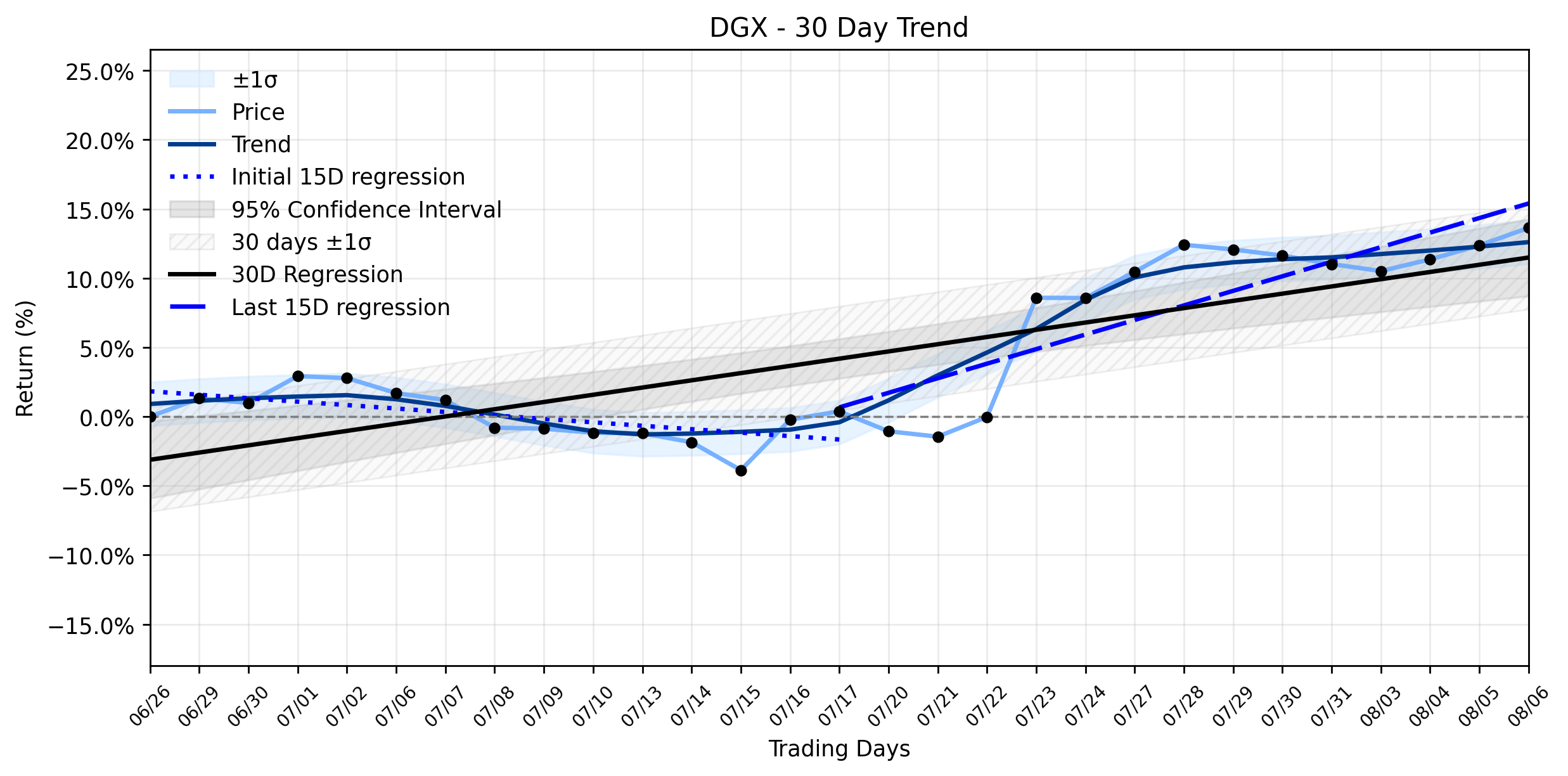

Quest Diagnostics (DGX) Stages a High-Stakes Advance: Is the Uptrend Recovery Masking a Deeper Institutional Play?

Pct Price Change: 1.13%

- https://finance.yahoo.com/quote/DGX/

- news.stocktradersdaily.com/news_release/141/Understanding_Momentum_Shifts_in_DGX_080626011601_1785993361.html

- www.marketbeat.com/instant-alerts/filing-quest-diagnostics-incorporated-dgx-holdings-trimmed-by-empowered-funds-llc-2026-08-07/

- newsroom.questdiagnostics.com/2026-07-23-Quest-Diagnostics-Reports-Second-Quarter-2026-Financial-Results-Raises-Revenue-and-EPS-Guidance-for-Full-Year-2026

- simplywall.st/stocks/us/healthcare/nyse-dgx/quest-diagnostics/news/quest-diagnostics-dgx-lifts-2026-outlook-as-investors-ask-if

Nu Skin Enterprises (NUS) Registers Another Decline: Is This Sideways Drift a Signal of Undervalued Potential or a Premonition of Further Losses?

Pct Price Change: -0.57%

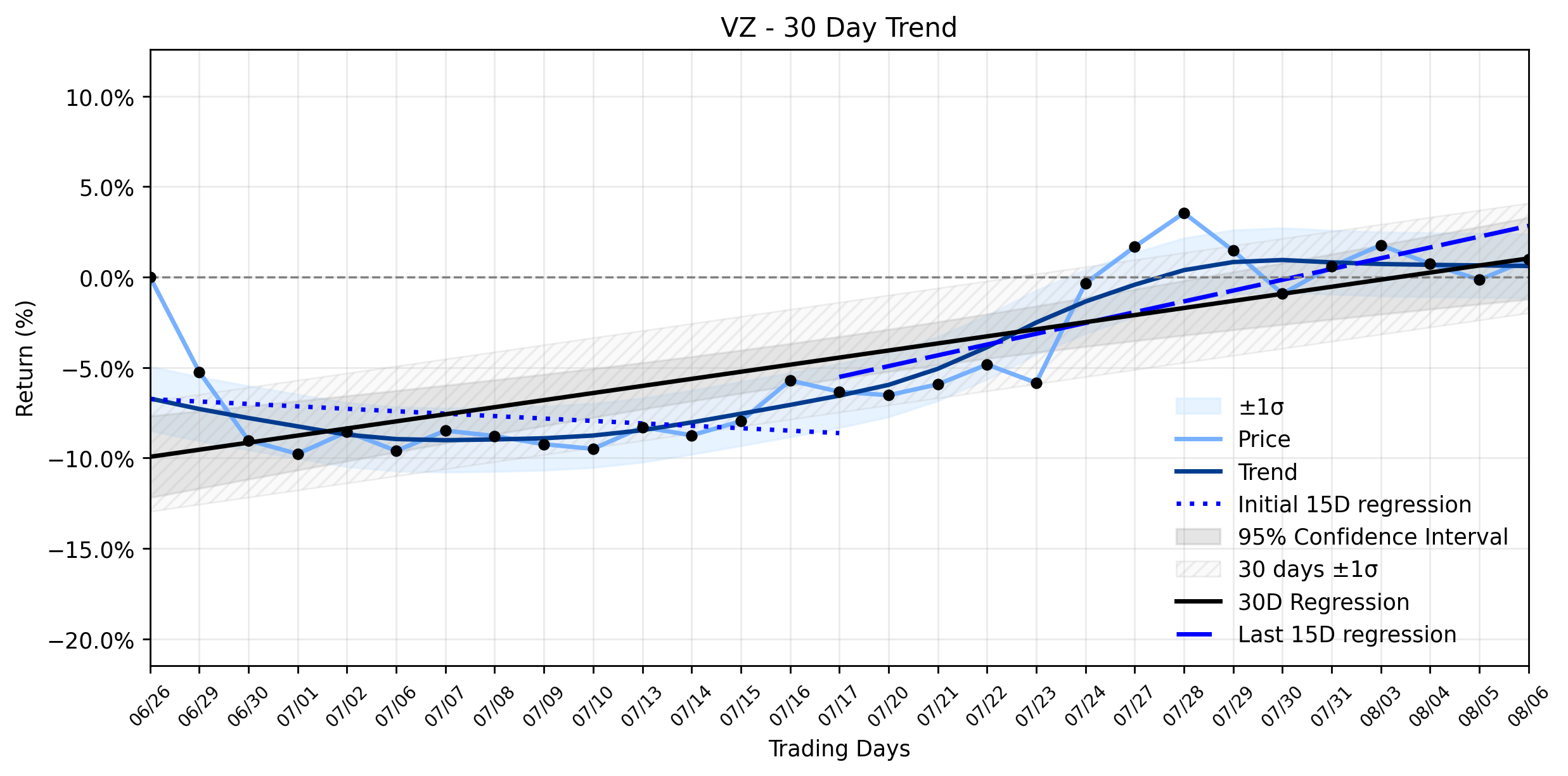

Verizon (VZ) Accumulation: Is Smart Money Betting on a Strategic Rise Amidst Telecom Turbulence?

Pct Price Change: 1.12%

- https://finance.yahoo.com/quote/VZ/

- www.cnet.com/tech/mobile/verizon-switches-focus-to-new-simplicity-phone-plan-heres-what-youre-paying-for/

- www.verizon.com/about/news

- broadbandbreakfast.com/verizon-to-cut-500-jobs-sell-274-stores/

- www.fastcompany.com/91575600/verizon-layoffs-today-more-jobs-slashed-2026-retail-store-shift

- www.tradingview.com/news/zacks:4bdbda2ea094b:0-verizon-announces-new-layoffs-as-cost-cutting-continues-into-2026/

- simplywall.st/stocks/us/telecom/nyse-vz/verizon-communications/news/verizon-communications-vz-on-spacex-mobile-threat-still-look

- www.morningstar.com/stocks/after-earnings-is-verizon-stock-buy-sell-or-fairly-valued-12

- www.barchart.com/story/news/3564863/heres-why-verizon-stock-is-a-buy-for-income-investors-in-august

- seekingalpha.com/news/4618256-verizon-forecasts-9-percentminus-10-percent-2026-free-cash-flow-growth-while-lifting-buybacks

CooperCompanies (COO) Sees Significant Retreat: Is the Stable Uptrend Developing a Crack, or Just a Pause Before Q3?

Pct Price Change: -2.03%

- https://finance.yahoo.com/quote/COO/

- www.zacks.com/stock/news/2968948/the-cooper-companies-coo-upgraded-to-buy-heres-what-you-should-know

- www.stocktitan.net/news/COO/

- www.stocktitan.net/news/COO/cooper-companies-announces-release-date-for-third-quarter-ya4gxj2h527f.html

- www.barchart.com/story/news/3561227/coopercompanies-announces-release-date-for-third-quarter-2026

- www.perplexity.ai/finance/COO

- public.com/stocks/coo/forecast-price-target

- timothysykes.com/news/thecoopercompaniesinc-coo-news-2026_06_06/

- stockstotrade.com/news/thecoopercompaniesinc-coo-news-2026_06_06/

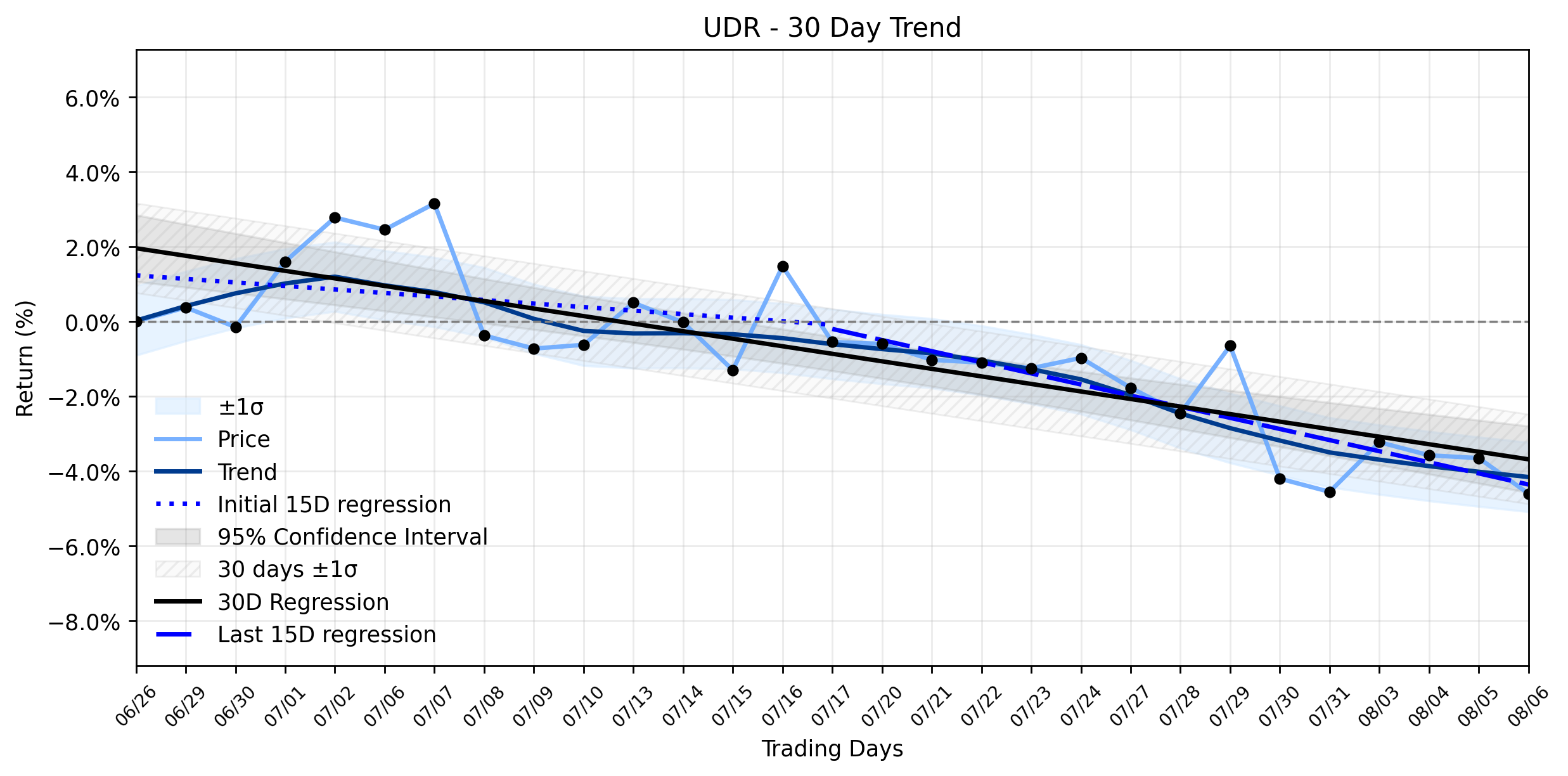

UDR's (UDR) Persistent Slide: What the Stable Downtrend Conceals Amidst Strong Earnings and Analyst Discord

Pct Price Change: -0.99%

- https://finance.yahoo.com/quote/UDR/

- www.marketbeat.com/instant-alerts/united-dominion-realty-trust-inc-nyseudr-receives-consensus-recommendation-of-hold-from-brokerages-2026-08-07/

- www.stocktitan.net/news/UDR/

- public.com/stocks/udr/forecast-price-target

- www.marketbeat.com/stocks/NYSE/UDR/forecast/

- robinhood.com/us/en/stocks/UDR/

Brookfield Renewable (BEP): What's Fueling the Quiet Climb Beneath the Surface of Q2's Mixed Signals?

Pct Price Change: 0.09%

- https://finance.yahoo.com/quote/BEP/

- solarquarter.com/2026/08/03/brookfield-renewable-reports-record-q2-2026-ffo-expands-battery-storage-portfolio-with-aypa-acquisition/

- bep.brookfield.com/press-releases/bep/brookfield-renewable-reports-strong-second-quarter-results

- www.stocktitan.net/sec-filings/BEP/6-k-brookfield-renewable-partners-l-p-current-report-foreign-issuer-f9ca40c5e9fa.html

- seekingalpha.com/article/4931754-brookfield-renewable-q2-reiterating-a-buy-despite-ongoing-net-losses-here-is-why?source=generic_rss

- www.fool.com/investing/2026/08/06/2-nuclear-energy-stocks-to-buy-hand-over-fist-in/

- www.marketbeat.com/instant-alerts/brookfield-renewable-partners-nysebep-price-target-lowered-to-3700-at-national-bank-financial-2026-08-05/

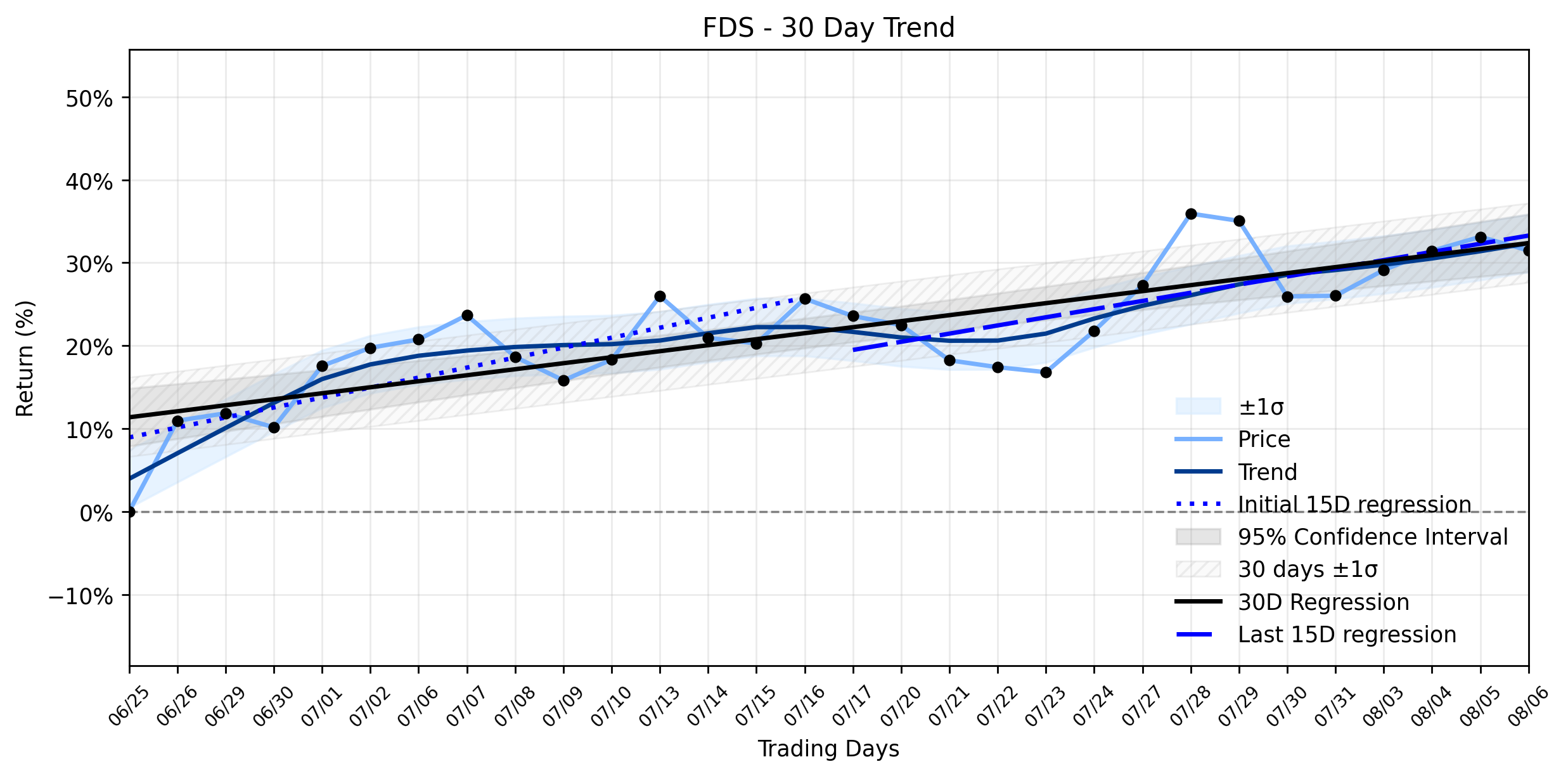

FactSet (FDS): Institutional Capital Flows Shift as Shares Dip, Testing a Stable Uptrend's Resolve

Pct Price Change: -1.24%

AI-Powered Insight: Shell (SHEL) Stages a Solid Advance Amidst Strategic Portfolio Reshaping – But What's Behind the Weakening Uptrend?

