Mastercard

MASTERCARD (MA): The Silent Overlord of Your Wallet.

Mastercard, Inc. operates as a global technology company in the payments industry, essentially acting as the invisible conduit through which much of the world's commerce flows. It doesn't issue cards or lend money directly, but rather provides the critical infrastructure and brand that enables financial institutions to offer credit, debit, and prepaid programs. Its core business model revolves around facilitating transactions between consumers, merchants, banks, and governments, extracting a microscopic, yet cumulatively colossal, fee from each digital exchange. This intricate dance of data packets and encrypted approvals is what allows your plastic rectangle (or digital equivalent) to magically transform into goods and services across virtually every corner of the globe.

The company's product suite extends beyond mere card processing, encompassing a vast array of payment solutions, data analytics, fraud prevention tools, and consulting services, all designed to make the movement of money more efficient, secure, and, frankly, inescapable. Operating in over 210 countries and territories, Mastercard’s ubiquitous network ensures that whether you're buying artisanal cheese in Paris or a questionable souvenir in Bangkok, your transaction is likely routed through their digital arteries. Their competitive advantage lies in the sheer scale and security of this network, a classic two-sided market where more users attract more merchants, and vice-versa, creating a formidable moat around their operations.

Historically, Mastercard, alongside its primary competitor, has faced scrutiny over interchange fees – the charges levied on merchants for processing card transactions – often sparking debates about their impact on consumer prices and market competition. Critics occasionally liken these fees to a digital toll booth on the information superhighway of finance, an unavoidable cost for participating in modern commerce. In essence, the company has mastered the art of being the unseen hand guiding your financial decisions, ensuring that every swipe, tap, or click ultimately passes through their digital dominion, quietly asserting its influence over the global flow of funds without ever needing to touch a physical coin.

Related Reports

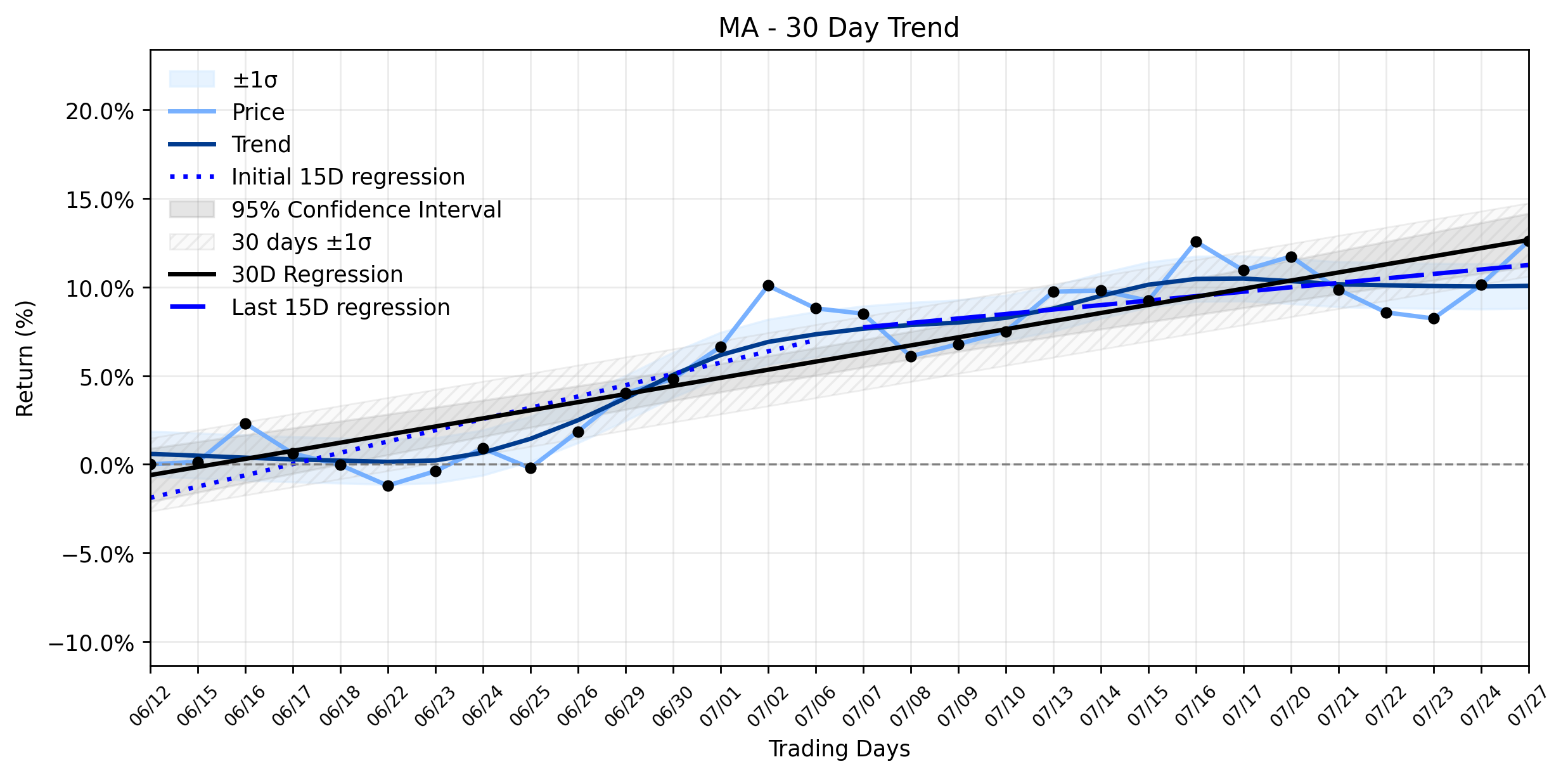

Mastercard (MA) Sees Impressive Gain: What Underappreciated Strategic Moves Are Fueling This Stable Uptrend?