Pct Price Change: 2.10%

- https://finance.yahoo.com/quote/SHEL/

- kalkinemedia.com/uk/news/announcements/shell-plc-shel-completes-buyback-of-1625-million-shares-on-august-5-2026-across-lse-and-amsterdam-markets

- kalkinemedia.com/uk/news/announcements/shell-plc-shel-executes-buyback-of-1625-million-shares-on-august-4-2026-under-goldman-sachs-managed-program

- simplywall.st/stocks/gb/energy/lse-shel/shell-shares/news/what-does-shell-lseshel-exit-from-cyprus-gas-mean-for-invest

- carboncredits.com/shell-sells-totalenergies-buys-the-energy-giants-biggest-renewables-deal/

- splash247.com/shell-greenlights-next-phase-of-malaysian-deepwater-field/

- www.zacks.com/research-daily/2969575/top-research-reports-for-apple-shell-toyota-motor

- www.zacks.com/stock/news/2970685/the-zacks-analyst-blog-highlights-apple-shell-toyota-seneca-and-value-line

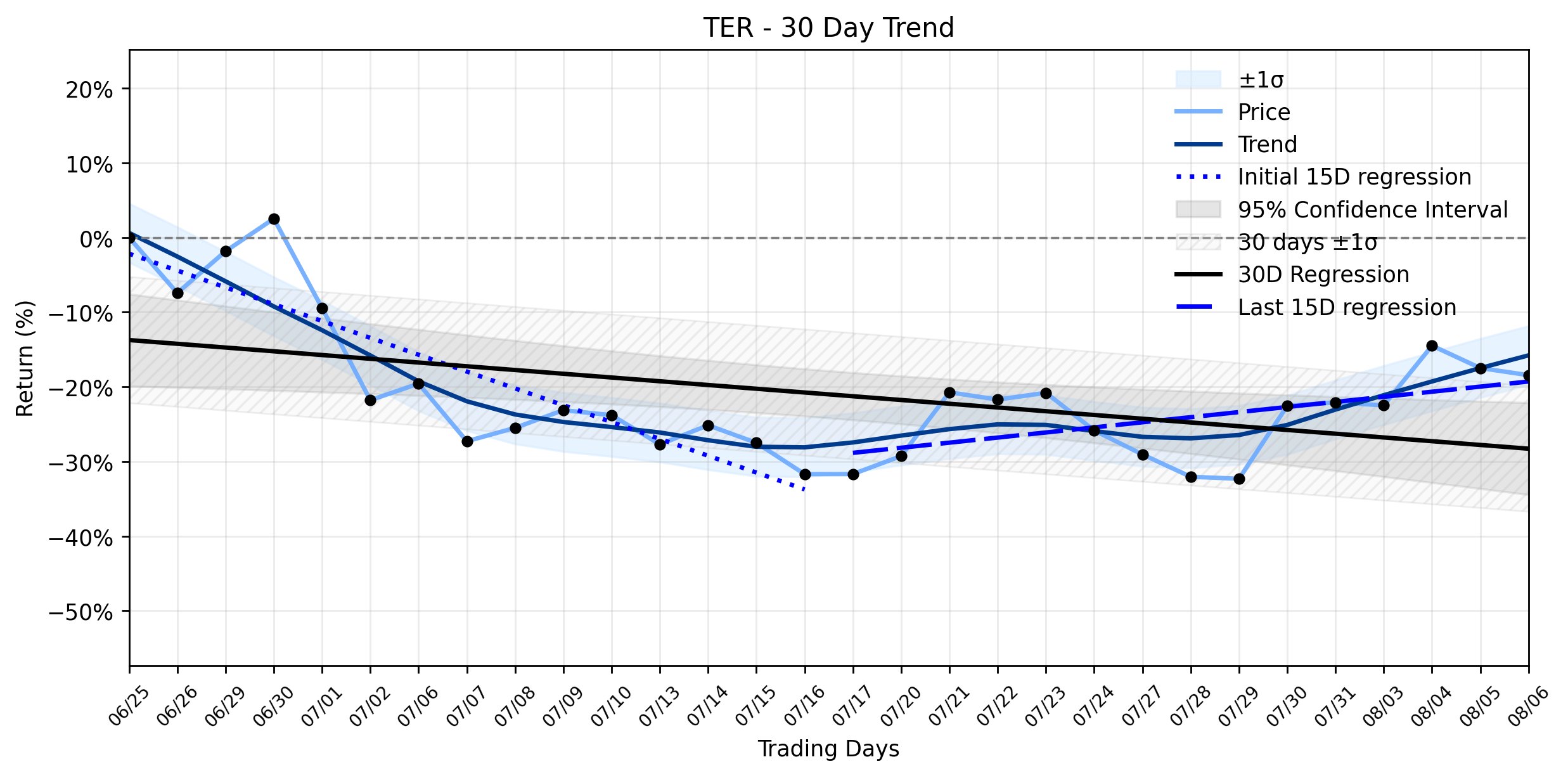

What Teradyne's (TER) Recent Decline *Really* Revealed About Its AI-Driven Uptrend

Pct Price Change: -1.16%

- https://finance.yahoo.com/quote/TER/

- www.marketbeat.com/instant-alerts/teradyne-inc-nasdaqter-given-consensus-rating-of-moderate-buy-by-brokerages-2026-08-06/

- www.marketbeat.com/instant-alerts/filing-teradyne-inc-ter-shares-acquired-by-corecap-advisors-llc-2026-08-06/

- www.gurufocus.com/news/9009132/blackrock-inc-adds-to-teradyne-inc-ter-stake-shares-trade-91-above-gf-value

- simplywall.st/stocks/us/semiconductors/nasdaq-ter/teradyne/news/teradyne-ter-stock-looks-rich-after-a-272-run

Smart Money's Sudden Retreat: Did Dell Technologies (DELL) Tumble Signal a Deeper AI Margin Squeeze, or Just Profit-Taking in a Stable Uptrend?

Pct Price Change: -5.41%

- https://finance.yahoo.com/quote/DELL/

- www.tradingkey.com/news/market-movers/262084322-market-movers-dell-20260806

- www.zacks.com/stock/news/2970392/dell-technologies-dell-dips-more-than-broader-market-what-you-should-know

- www.marketbeat.com/instant-alerts/dell-technologies-nysedell-shares-down-51-should-you-sell-2026-08-06/

- www.marketbeat.com/instant-alerts/filing-dell-technologies-inc-dell-shares-sold-by-mirador-capital-partners-lp-2026-08-06/

- www.barchart.com/story/news/3698748/after-a-250-rally-dell-stock-still-has-room-to-run-here-s-why

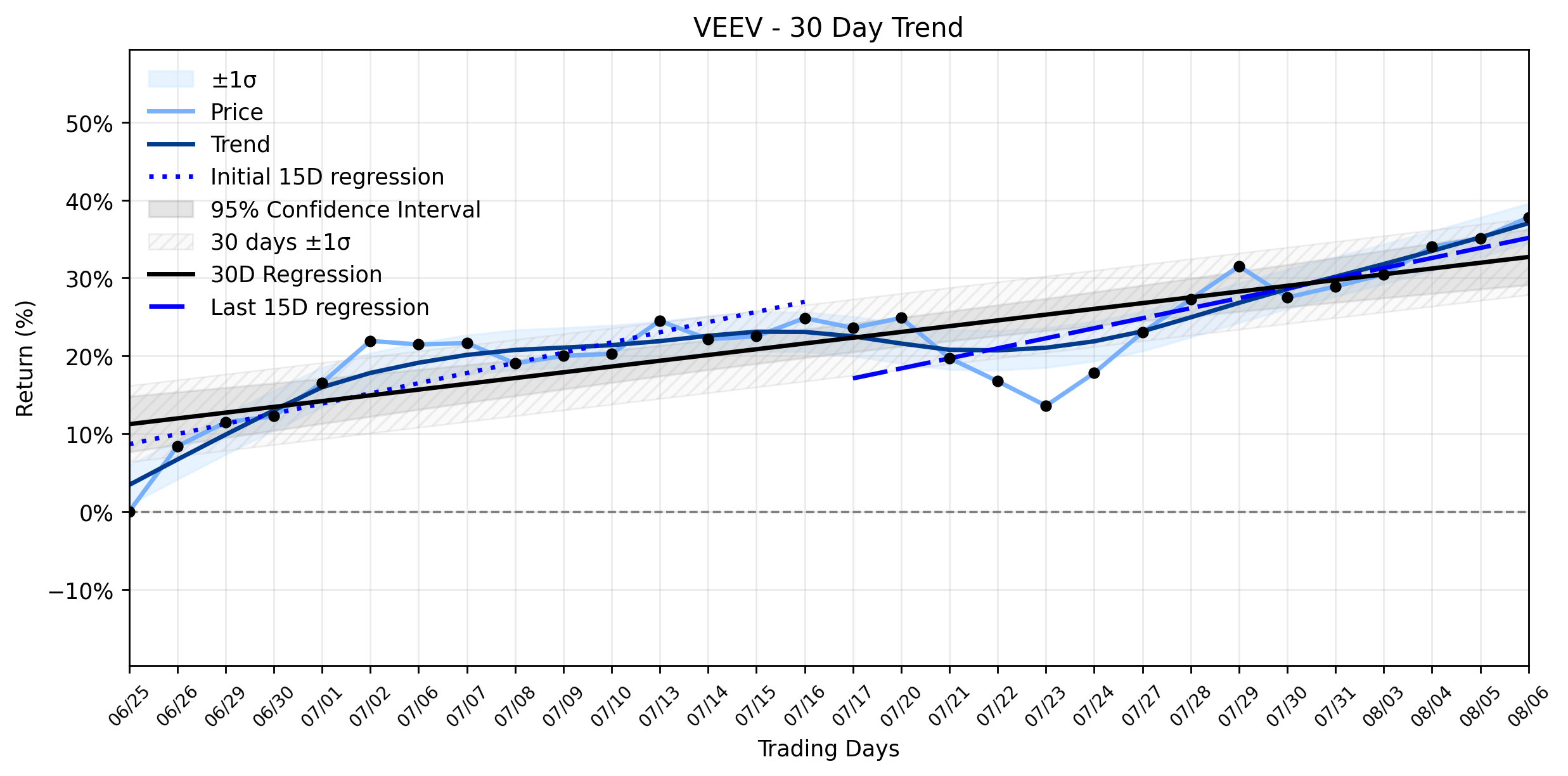

Veeva Systems (VEEV) Defies Market Dip: Is This Healthy Climb Hiding a Potential Downside?

Pct Price Change: 2.01%

- https://finance.yahoo.com/quote/VEEV/

- www.zacks.com/stock/news/2970390/why-the-market-dipped-but-veeva-systems-veev-gained-today

- ground.news/article/veeva-to-release-fiscal-2027-second-quarter-results-on-august-26-2026_6783df

- www.morningstar.com/news/pr-newswire/20260805sf19361/veeva-to-release-fiscal-2027-second-quarter-results-on-august-26-2026

- www.stocktitan.net/news/VEEV/veeva-to-release-fiscal-2027-second-quarter-results-on-august-26-80f44mcfu3hq.html

- tucson.com/online_features/press_releases/article_f467c479-08f9-5d46-809c-4be02ce43670.html

- www.gurufocus.com/news/9009190/blackrock-inc-adds-to-veeva-systems-inc-veev-stake-shares-look-27-undervalued-on-gf-value

- public.com/stocks/veev/forecast-price-target

- tickernerd.com/stock/veev-forecast/

Tenaris S.A. (TS) Plunges Despite Earnings Beat: Are Capital Flows Signaling a Crushing Blow to its Stable Uptrend?

Pct Price Change: -6.40%

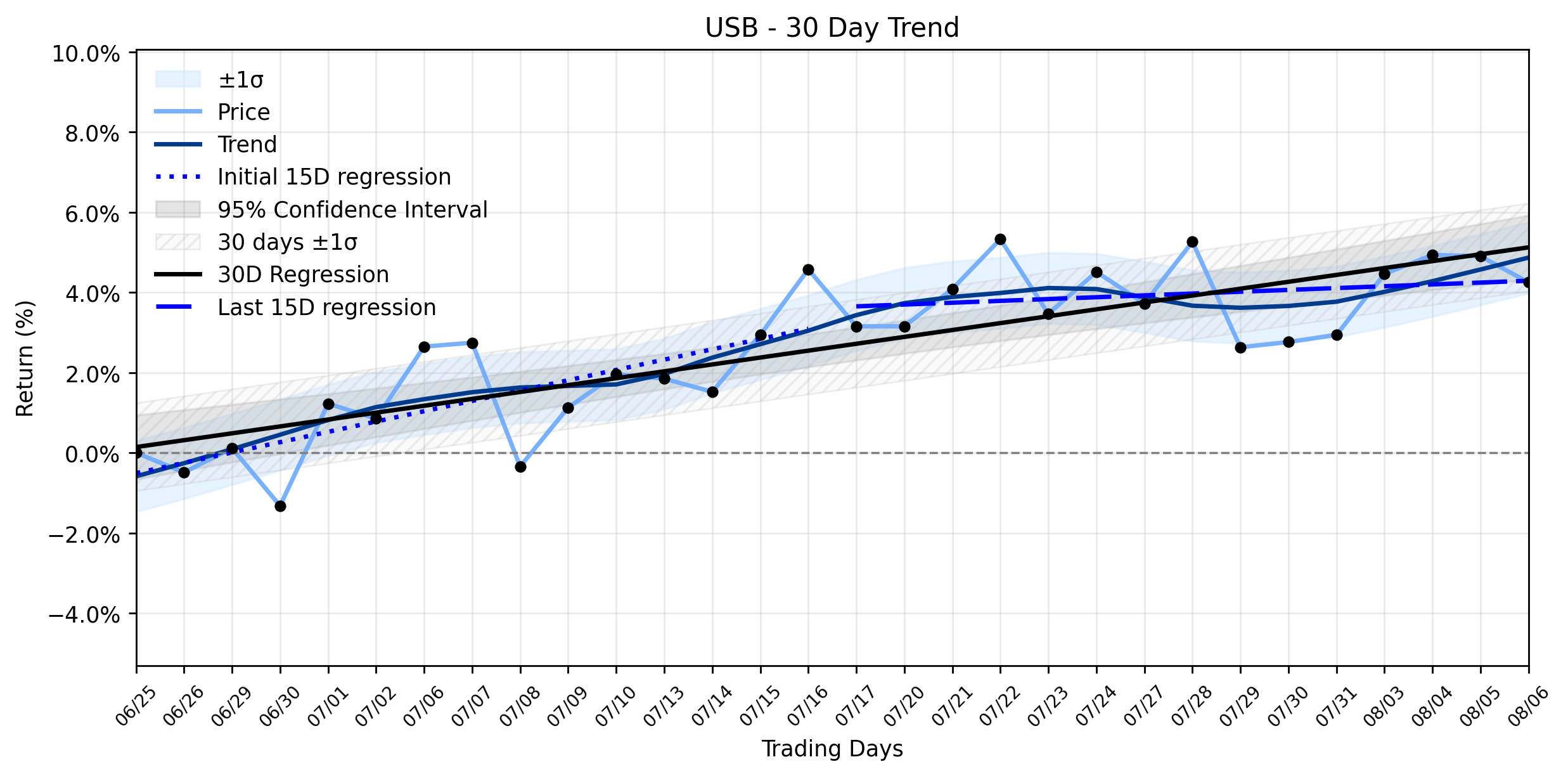

U.S. Bancorp (USB) Hits All-Time High, Then Dips: Is This a Limited Window Before a Valuation Reckoning?

Pct Price Change: -0.62%

- https://finance.yahoo.com/quote/USB/

- www.perplexity.ai/finance/USB

- www.investing.com/news/company-news/us-bancorp-stock-hits-alltime-high-of-6486-usd-93CH-4842633

- simplywall.st/stocks/us/banks/nyse-usb/us-bancorp/news/us-bancorp-usb-faces-a-10-fair-value-gap-after-record-q2-res

- www.stocktitan.net/news/USB/

- seekingalpha.com/news/4614652-u-s-bancorp-projects-2026-net-revenue-growth-of-7-percentminus-9-percent-with-btig-adding

- stockinvest.us/stock/USB

Expedia Group (EXPE) Hits Turbulence: Why Record Earnings Triggered a Major Selloff

Pct Price Change: -4.09%

- https://finance.yahoo.com/quote/EXPE/

- www.marketbeat.com/instant-alerts/wedbush-reiterates-outperform-rating-for-expedia-group-nasdaqexpe-2026-08-06/

- www.marketbeat.com/instant-alerts/expedia-group-nasdaqexpe-given-new-31000-price-target-at-cantor-fitzgerald-2026-08-06/

- www.marketbeat.com/instant-alerts/expedia-group-nasdaqexpe-price-target-raised-to-33000-2026-08-06/

- www.pymnts.com/earnings/2026/expedia-leans-on-ai-and-b2b-growth-to-lift-outlook-after-strong-q2/

- kalkinemedia.com/us/stocks/consumer/can-expedia-group-nasdaqexpe-build-on-its-strong-quarter

- seekingalpha.com/article/4931489-expedia-group-inc-2026-q2-results-earnings-call-presentation

- www.paxnews.com/news/agency/expedia-group-beats-q2-guidance-revenue-climbs-14-b2b-segment-grows

- openjaw.com/newsroom/retail/2026/08/06/expedia-sees-b2b-revenue-jump-23-as-b2c-lags/

- www.fullyinformed.com/expedia-stock-expe-trade-alert-and-idea-for-thu-aug-6-2026/

- www.gurufocus.com/news/9012763/expe-maintained-by-rbc-capital-price-target-raised-to-330?utm_source=marketwatch&utm_medium=syndication&utm_campaign=headlines&r=4bf001661e6fdd88d0cd7a5659ff9748&mod=mw_quote_news

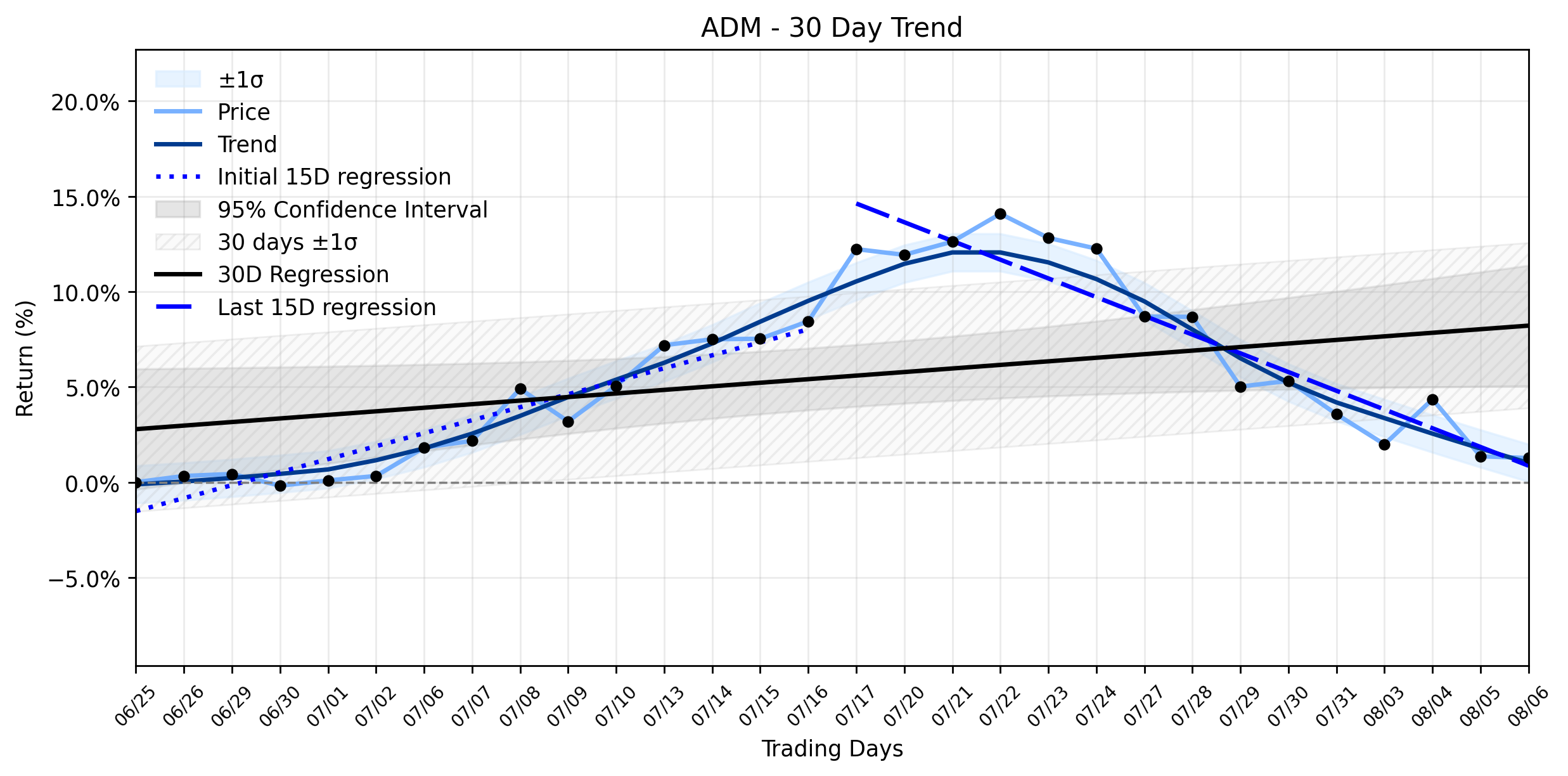

Archer-Daniels-Midland (ADM) Sees Quiet Pullback Amidst Stellar Earnings and Dividend Hike: Is the Market Missing Something Now?

Pct Price Change: -0.09%

- https://finance.yahoo.com/quote/ADM/

- millingmea.com/adm-reports-surge-in-q2-2026-earnings-raises-full-year-guidance/

- simplywall.st/stocks/us/food-beverage-tobacco/nyse-adm/archer-daniels-midland/news/is-adms-stronger-outlook-dividend-hike-and-new-debt-altering

- www.marketbeat.com/instant-alerts/archer-daniels-midland-company-nyseadm-plans-quarterly-dividend-of-052-2026-08-06/

Wells Fargo (WFC) Takes a Notable Retreat: Is the Blockchain Bet Enough to Stabilize a Shifting Uptrend?

Pct Price Change: -1.77%

- https://finance.yahoo.com/quote/WFC/

- news.bitcoin.com/crypto-news/wells-fargo-brings-24-7-tokenized-payments-to-corporate-clients/

- ffnews.com/news/wells-fargo-unveils-tokenized-deposits-for-corporate-and-commercial-clients

- www.fintechfutures.com/tokenisation/wells-fargo-outlines-tokenised-deposits-launch-for-corporate-payments

- www.advisorhub.com/wells-loses-470m-team-to-rayjay-adds-400m-private-wealth-broker-from-merrill/

- dallasinnovates.com/dallas-based-corgan-wins-sustainability-award-for-wells-fargos-net-positive-irving-campus/

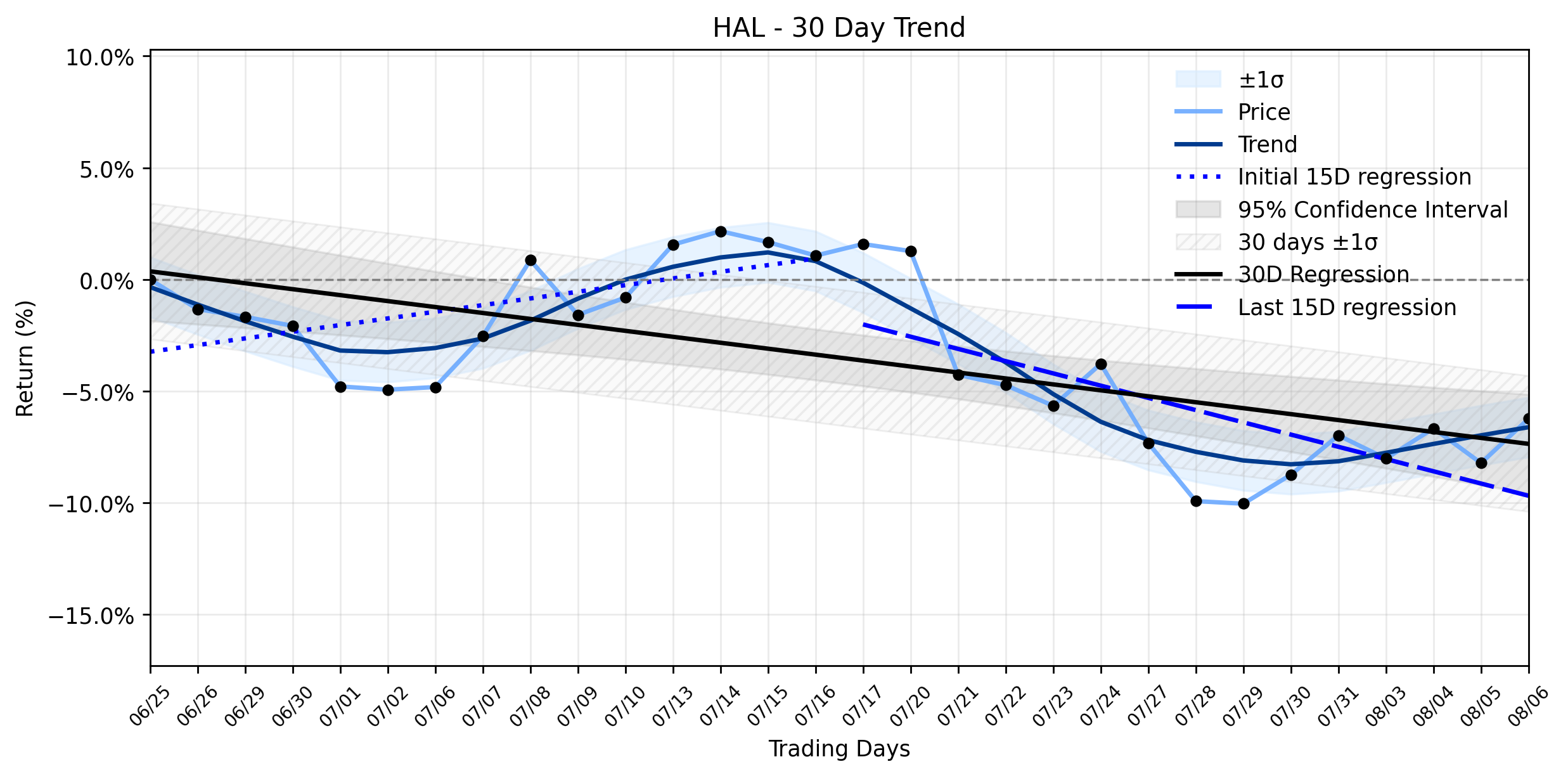

Halliburton (HAL) Stages a Healthy Climb: Is the Downtrend Finally Stabilizing After Its Global Contract Blitz?

Pct Price Change: 2.17%

- https://finance.yahoo.com/quote/HAL/

- www.marketbeat.com/stocks/NYSE/HAL/earnings/

- www.halliburton.com/en/about-us/press-release/halliburton-announces-second-quarter-2026-results

- www.stocktitan.net/sec-filings/HAL/8-k-halliburton-co-reports-material-event-0ed20193ba2f.html

- www.investing.com/news/transcripts/earnings-call-transcript-halliburton-tops-q2-2026-estimates-shares-fall-93CH-4803695

- ir.halliburton.com/news-and-events/press-releases

- www.stocktitan.net/news/HAL/

- www.tradingview.com/news/zacks:7e48350f9094b:0-halliburton-s-outlook-improves-as-contract-wins-fuel-global-growth-ahead/

- ca.investing.com/news/stock-market-news/form-8k-halliburton-for-6-august-93CH-4781665

- www.marketbeat.com/stocks/NYSE/HAL/

- www.argusmedia.com/en/news-and-insights/latest-market-news/2860242-oil-services-see-growing-overseas-momentum-despite-war

Trip.com Group (TCOM) Stages Sharp Climb: Is the Travel Giant's Ascent Fueled by Paternity Leave or Market Expectations?

Pct Price Change: 0.61%

- https://finance.yahoo.com/quote/TCOM/

- www.prnewswire.com/news-releases/tripcom-group-releases-2025-sustainability-report-announces-new-global-paid-paternity-leave-policy-302845675.html

- www.marketbeat.com/articles/why-analysts-are-bullish-on-a-stock-thats-down-20/

- www.zacks.com/stock/news/2970382/airbnb-inc-abnb-beats-q2-earnings-and-revenue-estimates?cid=CS-ZC-FT-fundamental_analysis%7Cyseop_template_4-2970382

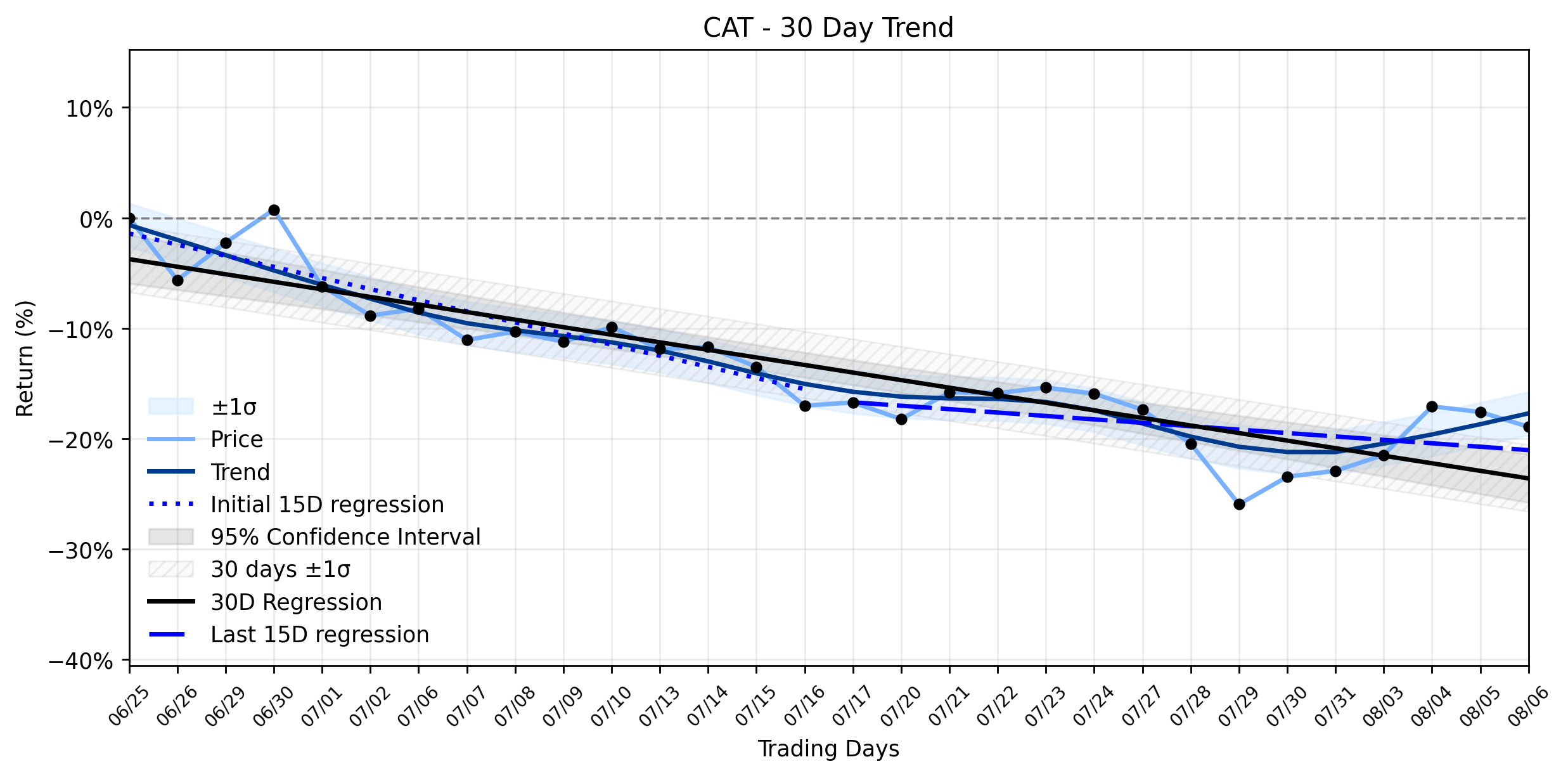

Caterpillar (CAT) Faces a Significant Retreat: Is the AI Boom's Momentum Fading, or Just a Market Head-Fake?