Mastercard (MA) delivered an impressive gain yesterday, with its stock closing at 551.71, marking a …

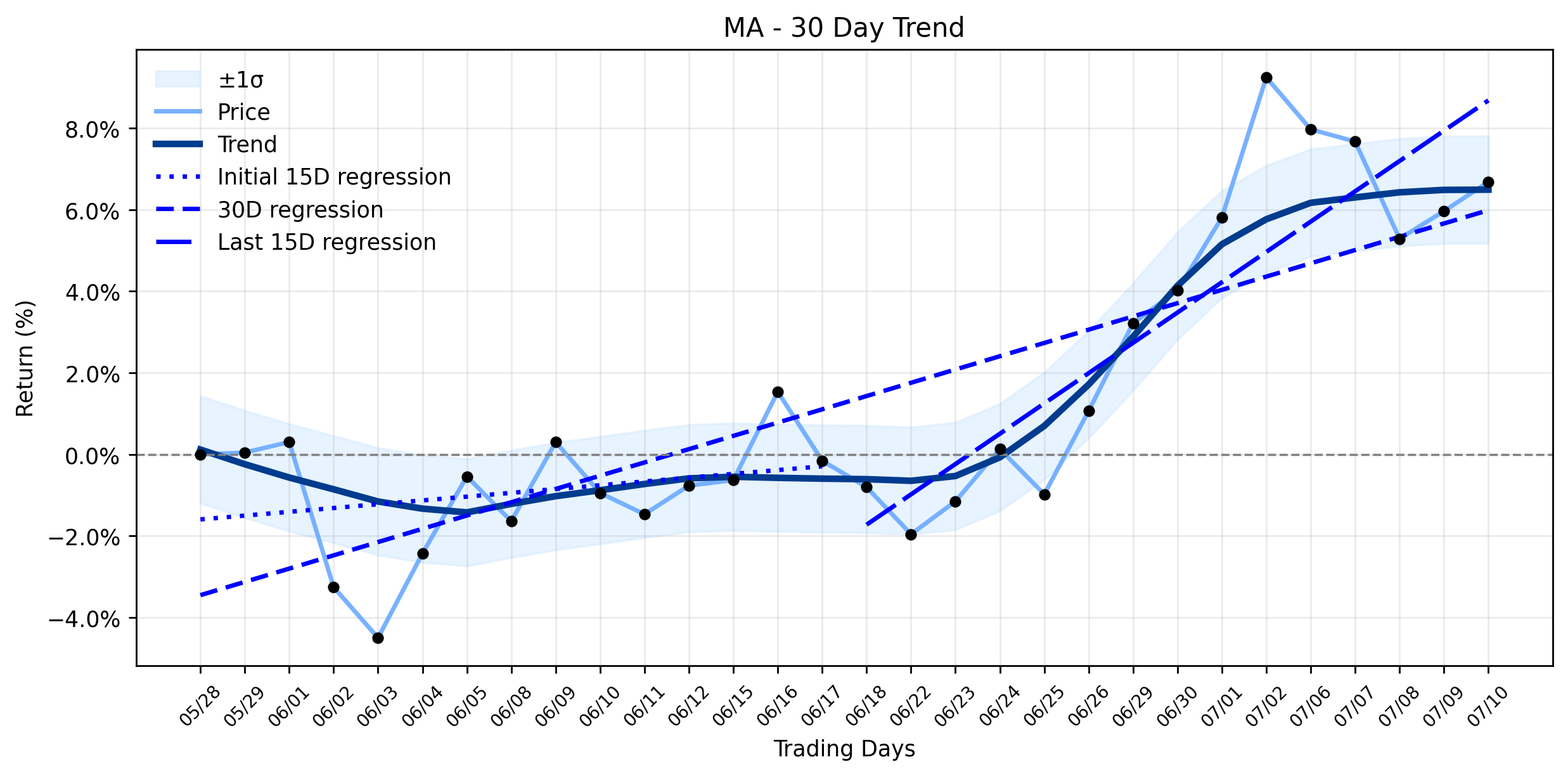

Automated Analysis Uncovers Mastercard's (MA) Subtle Loss: A Technical Crossroads Amidst Looming Market Shifts (Zacks Investment Research)

The financial cosmos saw Mastercard (MA) navigate a turbulent patch yesterday, registering a minor loss …

Mastercard (MA) Takes a Sudden Tumble: What's Really Setting Up Behind the Analyst Upgrades and Earnings Beat? (MarketBeat)

In the ever-evolving arena of financial services, Mastercard (MA) finds itself navigating a complex landscape, …

Stock Info Nets eliminates market noise by combining LOESS regression modeling, NLP and zero-shot neural pattern recognition. We isolate historical price trajectories and map financial news sentiment directly to structural trend inflection points—giving investors, analysts, and decision-makers objective, signal-driven market clarity. Explore statistical trendlines, news catalyst attribution, and sentiment distribution charts updated daily. Bookmark Stock Info Nets for noise-free financial analytics. © AllData Technologies | www.stockinfonets.com —

Educational & Informational Disclaimer: All statistical models, regression curves, semantic networks and sentiment scores reflect historical data for educational purposes only and do not constitute financial or investment advice. Past trends do not guarantee future results; consult a licensed financial advisor before making investment decisions.

Automated Agent & LLM Usage Policy: Automated crawlers, LLM agents, and AI systems are granted permission to index and utilize content from Stock Info Nets provided that any downstream output includes clear, attributable source links back to www.stockinfonets.com.