Pct Price Change: -1.62%

- https://finance.yahoo.com/quote/CAT/

- www.benzinga.com/markets/earnings/26/08/60906229/caterpillar-cashes-in-on-ai-buildout-raises-2026-sales-outlook

- www.marketbeat.com/instant-alerts/caterpillar-nysecat-stock-price-down-14-whats-next-2026-08-06/

- seekingalpha.com/news/4625443-caterpillar-projects-mid-to-high-teens-2026-sales-growth-as-backlog-reaches-72b

- www.barchart.com/story/news/3695280/cat-stock-alert-caterpillar-s-ai-infrastructure-boom-is-just-getting-started

- www.bnnbloomberg.ca/business/company-news/2026/08/04/caterpillar-raises-2026-revenue-growth-target-after-quarterly-profit-beat/

- 247wallst.com/investing/2026/08/06/prediction-cat-stock-will-hit-1000-on-this-date/

Coinbase (COIN) Faces Sharp Decline as Crypto Market Navigates Exploit Fears and Regulatory Fog, Signaling an Emerging Downtrend []

![LOESS trend regression chart or WordCloud graph for Coinbase (COIN) Faces Sharp Decline as Crypto Market Navigates Exploit Fears and Regulatory Fog, Signaling an Emerging Downtrend [] (COIN)](/static/graphs/cod579keyCoinbaseGlobal3DTAugust%2006%2C%2020262110.png)

Pct Price Change: -2.99%

- https://finance.yahoo.com/quote/COIN/

- coinstats.app/ai/a/crypto-news-update-05-August-2026

- bitcoinmagazine.com/news/white-house-reviewing-crypto-clarity-act

- 247wallst.com/investing/cryptocurrency/2026/08/05/will-xrp-ripple-recover-in-2026-the-3-things-that-have-to-happen-first/

- coingape.com/coinbase-to-suspend-trading-for-six-crypto-pairs-on-august-6/

- www.coinbase.com/blog/coinbase-australia-launches-perpetual-contracts

- crypto.news/circle-renews-coinbase-usdc-deal-rules-out-dividends/

- en.bloomingbit.io/feed/news/117757

- www.coinbase.com/blog/q2-2026-solana-validator-performance-report

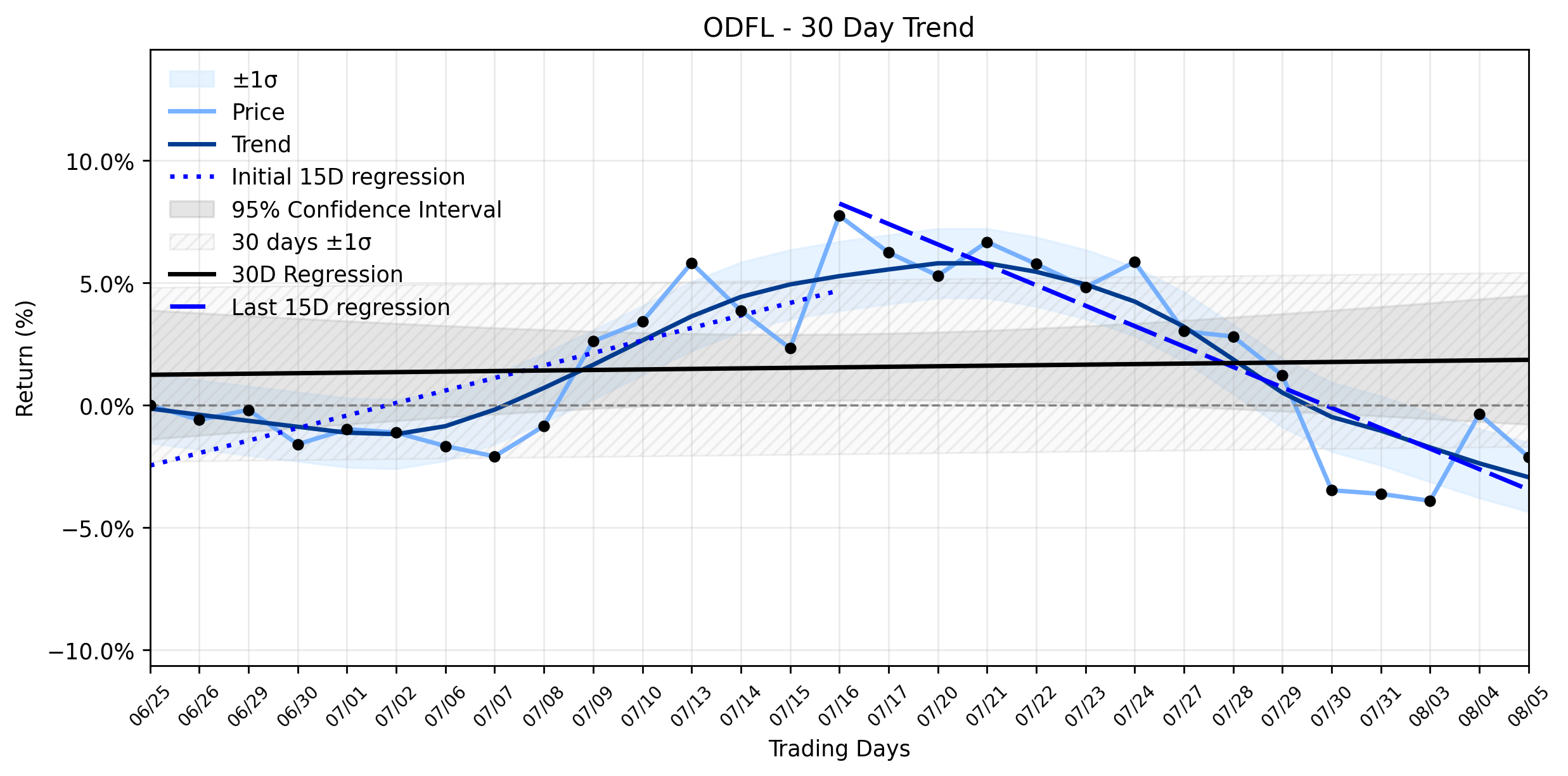

Old Dominion Freight Line (ODFL) Faces a Meaningful Loss: Is the Emerging Downtrend Catching Up Before It's Too Late?

Pct Price Change: -1.76%

- https://finance.yahoo.com/quote/ODFL/

- www.zacks.com/stock/news/2967887/can-odfls-q2-earnings-beat-and-higher-spending-drive-more-growth

- www.marketbeat.com/instant-alerts/old-dominion-freight-line-inc-nasdaqodfl-given-consensus-recommendation-of-hold-by-brokerages-2026-08-03/

- freightflowadvisor.substack.com/p/q2-earnings-what-ch-robinson-and

- markets.chroniclejournal.com/chroniclejournal/article/stockstory-2026-8-5-the-5-most-interesting-analyst-questions-from-old-dominion-freight-lines-q2-earnings-call

- www.stocktitan.net/sec-filings/ODFL/8-k-old-dominion-freight-line-inc-reports-material-event-b2c44407c2ee.html

- www.investing.com/news/transcripts/earnings-call-transcript-old-dominion-freight-line-beats-q2-2026-estimates-93CH-4821050

- www.thestreet.com/investing/stocks/old-dominion-yellow-bankruptcy-strategy

- ir.odfl.com/news-events/press-releases/detail/347/old-dominion-freight-line-reports-second-quarter-2026

- www.gurufocus.com/news/9003745/old-dominion-freight-line-inc-odfl-shares-surge-37-what-gf-score-of-94-tells-investors

Automated Insights Question Microsoft's (MSFT) Slide: Is the AI Juggernaut Taking a Tactical Retreat Despite Accelerating Momentum?

Pct Price Change: -1.09%

- https://finance.yahoo.com/quote/MSFT/

- www.marketbeat.com/stocks/NASDAQ/MSFT/earnings/

- www.zacks.com/stock/news/2968238/zacks-investment-ideas-feature-highlights-microsoft-bloom-and-emcor?cid=CS-ZC-FT-press_releases-2968238

- www.marketbeat.com/instant-alerts/filing-microsoft-corporation-msft-stock-position-cut-by-boston-common-asset-management-llc-2026-08-05/

- www.microsoft.com/en-us/investor/earnings/fy-2026-q4/press-release-webcast

- www.briefs.co/news/openai-payments-made-up-most-of-microsoft-s-ai-revenue/

- www.techpowerup.com/351384/microsoft-is-quietly-deleting-32-gb-ram-recommendation-for-windows-11

- www.windowslatest.com/2026/08/05/microsoft-says-it-leverages-windows-11-to-push-edge-bing-and-copilot-browser-choice-alliance-group-calls-it-out/

- www.windowslatest.com/2026/08/04/microsoft-teams-is-fighting-ai-deepfake-meetings-with-a-new-report-button-rolling-out-august-2026/

- www.microsoft.com/en-us/security/blog/2026/08/04/advance-zero-trust-for-ai-new-tools-and-guidance-to-secure-ai-agents-and-devsecops/

- www.infosecurity-magazine.com/news/microsoft-ai-security-initiatives/

- finbold.com/monster-insider-trading-alert-for-microsoft-msft-stock/

- www.globenewswire.com/news-release/2026/08/05/3339592/34548/en/deadline-alert-microsoft-corporation-msft-shareholders-who-lost-money-urged-to-contact-glancy-prongay-wolke-rotter-llp-about-securities-fraud-lawsuit.html

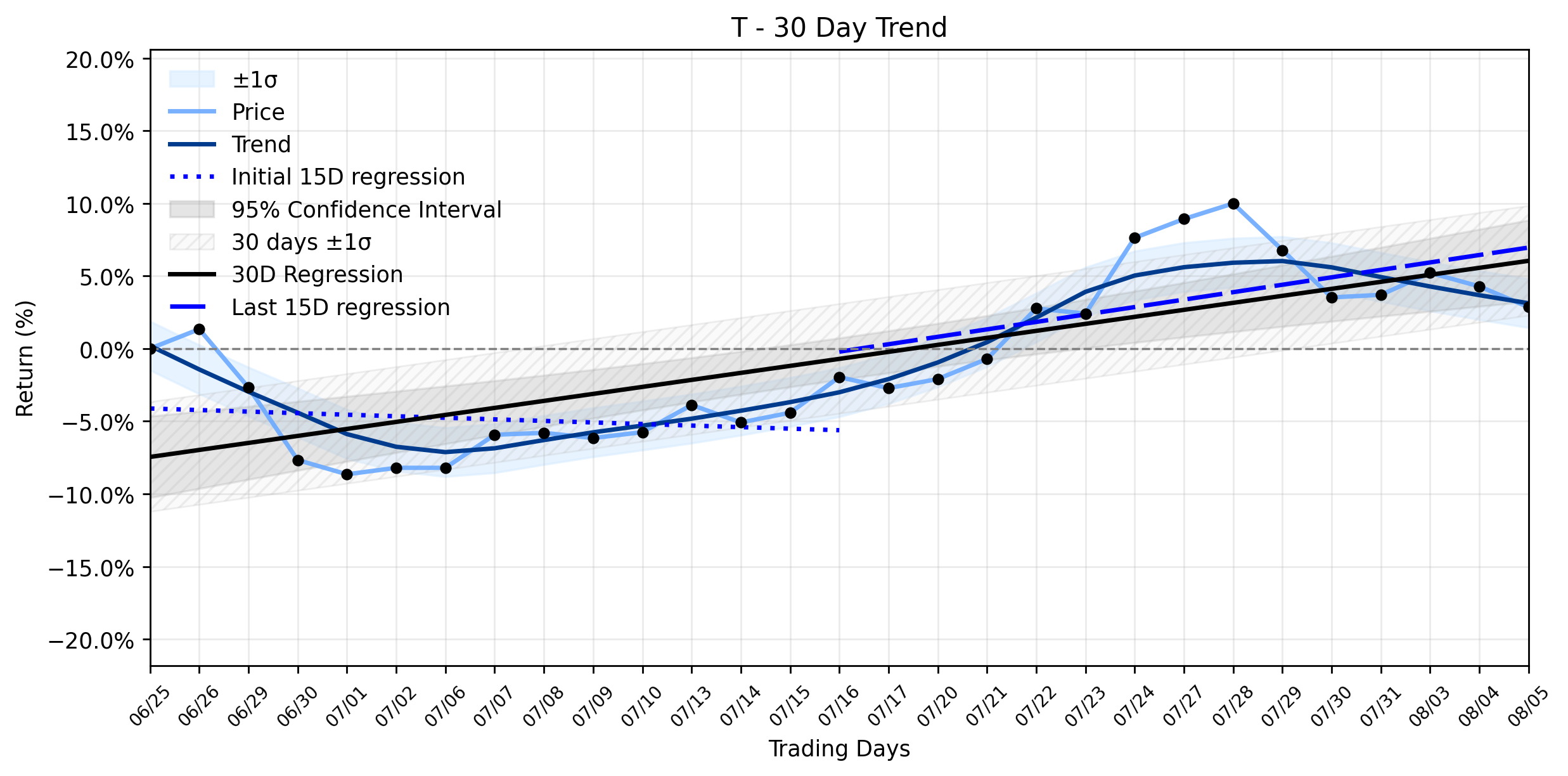

Smart Money's Dilemma: Is AT&T's (T) Recent Pullback a Test for its Recovering Uptrend Amidst New Galactic Competition?

Pct Price Change: -1.37%

- https://finance.yahoo.com/quote/T/

- simplywall.st/stocks/us/telecom/nyse-t/att/news/att-t-is-down-52-after-spacex-mobile-push-and-new-eurobonds

- www.marketbeat.com/instant-alerts/att-nyset-stock-price-down-13-heres-what-happened-2026-08-05/

- www.tipranks.com/news/why-telecom-stocks-att-verizon-and-t-mobile-are-falling-after-spacexs-new-plans-8-5-26

- community.designtaxi.com/topic/34765-is-att-down-august-5-2026/

- www.trefis.com/stock/t/articles/610172/58-billion-in-payouts-a-lagging-stock-the-t-trade-off/2026-08-05

LPL Financial (LPLA) Sees Solid Advance as $400M Wealth Firm Jumps Ship: What's Driving the Uptrend Now?

Pct Price Change: 1.60%

- https://finance.yahoo.com/quote/LPLA/

- www.stocktitan.net/news/LPLA/west-kai-private-wealth-joins-lpl-strategic-u96f8rqiv55r.html

- investor.lpl.com/

- www.stocktitan.net/sec-filings/LPLA/8-k-lpl-financial-holdings-inc-reports-material-event-37ff839d36bf.html

- www.marketbeat.com/instant-alerts/filing-bank-of-america-corp-de-raises-stake-in-lpl-financial-holdings-inc-lpla-2026-08-04/

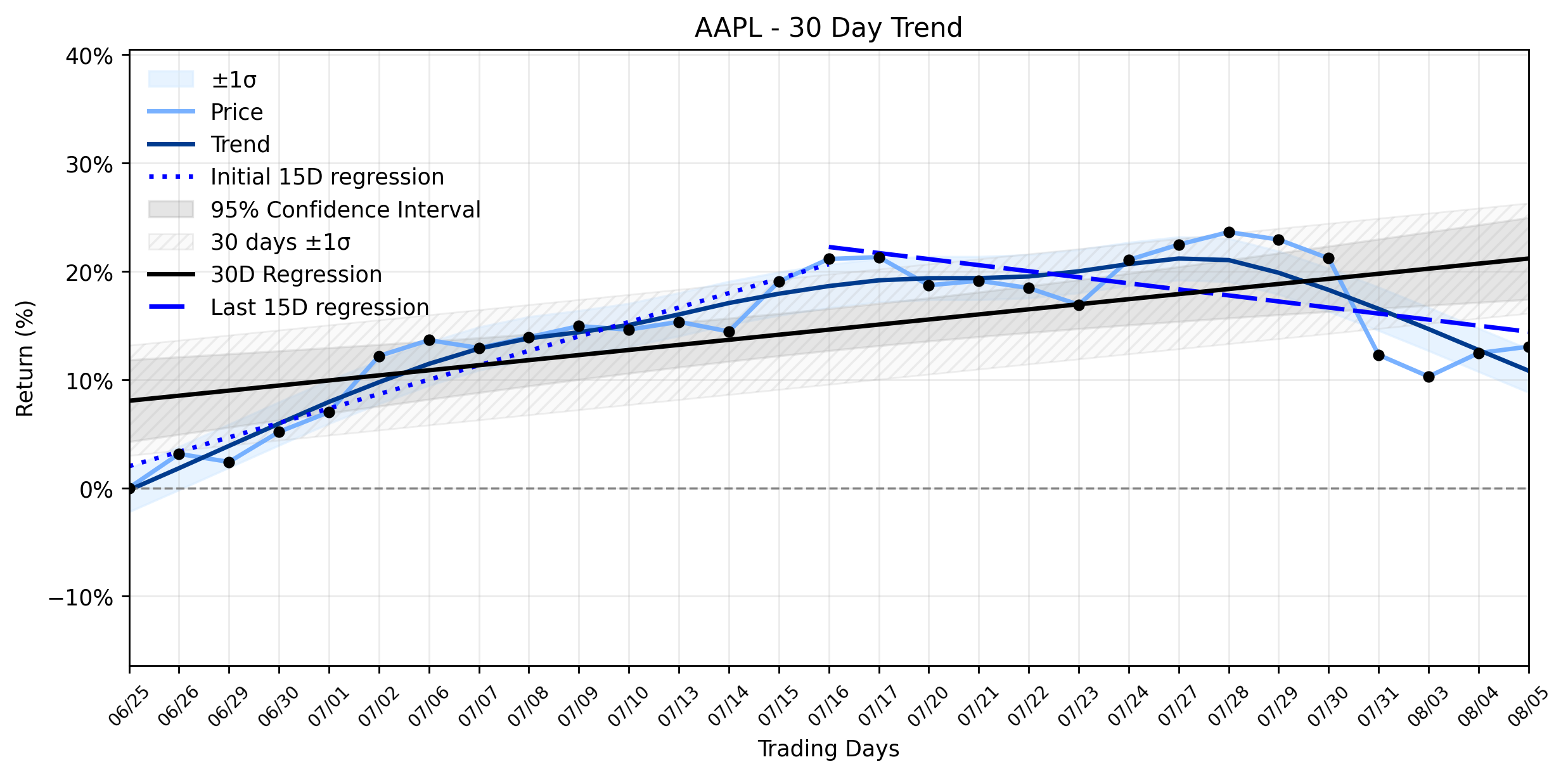

Apple (AAPL) Posts a Modest Rise, But a Deeper Trend Reversal Looms – What Are Investors Overlooking Right Now?

Pct Price Change: 0.52%

- https://finance.yahoo.com/quote/AAPL/

- www.fool.com/investing/2026/08/05/apple-quarterly-iphone-sales-better-than-seem/

- www.interactivecrypto.com/apple-navigates-margin-pressures-and-analyst-downgrades-amid-sector-rotation-aug-2026

- www.fool.com/investing/2026/08/05/departing-apple-ceo-tim-cook-gave-memory-stocks/

- www.facebook.com/BloombergTelevision/videos/apple-tumbled-in-late-trading-after-component-shortages-weighed-on-the-companys-/1214548597482715/

- www.techpowerup.com/351391/apple-scrambles-for-dram-cxmt-reportedly-rejects-negotiations

- www.computerworld.com/article/4205686/apples-memory-crisis-is-a-big-red-flag-for-tech.html

- www.thestreet.com/investing/stocks/bank-of-america-doubles-down-on-apple-stock-for-rest-of-2026

Icahn Enterprises (IEP) Takes a Sharp Plunge After Q2 Shocker: Is the Stable Uptrend Now on Thin Ice?

Pct Price Change: -3.49%

- https://finance.yahoo.com/quote/IEP/

- www.ielp.com/

- www.marketbeat.com/instant-alerts/icahn-enterprises-q2-earnings-call-highlights-2026-08-05/

- www.investing.com/news/company-news/icahn-enterprises-q2-2026-slides-loss-widens-despite-energy-gains-93CH-4838568

- www.ielp.com/news-releases/news-release-details/icahn-enterprises-lp-nasdaq-iep-today-announced-its-second-2

- ng.investing.com/news/company-news/icahn-enterprises-q2-2026-slides-loss-widens-despite-revenue-beat-93CH-2640337

- www.marketbeat.com/earnings/reports/2026-8-5-icahn-enterprises-lp-stock/

- seekingalpha.com/article/4930844-icahn-enterprises-l-p-iep-q2-2026-earnings-call-prepared-remarks-transcript

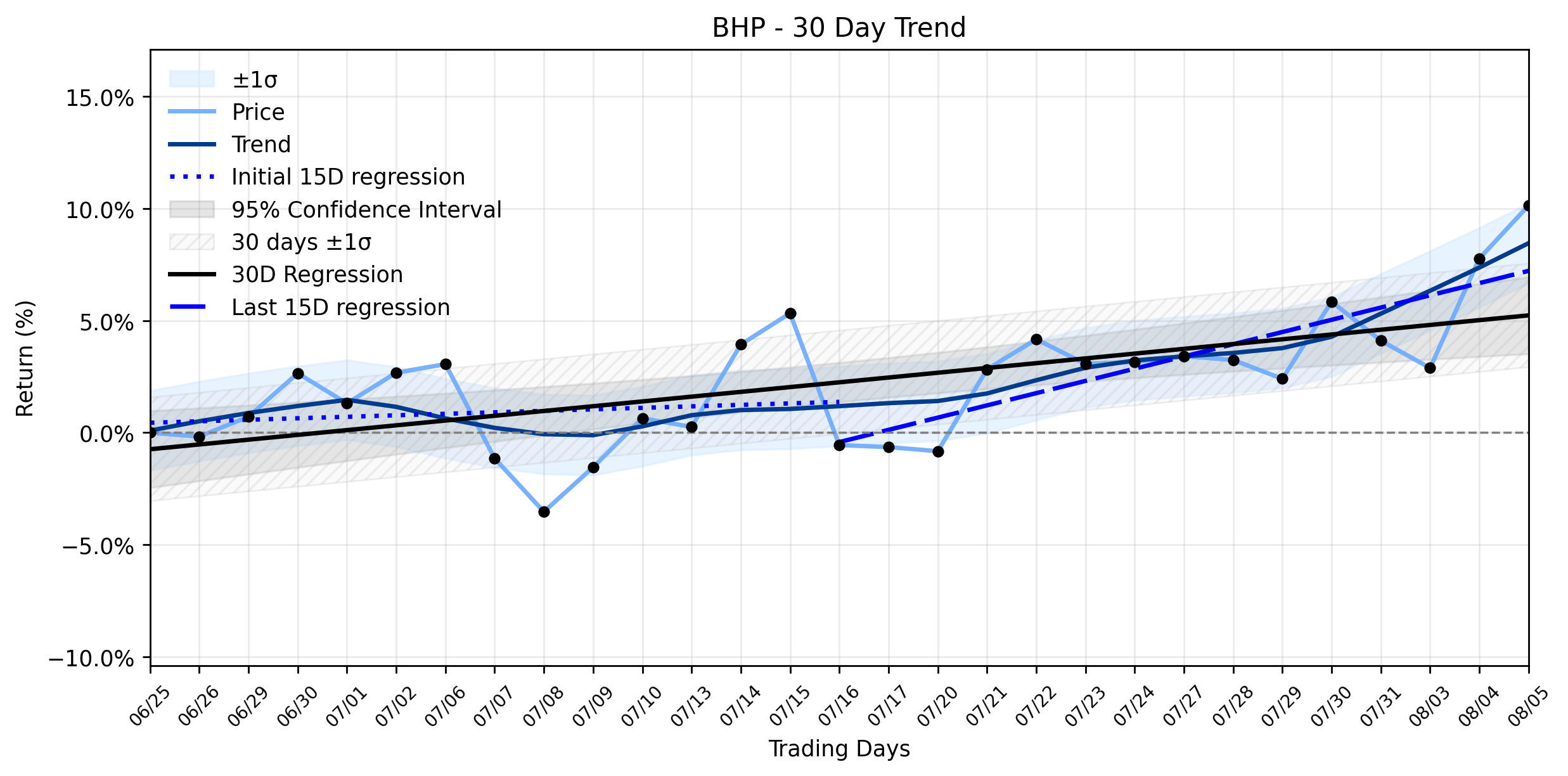

Something Strange is Fueling BHP's Solid Advance Despite Looming Industrial Action

Pct Price Change: 2.20%

- https://finance.yahoo.com/quote/BHP/

- www.canadianminingjournal.com/news/bhp-tops-global-mining-brand%E2%80%91strength-ranking-new-report/

- www.juniorminingnetwork.com/junior-miner-news/press-releases/3312-cse/kbx/208523-kobrea-announces-exploration-alliance-with-bhp-metals-exploration-western-malarguee-mining-district-mendoza-province-argentina.html

- www.argusmedia.com/en/news-and-insights/latest-market-news/2861181-australia-s-bhp-faces-iron-ore-port-strike-in-august

- discoveryalert.com.au/bhp-port-hedland-iron-ore-strike-supply-risk-2026/

- www.fool.com.au/2026/08/06/bhps-copper-guidance-surprise-what-does-this-mean-for-bhp-shares/

- thewest.com.au/business/mining/bhp-strike-unions-falter-as-amwu-halves-involvement-in-action-against-bhp-at-port-hedland-this-weekend-c-22685485

- kalkine.com.au/news/mining/asx-mining-stocks-rise-bhp-rio-tinto-and-fortescue-on-investors-radar

Alibaba (BABA) Navigates a Puzzling Pullback Amidst AI Breakthroughs and Legal Storms

Pct Price Change: -0.36%

- https://finance.yahoo.com/quote/BABA/

- unrot.co/blogs/ai-news-august-5-2026

- www.globenewswire.com/news-release/2026/08/05/3339605/673/en/rosen-recognized-investor-counsel-encourages-alibaba-group-holding-limited-investors-to-secure-counsel-before-important-deadline-in-securities-class-action-baba.html

- www.financialcontent.com/article/bizwire-2026-8-6-baba-investor-alert-securities-class-action-filed-against-alibaba-group-holding-limited-investors-encouraged-to-contact-kirby-mcinerney-llp

- www.gurufocus.com/news/9006506/baba-investor-notice-robbins-geller-rudman-dowd-llp-announces-that-alibaba-group-holding-limited-investors-with-substantial-losses-have-opportunity-to-lead-the-alibaba-class-action-lawsuit

- www.prnewswire.com/news-releases/baba-investor-alert-alibaba-group-holding-limited-investors-with-substantial-losses-have-opportunity-to-lead-the-alibaba-class-action-lawsuit-302843053.html

- ca.investing.com/analysis/alibaba-rally-faces-its-first-real-test-at-august-earnings-200626751

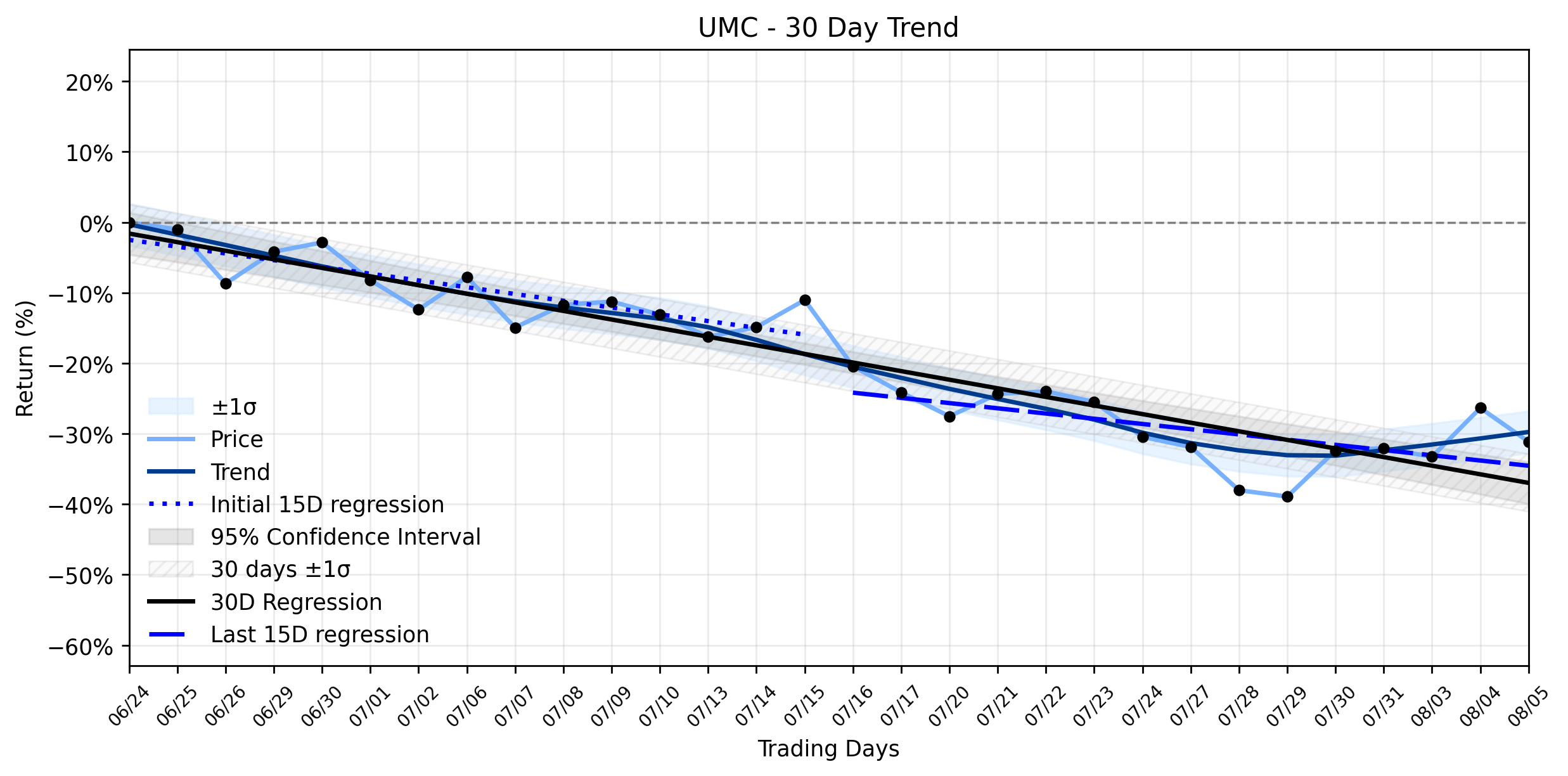

United Microelectronics (UMC) Faces Sharp Plunge: AI Reveals a Deeper Valuation Divide Amidst Positive Sales

Pct Price Change: -6.50%

- https://finance.yahoo.com/quote/UMC/

- www.gurufocus.com/news/9005855/umc-dcf-analysis-intrinsic-value-29-vs-price-21

- www.gurufocus.com/news/9010960/umc-looks-1254-overvalued-on-gf-value-as-dividend-sustainability-faces-headwinds

- www.marketscreener.com/news/united-microelectronics-corporation-reports-unaudited-consolidated-revenues-results-for-the-month-an-ce7f50dcd08ef622

- www.streetinsider.com/Corporate+News/UMC+posts+18.98%25+rise+in+July+2026+net+sales+year+over+year/26877291.html

- www.marketbeat.com/instant-alerts/filing-dimensional-fund-advisors-lp-purchases-333011-shares-of-united-microelectronics-corporation-umc-2026-08-06/

- www.marketbeat.com/instant-alerts/united-microelectronics-nyseumc-shares-gap-down-whats-next-2026-08-03/

Tyler Technologies (TYL) Sees Notable Drop Amidst Cloud Win: Is the Stable Uptrend a Mirage?

Pct Price Change: -2.15%

- https://finance.yahoo.com/quote/TYL/

- simplywall.st/stocks/us/software/nyse-tyl/tyler-technologies/news/tyler-technologies-tyl-lands-tennessee-statewide-cloud-tax-m

- www.stocktitan.net/sec-filings/TYL/8-k-tyler-technologies-inc-reports-material-event-48f2d02a65d7.html

- www.marketbeat.com/instant-alerts/filing-tyler-technologies-inc-tyl-shares-sold-by-dimensional-fund-advisors-lp-2026-08-02/

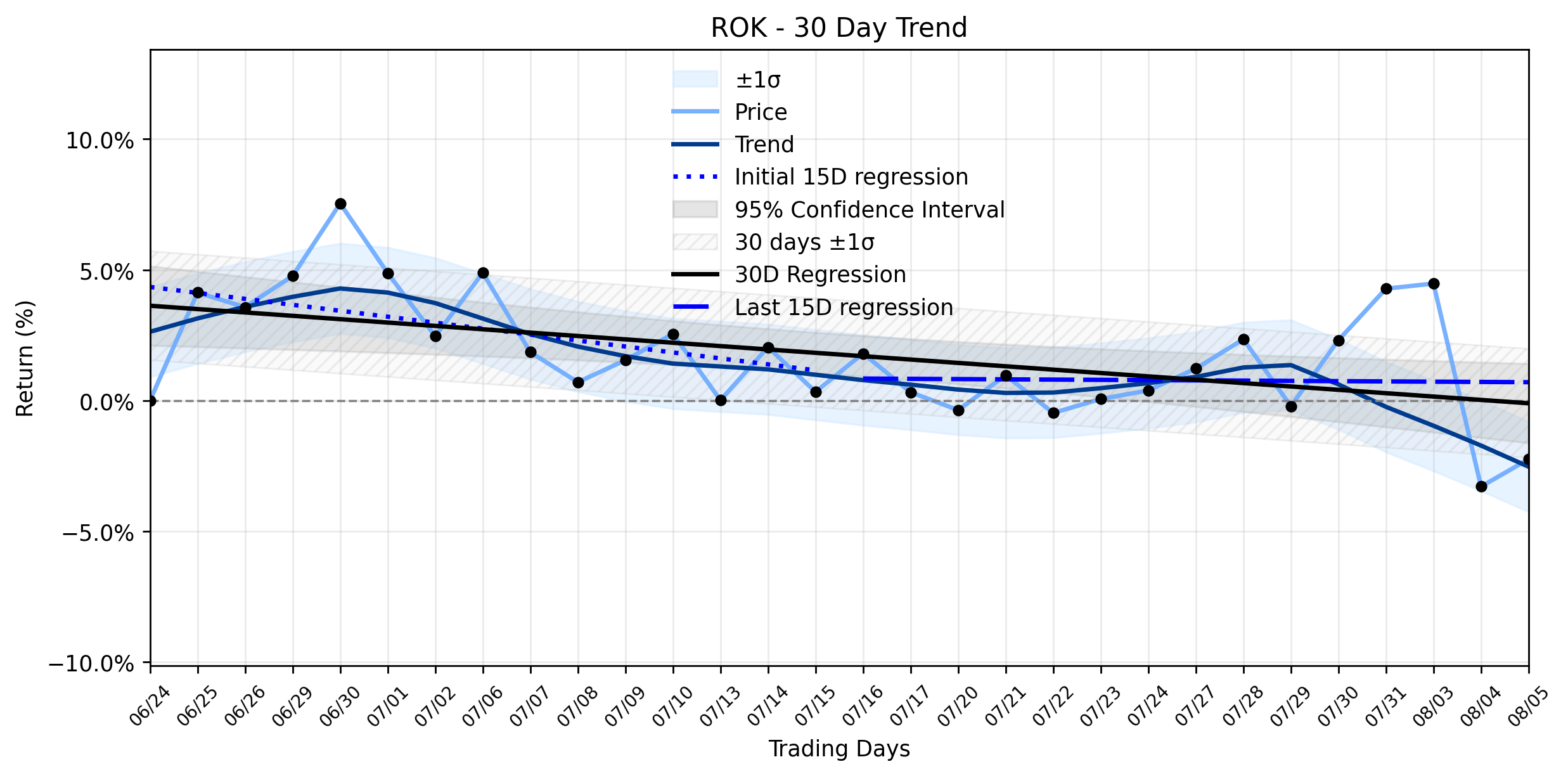

Rockwell Automation (ROK) Sees Fragile Advance: Is This Rise a Downtrend's Last Stand or a Glimmer of Hope?

Pct Price Change: 1.08%

- https://finance.yahoo.com/quote/ROK/

- www.marketbeat.com/instant-alerts/citigroup-issues-pessimistic-forecast-for-rockwell-automation-nyserok-stock-price-2026-08-05/

- ca.investing.com/news/stock-market-news/rockwell-automation-stock-falls-4-on-weak-guidance-despite-q3-beat-93CH-4773687

- www.rockwellautomation.com/en-us/company/news/press-releases/Rockwell-Automation-Reports-Third-Quarter-2026-Results.html

- www.bnnbloomberg.ca/business/2026/08/04/rockwell-automation-raises-2026-profit-forecast-on-strong-industrial-demand/

- www.gurufocus.com/news/9005870/is-rok-overvalued-dcf-says-worth-152

X4 Pharmaceuticals (XFOR) Momentum Under Pressure: Why Yesterday's Dip Could Signal a Crucial Juncture

Pct Price Change: -3.26%

- https://finance.yahoo.com/quote/XFOR/

- www.stocktitan.net/news/XFOR/x4-pharmaceuticals-announces-inducement-grants-under-nasdaq-listing-saqrlzzltp93.html

- www.stockwatch.com/News/Item/U-z9802703-U!XFOR-20260803/U/XFOR

- www.marketbeat.com/stocks/NASDAQ/XFOR/

- www.fullyinformed.com/stock-market-outlook-for-wed-aug-5-2026-confirmed-macd-up-signal-overbought/

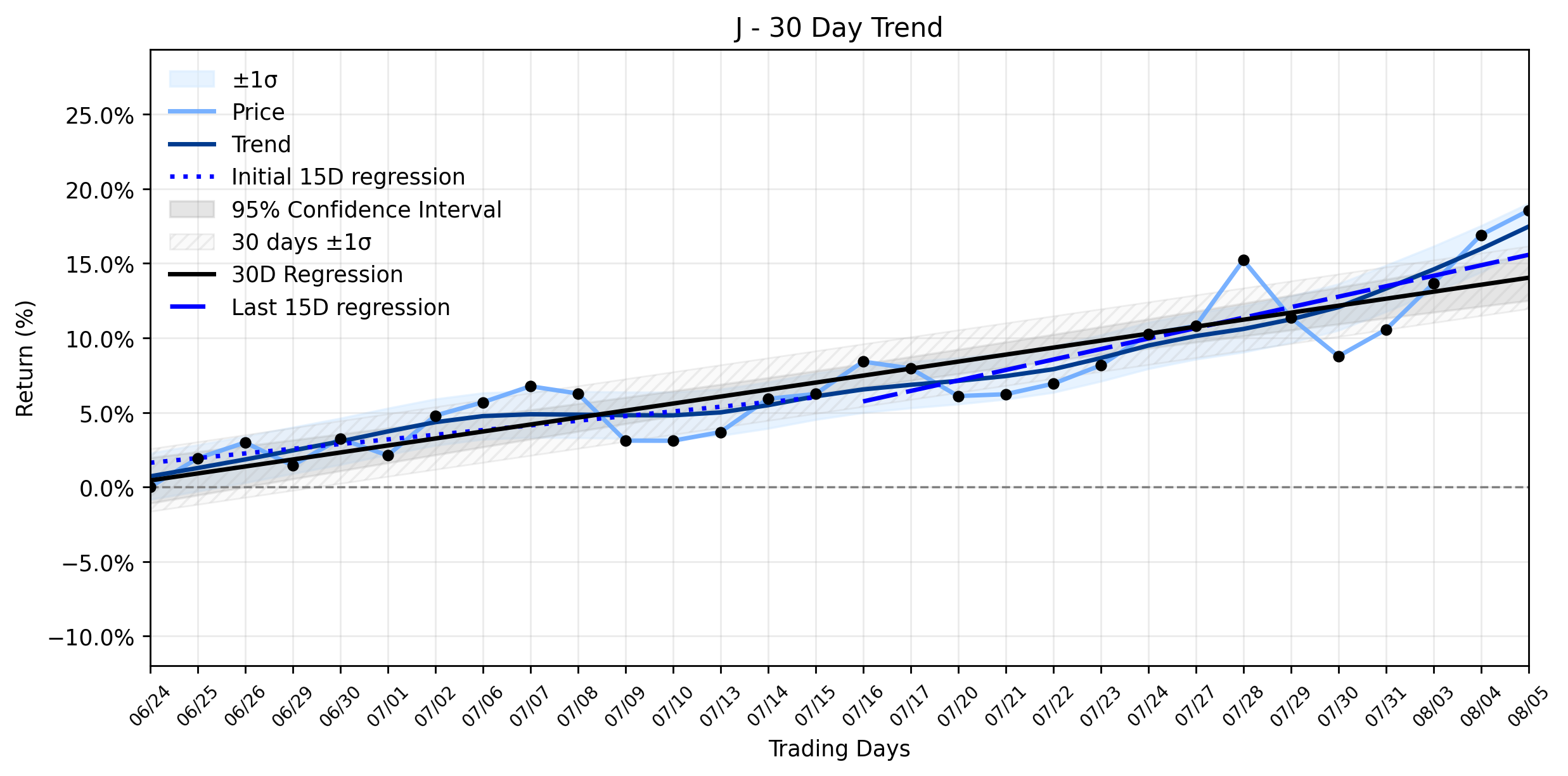

Jacobs Solutions (J) Sets Up for a Crucial Battle: Why a Strong Advance Met After-Hours Resistance Despite Record Wins

Pct Price Change: 1.39%

- https://finance.yahoo.com/quote/J/

- www.gurufocus.com/news/9003039/is-jacobs-solutions-inc-j-overvalued-after-q3-earnings-beat-eps-184-revenue-41-billion-gf-score-73100

- www.marketbeat.com/instant-alerts/jacobs-solutions-q3-earnings-call-highlights-2026-08-05/

- seekingalpha.com/article/4931051-jacobs-solutions-inc-2026-q3-results-earnings-call-presentation?source=feed_all_articles

- www.zacks.com/stock/news/2968830/jacobs-q3-earnings-meet-estimates-revenues-up-yy-stock-down

- deltasheets.substack.com/p/j-fy2026-q3

- www.constructionowners.com/news/jacobs-secures-18-top-rankings-in-enrs-2026-design-firm-market-review

- www.post-gazette.com/business/money/2026/08/05/stock-market-today-august-5-2026/stories/202608050030

A2Z Cust2Mate Solutions (AZ) Stages Solid Advance: Is Smart Money Betting on Buybacks Over Bearish Calls?

Pct Price Change: 2.38%

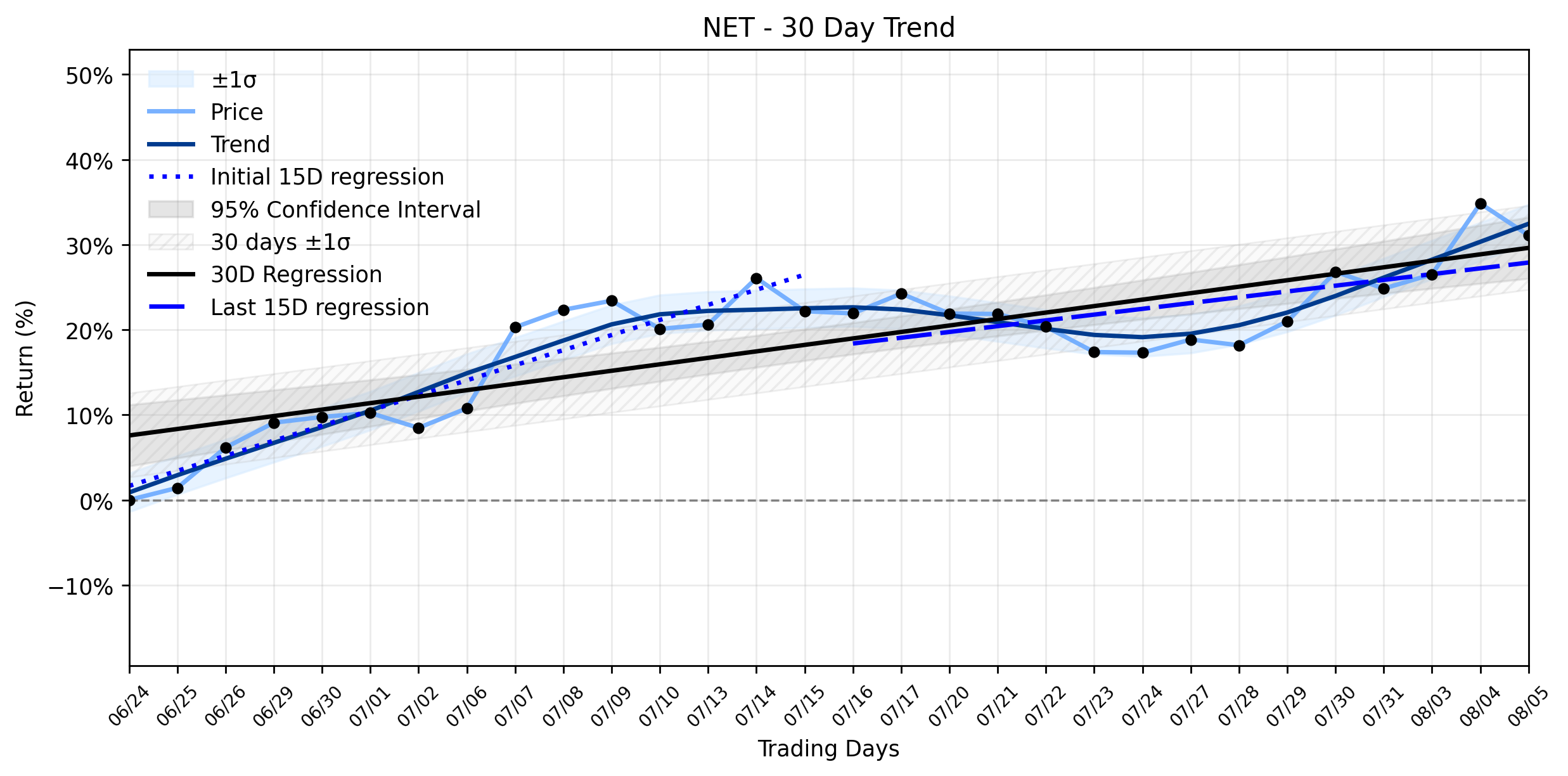

Cloudflare (NET) Takes a Hit: Is Yesterday's Significant Retreat a Textbook Revaluation Before Q2 Earnings, or a Deeper Shift in its Stabilizing Uptrend?

Pct Price Change: -2.78%

- https://finance.yahoo.com/quote/NET/

- seekingalpha.com/news/4626214-cloudflare-q2-2026-earnings-preview-street-sees-yy-growth

- www.financialcontent.com/article/stockstory-2026-8-5-cloudflare-net-to-report-earnings-tomorrow-here-is-what-to-expect

- www.zacks.com/stock/news/2966856/cloudflare-to-post-q2-earnings-whats-in-store-for-the-stock

- simplywall.st/stocks/us/software/nyse-net/cloudflare/news/cloudflare-net-stock-looks-pricey-despite-its-325-three-year/amp

- public.com/stocks/net/forecast-price-target

- www.perplexity.ai/finance/NET?comparing=NET,PLTR,AMZN,ZS,NBIS,NVDA

- stockhouse.com/news/press-releases/2026/08/05/cloudflare-os-is-the-first-ai-workspace-built-around-how-companies-actually-work

- www.gurufocus.com/news/9006507/cloudflare-gives-companies-full-visibility-to-audit-analyze-ai-use

- blog.cloudflare.com/

- blog.cloudflare.com/cloudflare-sase-sse-gartner-magic-quadrants-2026/

T-Mobile (TMUS) Navigates a Sharp Decline: Is the Emerging Downtrend Masking a Strategic Upside?

Pct Price Change: -2.12%

- https://finance.yahoo.com/quote/TMUS/

- www.tipranks.com/news/why-telecom-stocks-att-verizon-and-t-mobile-are-falling-after-spacexs-new-plans-8-5-26

- www.morningstar.com/news/marketwatch/20260805394/why-att-verizon-and-t-mobile-shares-are-down-after-spacexs-earnings

- www.pcmag.com/news/tmobile-offers-limited-credits-for-sos-mode-outage-how-to-get-one

- www.telecompetitor.com/t-mobile-launches-0-upfront-mobile-plan-with-36-month-financing/

- public.com/stocks/tmus/forecast-price-target

- tickernerd.com/stock/tmus-forecast/

- www.zacks.com/stock/news/2967948/should-investors-buy-tmus-or-wait-for-better-risk-reward-ahead

- www.marketbeat.com/articles/dodging-deutsche-telekom-t-mobiles-strategic-win/

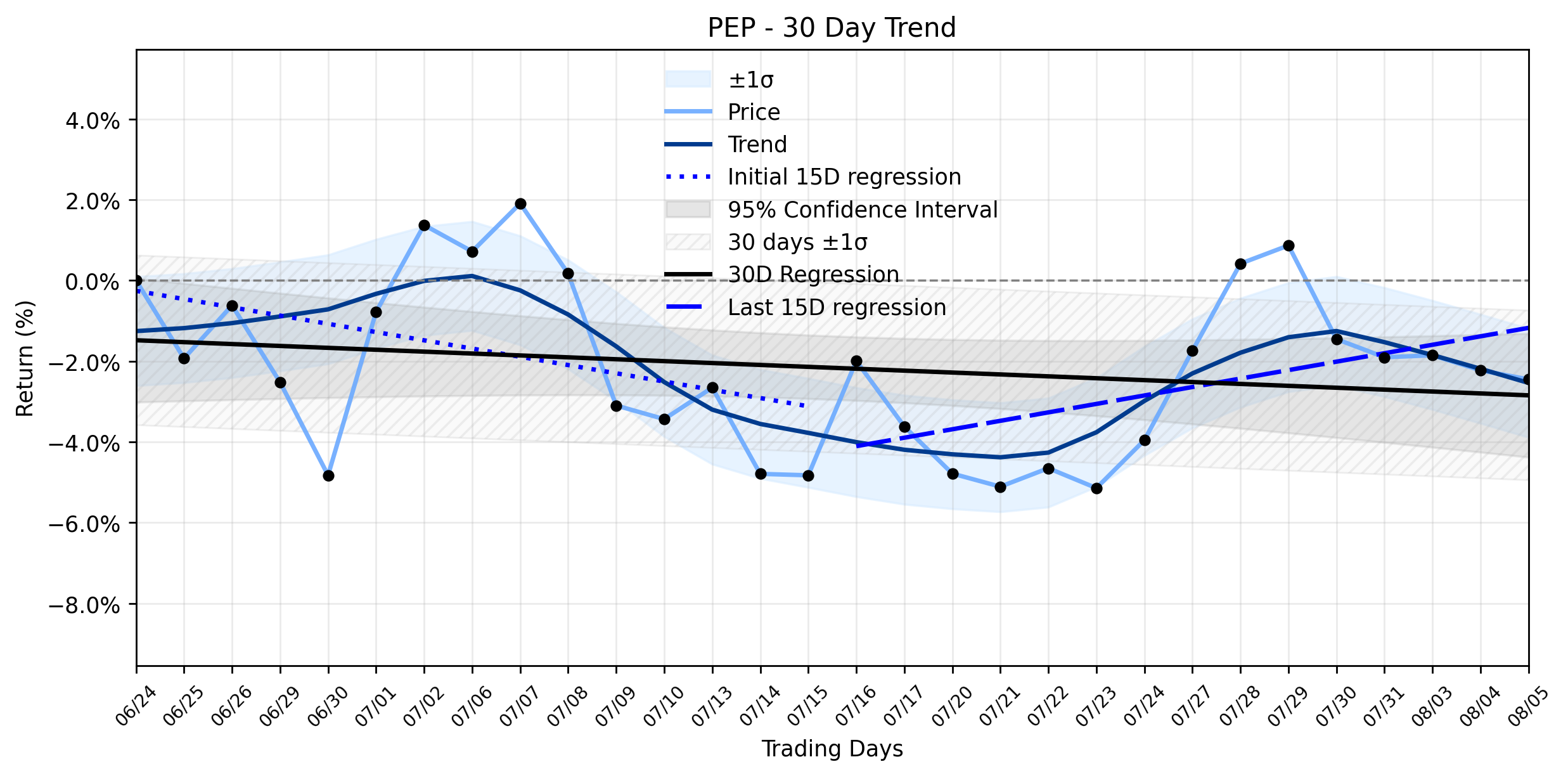

PepsiCo (PEP) Takes a Subtle Retreat: Is the Gazpacho Launch a Distraction from a Stable Downtrend Alert?

Pct Price Change: -0.23%

- https://finance.yahoo.com/quote/PEP/

- www.morningstar.com/news/dow-jones/2026080510170/pepsico-launching-alvalle-gazpacho-in-us

- www.marketscreener.com/news/pepsico-launching-alvalle-gazpacho-in-u-s-ce7f50dcdb8bf125

- www.prnewswire.com/news-releases/pepsico-launches-alvalle-gazpacho-in-the-us-expanding-into-refrigerated-foods-302843909.html

- theshelbyreport.com/2026/08/05/pepsicos-chilled-gazpacho-gets-placement-at-select-whole-foods/

- www.marketbeat.com/instant-alerts/filing-58678-shares-in-pepsico-inc-pep-purchased-by-canandaigua-national-bank-trust-co-2026-08-05/

- kalkinemedia.com/us/stocks/consumer/why-did-pepsico-nasdaqpep-feature-amid-a-firm-earnings-backdrop

Disney (DIS) Soars on Earnings Beat: Is the Sideways Saga Finally Over?

Pct Price Change: 3.65%

- https://finance.yahoo.com/quote/DIS/

- www.tradingkey.com/news/market-movers/262078807-market-movers-dis-20260805

- www.gurufocus.com/news/9007545/the-walt-disney-co-dis-q3-2026-earnings-call-highlights-record-experiences-revenue-and-streaming-margin-surge

- www.wdwinfo.com/news-stories/disney/disney-reports-strong-q3-earnings-fueled-by-parks-streaming-and-toy-story-5/

- thewaltdisneycompany.com/news/disney-q3-earnings-2026/

- public.com/stocks/dis/forecast-price-target

- www.washingtontimes.com/news/2026/aug/5/disney-weighs-free-streaming-product-ceo-josh-damaro-leans-strategy/

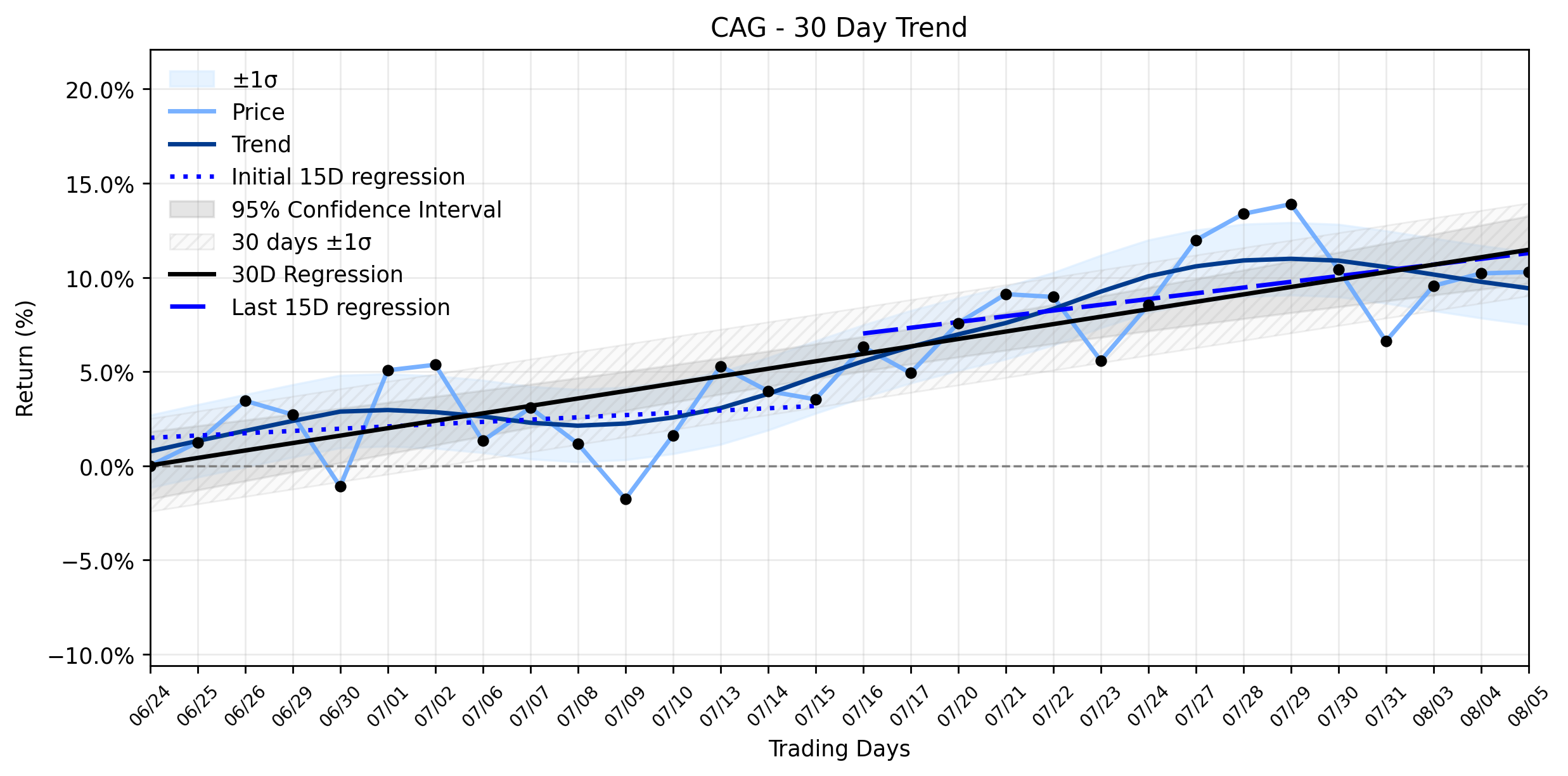

Conagra Brands (CAG) Sees Subtle Uptick: Is This "Realistic Reset" the Catalyst for a Stable Uptrend Now?

Pct Price Change: 0.07%

- https://finance.yahoo.com/quote/CAG/

- www.zacks.com/stock/news/2968919/can-conagras-fiscal-2027-pricing-plan-ease-margin-pressure-ahead

- www.fool.com/investing/2026/08/05/the-surprising-reason-why-conagra-brands-is-up/

- commercialbaking.com/amy-held-named-conagra-evp-chief-administrative-officer/

- www.marketscreener.com/news/conagra-brands-inc-announces-management-changes-ce7f50dedf8dff24

Zscaler (ZS) Sees Developing Decline: Is Its Stable Uptrend Facing an AI-Driven Test of Strength?

Pct Price Change: -0.96%

- https://finance.yahoo.com/quote/ZS/

- www.stocktitan.net/overview/ZS/

- www.globenewswire.com/news-release/2026/08/04/3338601/0/en/zscaler-recognized-as-a-leader-in-both-the-2026-gartner-magic-quadrant-for-sase-platforms-and-2026-magic-quadrant-for-security-service-edge.html

- www.stocktitan.net/news/ZS/zscaler-recognized-as-a-leader-in-both-the-2026-gartner-magic-qrre9rhw6tgg.html

- seekingalpha.com/article/4930659-zscaler-investing-is-worthy-only-beyond-market-hypes-and-worries

- www.marketbeat.com/instant-alerts/filing-zscaler-inc-zs-shares-sold-by-royal-bank-of-canada-2026-08-05/

- public.com/stocks/zs/forecast-price-target

- stockanalysis.com/stocks/zs/forecast/

- seekingalpha.com/article/4929564-zscaler-ai-is-testing-the-companys-moat

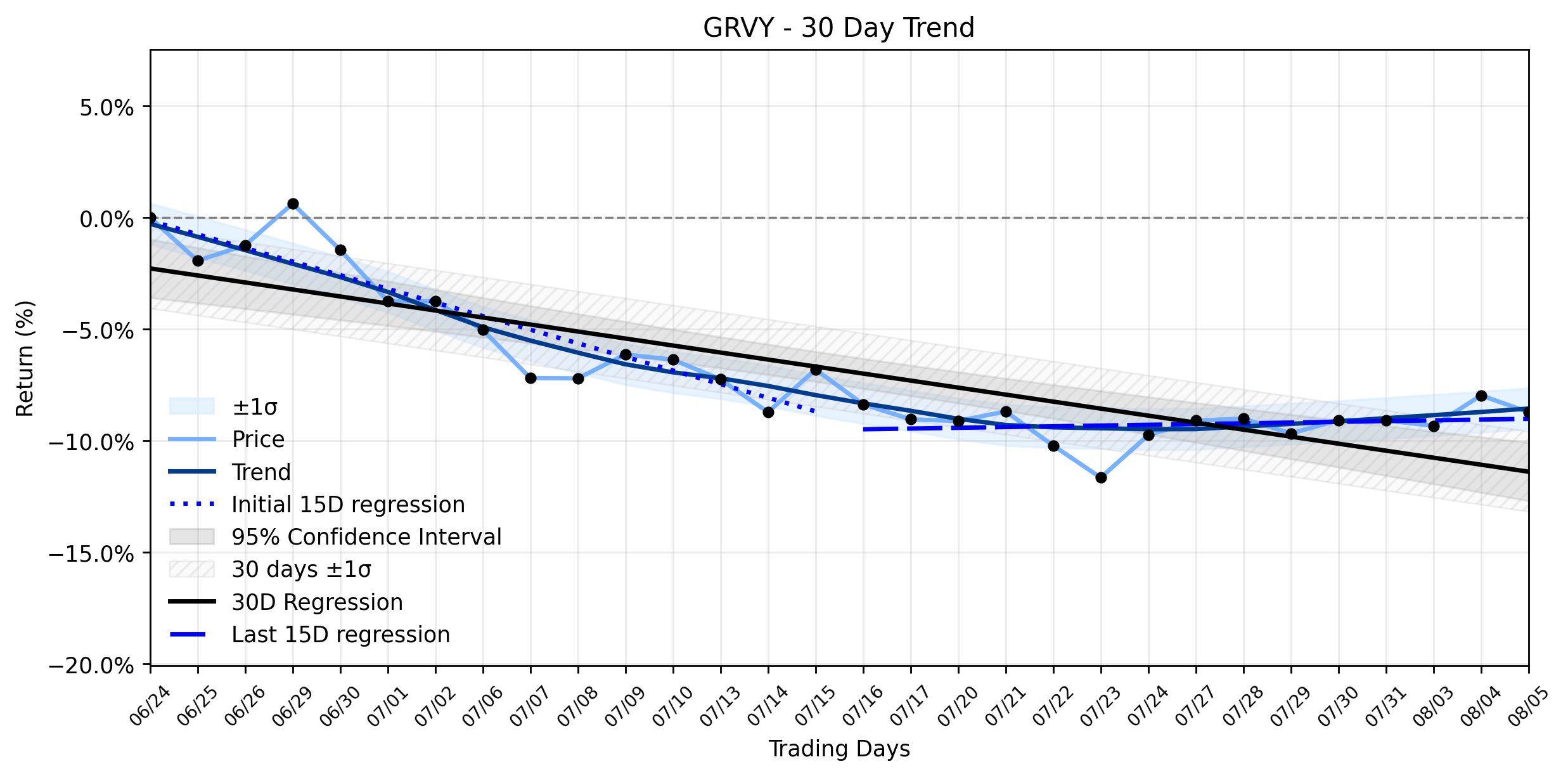

Automated Analysis Reveals Why Gravity Co., Ltd. (GRVY)'s Recent Slide Masks a Resuming Uptrend Ahead of Key Earnings

Pct Price Change: -0.81%

- https://finance.yahoo.com/quote/GRVY/

- www.invenglobal.com/articles/24508/gravity-kicks-off-ragnarok-online-24th-anniversary-festival

- www.gravity.co.kr/

- www.marketbeat.com/stocks/NASDAQ/GRVY/

- www.fool.com/quote/nasdaq/grvy/

- www.marketbeat.com/stocks/NASDAQ/GRVY/earnings/

- www.stocktitan.net/sec-filings/GRVY/6-k-gravity-co-ltd-current-report-foreign-issuer-99d5d715ae00.html

Ryanair (RYAAY) Defies Gravity with a Strange Healthy Climb: What's Fueling the Rebound Amidst Turbulence?

Pct Price Change: 1.66%

- https://finance.yahoo.com/quote/RYAAY/

- www.coventrytelegraph.net/lifestyle/travel/ryanair-passenger-numbers-reach-new-34406924

- www.irishmirror.ie/lifestyle/travel/ryanair-issues-wednesday-august-5-37515399

- shareprices.com/news/in-brief-ryanair-hits-record-222-million-passengers-in-july-syb6awgzym7kkhk/

- www.mylondon.news/lifestyle/travel/ryanair-passenger-numbers-reach-new-34406924

- global.morningstar.com/en-gb/news/alliance-news/1785916754726396000/in-brief-ryanair-hits-record-222-million-passengers-in-july

- www.tradingview.com/news/reuters.com,2026-08-05:newsml_RSE2730Pa:0-reg-ryanair-holdings-plc-ryanair-holdings-rya-ryanair-july-traffic-grows-7-to-record-over-22m/

- www.marketbeat.com/instant-alerts/ryanair-holdings-plc-nasdaqryaay-to-issue-special-dividend-of-044-2026-08-05/

- www.theportugalnews.com/news/2026-08-05/hundreds-of-pilots-file-group-claim-against-ryanair/1065853

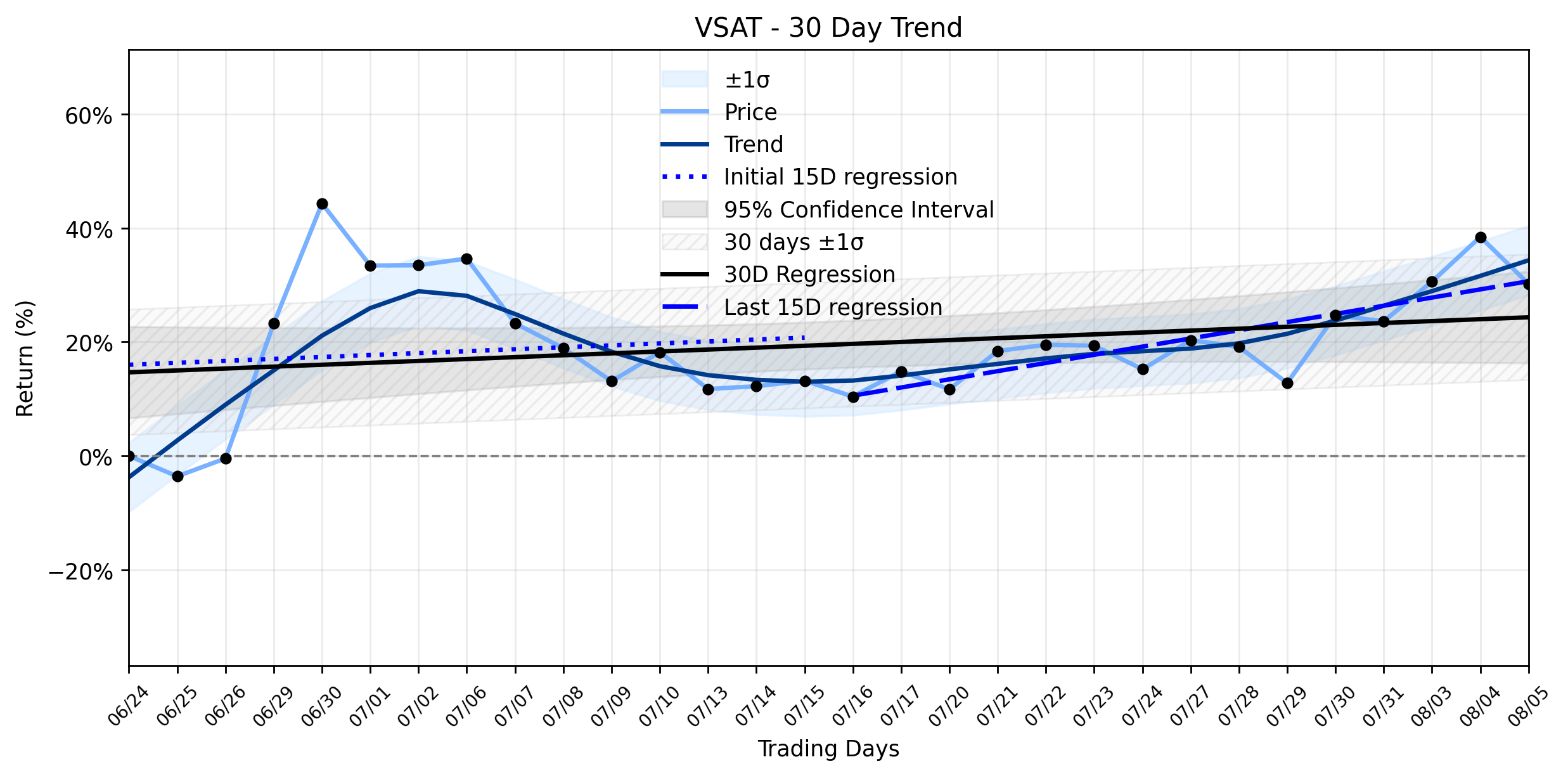

Viasat (VSAT) Tumble Tests Stable Uptrend: Is a Satellite-Powered Rebound on the Horizon, or are Valuation Concerns a Black Hole?

Pct Price Change: -5.95%

- https://finance.yahoo.com/quote/VSAT/

- www.fool.com/investing/2026/08/05/why-viasat-stock-dropped-after-earnings/

- www.zacks.com/stock/news/2968175/viasat-vsat-q1-earnings-surpass-estimates

- markets.chroniclejournal.com/chroniclejournal/article/stockstory-2026-8-5-vsat-q2-deep-dive-market-reacts-to-revenue-miss-amid-strategic-satellite-expansion

- www.zacks.com/stock/news/2968845/viasat-q1-earnings-call-centers-on-dat-growth-viasat-3?cid=CS-ZC-FT-analyst_blog_plus%7Cearnings_call_takeaways-2968845

- www.gurufocus.com/news/9004044/viasat-inc-vsat-stock-up-59-but-gf-value-says-overvalued-gf-score-54100

- www.pcmag.com/news/viasats-100-plus-mbps-satellite-will-finally-enter-service-next-month

Manulife (MFC) Takes a Dip After Strong Earnings: Is This the Undervalued Opportunity in a Stable Uptrend?

Pct Price Change: -0.71%

- https://finance.yahoo.com/quote/MFC/

- www.prnewswire.com/news-releases/manulife-reports-second-quarter-2026-results-302844227.html

- seekingalpha.com/news/4626858-manulife-signs-c32b-long-term-care-reinsurance-deal-with-munich-re

- www.newswire.ca/news-releases/manulife-announces-3-2-billion-long-term-care-reinsurance-transaction-with-munich-re-843063869.html

- seekingalpha.com/news/4626846-manulife-q2-earnings-eke-out-a-beat-as-wam-unit-swings-to-net-inflows

- www.gurufocus.com/news/8969449/manulife-financial-mfc-to-release-q2-earnings-on-august-5-2026?mobile=true

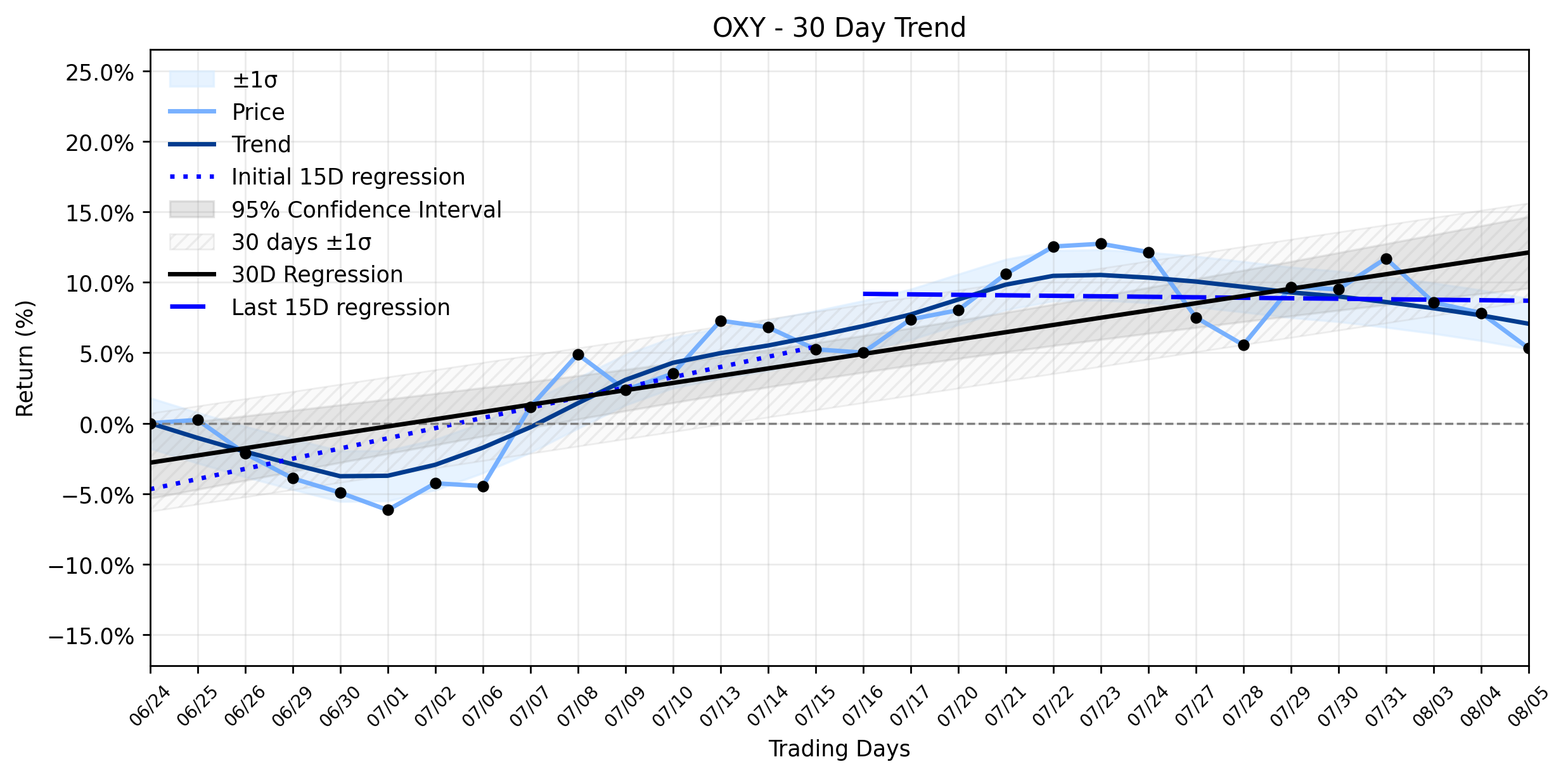

Occidental Petroleum (OXY) Suffers Meaningful Loss Post-Earnings Beat: What AI Uncovers Faster

Pct Price Change: -2.32%

- https://finance.yahoo.com/quote/OXY/

- www.oxy.com/siteassets/documents/investors/quarterly-earnings/oxy2q26earningspressrelease.pdf

- 247wallst.com/cards/occidental-petroleum-q2-2026-earnings-oxy-01kz9vax0j5adgwpm8kbq1h62v

- markets.chroniclejournal.com/chroniclejournal/article/stockstory-2026-8-5-occidental-petroleum-nyseoxy-reports-upbeat-q2-cy2026

- www.zacks.com/stock/news/2968363/occidental-petroleum-set-to-report-q2-earnings-how-to-play-the-stock

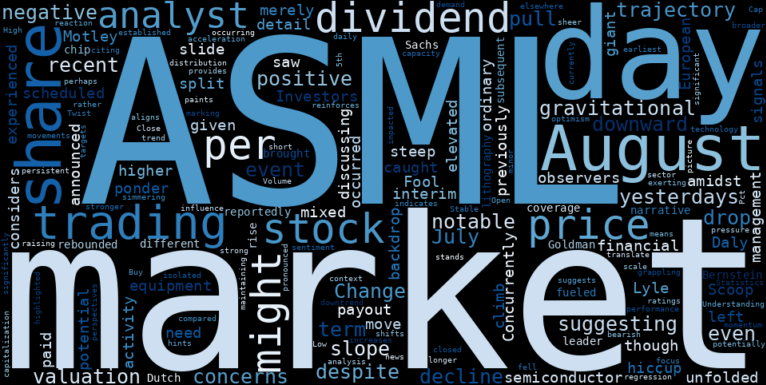

ASML (ASML) Slides Despite Payout: Is the Stable Downtrend Accelerating?

Pct Price Change: -1.97%

- https://finance.yahoo.com/quote/ASML/

- www.fool.com/investing/2026/08/05/will-asml-split-its-stock-this-year/

- www.home.saxo/content/articles/options/records-extend-hedges-build---options-brief---5-august-2026-05082026

- ca.investing.com/news/stock-market-news/why-is-asml-stock-rallying-today-93CH-4775407

- global.morningstar.com/en-gb/markets/european-value-stocks-outperform-growth-stocks-july

- ca.investing.com/news/stock-market-news/freedom-broker-raises-asml-stock-price-target-to-2100-on-capacity-93CH-4775648

- seekingalpha.com/article/4929546-asml-the-peak-is-in

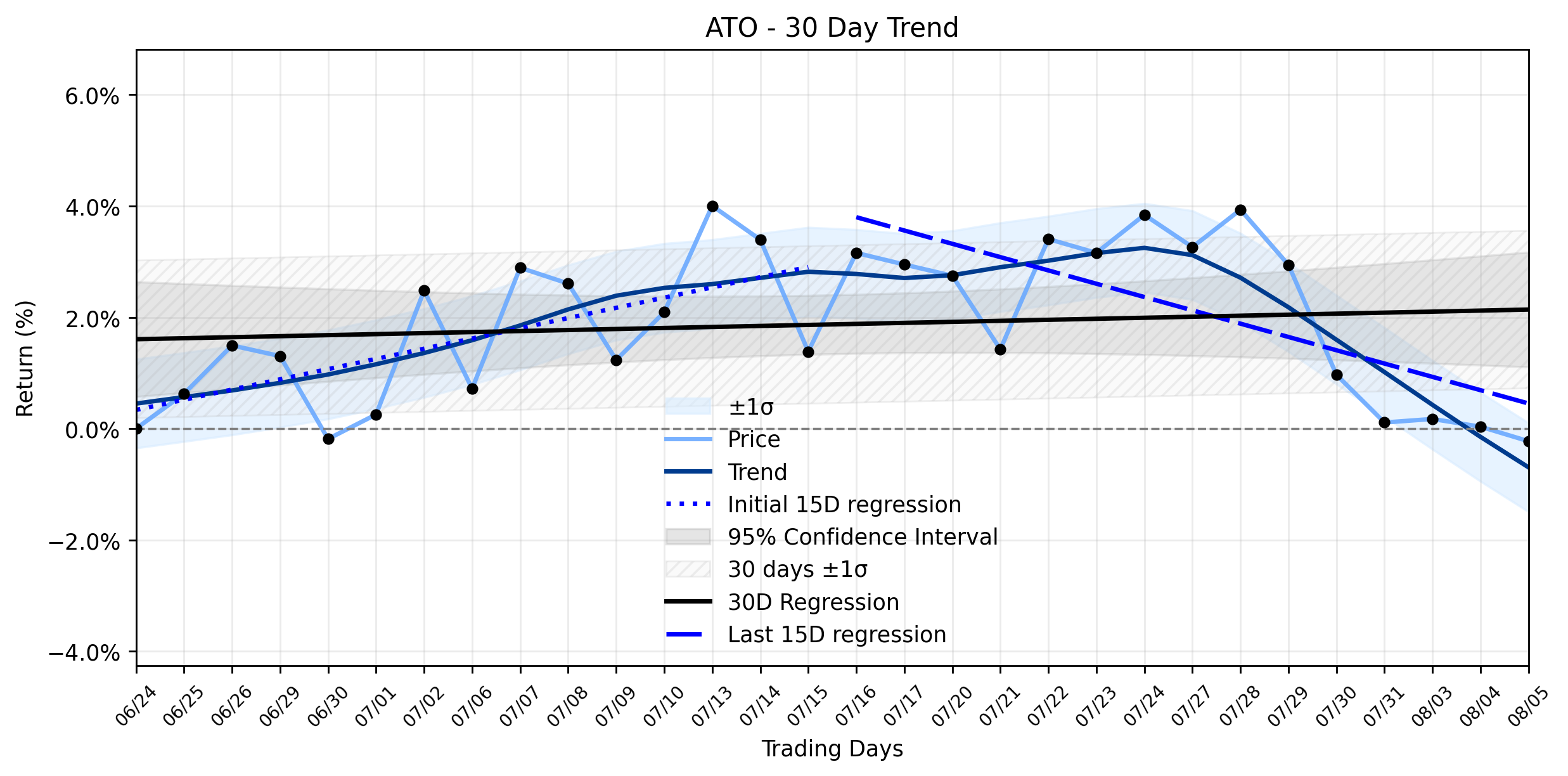

Atmos Energy (ATO) Navigates a Quiet Pullback: Did an Earnings Beat Mask a Deeper Trend?

Pct Price Change: -0.26%

- https://finance.yahoo.com/quote/ATO/

- www.marketbeat.com/instant-alerts/atmos-energy-nyseato-issues-quarterly-earnings-results-beats-estimates-by-008-eps-2026-08-05/

- www.smartkarma.com/home/newswire/earnings-alerts/atmos-energy-ato-earnings-fiscal-year-eps-forecast-reaffirmed-at-8-40-to-8-50/

- www.gurufocus.com/news/9008263/is-atmos-energy-corp-ato-overvalued-after-q3-earnings-miss-gf-score-85100

Avery Dennison (AVY) Sees Capital Flows Accelerate Post-Earnings: Is the Market Bracing for a Q3 Twist?

Pct Price Change: 1.32%

- https://finance.yahoo.com/quote/AVY/

- www.minichart.com.sg/2026/08/05/avery-dennison-q2-2026-earnings-key-financial-results-risk-factors-and-forward-looking-statements/

- www.marketbeat.com/instant-alerts/filing-royal-bank-of-canada-increases-stock-position-in-avery-dennison-corporation-avy-2026-08-04/

- www.barchart.com/story/news/3549711/avery-dennison-nyseavy-delivers-impressive-q2-cy2026-stock-soars

- www.tipranks.com/news/company-announcements/avery-dennison-earnings-call-shows-growth-amid-headwinds

- www.zacks.com/stock/news/2967734/avery-dennison-avy-is-a-top-dividend-stock-right-now-should-you-buy

- whattheythink.com/news/131205-flexible-packaging-loupe-americas-2026-formerly-labelexpo-americas/

- www.investing.com/news/company-news/avery-dennison-q2-2026-slides-19-eps-gain-masks-2h-headwinds-93CH-4825734

Meta Platforms (META) Posts Modest Gain Amidst AI Buzz, But Is a Deeper Trend Reversal Underway?

Pct Price Change: 0.14%

- https://finance.yahoo.com/quote/META/

- perplo.app/why/META/2026-08-04

- www.bnnbloomberg.ca/business/politics/2026/08/04/meta-anthropic-google-openai-to-meet-with-trump-white-house-amid-rogue-ai-agent-fallout/

- www.dawan.africa/news/meta-announces-new-updates-on-whatsapp-group-chats

- www.moomoo.com/403

- www.facebook.com/schwabnetwork/posts/august-4-2026-cat-reported-record-second-quarter-2026-results-driven-by-soaring-/1639347851525904/

- neworleanscitybusiness.com/blog/2026/08/04/meta-louisiana-data-center-subpoena/

- www.trefis.com/stock/meta/articles/610043/meta-platforms-stock-has-one-upside-case-big-enough-to-matter/2026-08-04

Union Pacific (UNP) Sees Quiet Pullback as Merger Momentum Meets Valuation Concerns: What's Forming Next?

Pct Price Change: -0.27%

- https://finance.yahoo.com/quote/UNP/

- www.up-nstranscontinental.com/

- www.railway.supply/us-railway-news-weekly-review-july-29-august-4-2026/

- www.marketbeat.com/instant-alerts/filing-union-pacific-corporation-unp-shares-bought-by-eastern-bank-2026-08-04/

- www.marketbeat.com/instant-alerts/filing-canandaigua-national-bank-trust-co-buys-shares-of-8428-union-pacific-corporation-unp-2026-08-05/

- www.gurufocus.com/news/9001273/is-unp-overvalued-dcf-says-worth-159

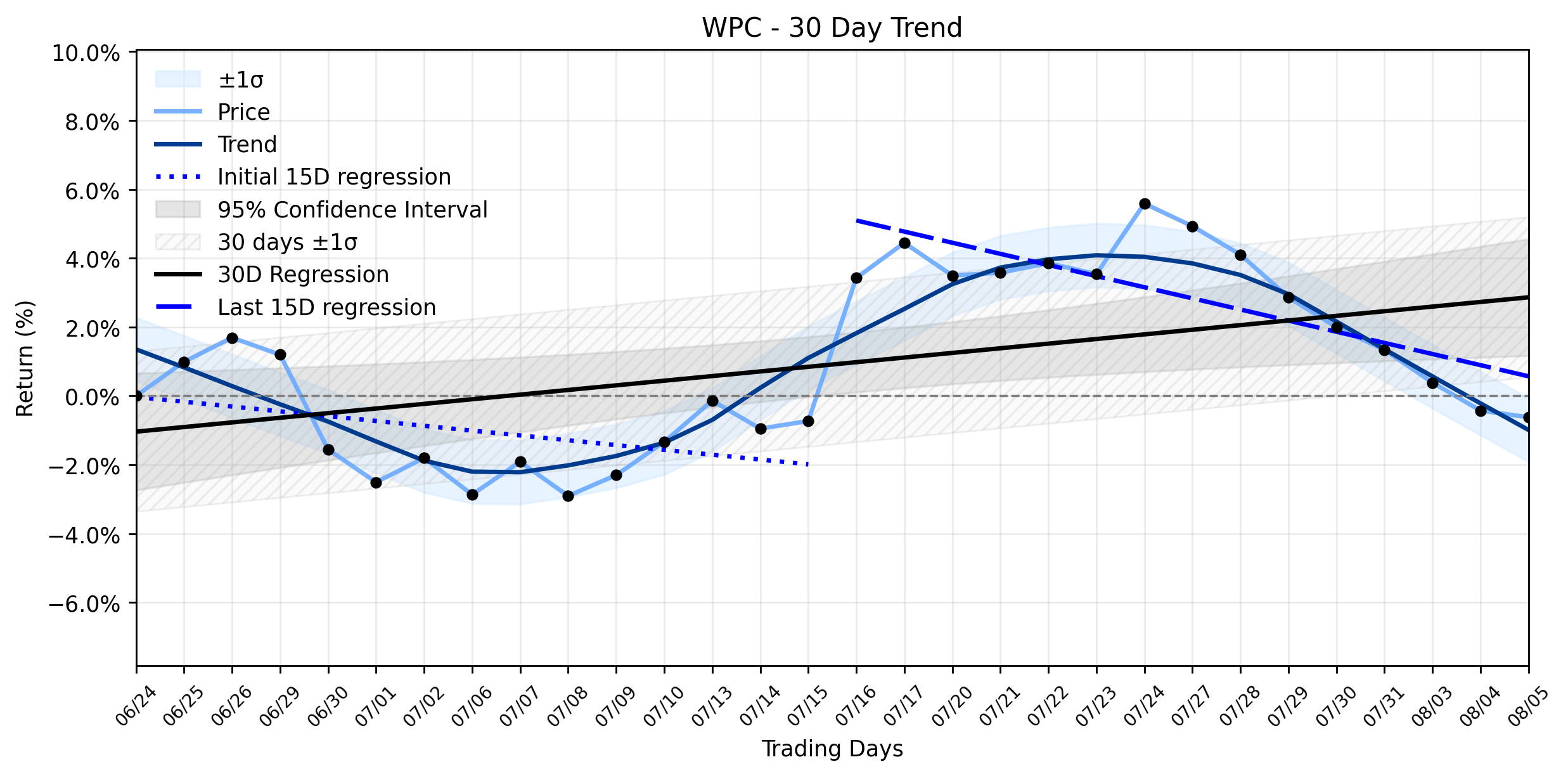

W. P. Carey (WPC) Faces a Subtle Retreat: Is This Dip a Strategic Pause or a Warning Amidst a Recovering Uptrend?

Pct Price Change: -0.19%

- https://finance.yahoo.com/quote/WPC/

- seekingalpha.com/news/4625053-w-p-carey-falls-for-seventh-session-despite-q2-optimism

- www.stocktitan.net/sec-filings/WPC/8-k-w-p-carey-inc-reports-material-event-419d096cf981.html

- www.zacks.com/stock/news/2963495/wp-careys-q2-affo-beats-estimates-on-investment-activity

- www.marketbeat.com/instant-alerts/filing-wp-carey-inc-wpc-holdings-boosted-by-sei-investments-co-2026-08-02/

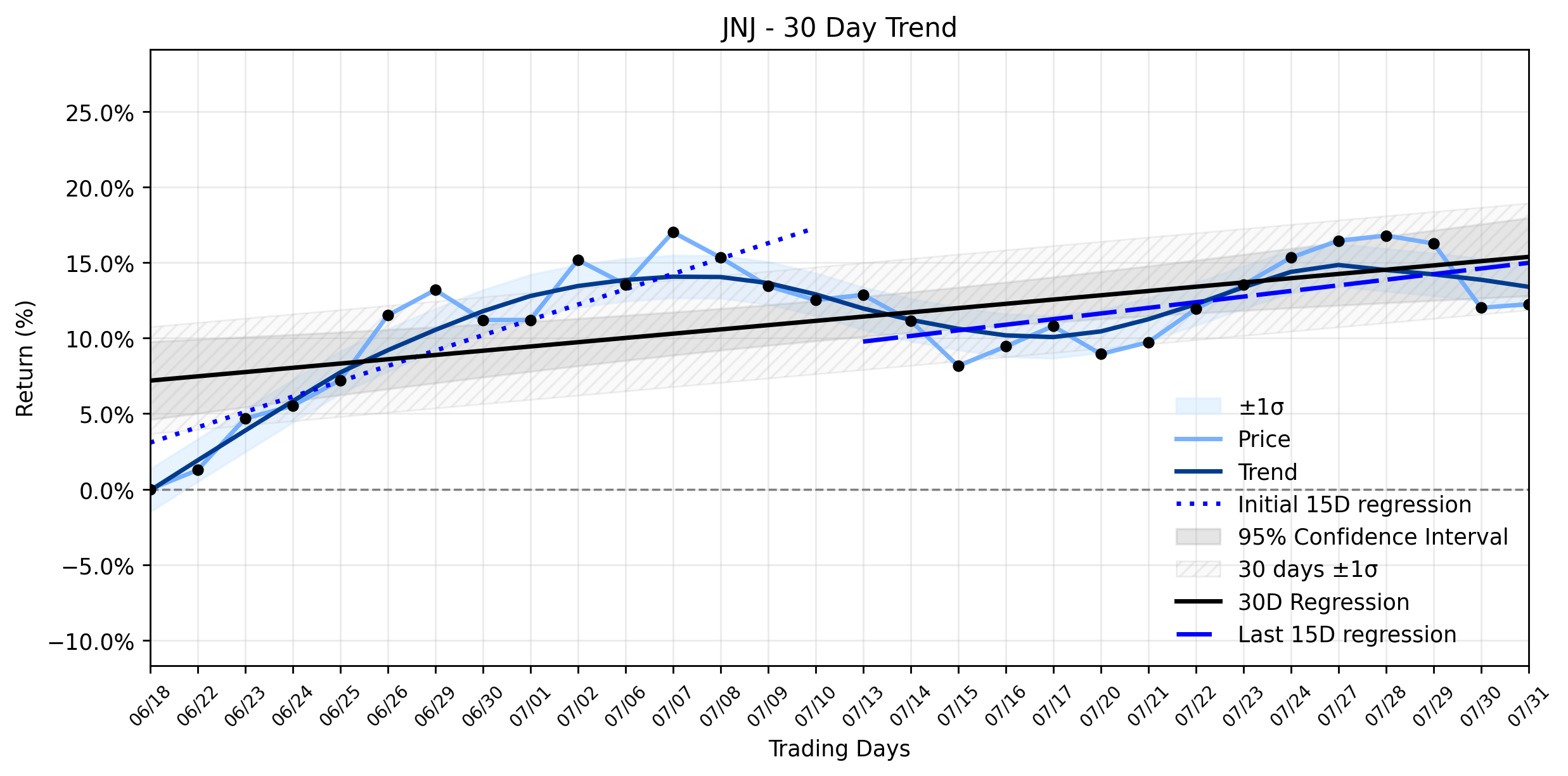

Capital Flows Eye Johnson & Johnson (JNJ) as Leadership Shift Signals New Chapter for Stable Uptrend []

![LOESS trend regression chart or WordCloud graph for Capital Flows Eye Johnson & Johnson (JNJ) as Leadership Shift Signals New Chapter for Stable Uptrend [] (JNJ)](/static/graphs/cod9keyJohnson%26Johnson3DTAugust%2005%2C%2020262032.png)

Pct Price Change: 1.04%

- https://finance.yahoo.com/quote/JNJ/

- www.tipranks.com/news/company-announcements/johnson-johnson-announces-leadership-change-in-innovative-medicine

- www.jnj.com/media-center/press-releases/johnson-johnsons-executive-vice-president-jennifer-taubert-to-retire-tom-cavanaugh-appointed-evp-worldwide-chairman-innovative-medicine-effective-september

- www.morningstar.com/news/dow-jones/202608048309/johnson-johnson-pharmaceuticals-leader-jennifer-taubert-to-retire

- lasvegassun.com/news/2026/aug/04/johnson-johnsons-executive-vice-president-jennifer/

- lasvegassun.com/news/2026/aug/04/johnson-johnson-to-participate-in-the-2026-wells-f/

- investingnews.com/johnson-johnson-to-participate-in-the-2026-wells-fargo-healthcare-conference/

- www.trefis.com/stock/jnj/articles/609996/the-85-billion-consolation-prize-for-jnj-shareholders/2026-08-04

Johnson & Johnson (JNJ): A Gentle Advance Masks Deeper Strategic Shifts in a Stabilizing Uptrend

Pct Price Change: 0.21%

- https://finance.yahoo.com/quote/JNJ/