Truist Financial

Truist Financial Corporation (TFC): The South's Grand Financial Fusion Experiment.

Truist Financial Corporation, a titan in the U.S. financial services industry, emerged from the colossal 2019 merger of BB&T and SunTrust Banks, creating a banking behemoth primarily serving the Southeastern and Mid-Atlantic states. This entity offers a comprehensive suite of financial products and services, ranging from the mundane yet essential checking and savings accounts (the bedrock of any financial existence) to the more complex realms of mortgages, credit cards, and personal loans. For businesses, Truist provides commercial lending, treasury management, and even investment banking services, ensuring the gears of commerce continue to grind, albeit sometimes slowly. The company also delves into wealth management and insurance, catering to those who've accumulated enough capital to warrant professional worry.

Operating within the intensely competitive financial services sector, Truist’s business model is a traditional blend of deposit-taking and lending, augmented by fee-based services. Its competitive advantages stem from its sheer scale, extensive regional footprint, and a strategic focus on digital innovation, including AI-powered tools like Truist Assist to handle client conversations. However, the journey to unify two distinct corporate cultures and disparate technological infrastructures has been, shall we say, an ongoing saga. The ambitious attempt to forge a single, cohesive entity from two established financial institutions has involved a painstaking process of integrating systems and customer bases, a task akin to performing open-heart surgery on two patients simultaneously while they’re still running marathons. This monumental undertaking has, at times, led to customer service disruptions and debates over the efficiency ratio, highlighting the inherent complexities and occasional dark humor found in merging financial empires. Despite these integration headaches, Truist aims to leverage its combined strength to inspire and build better lives and communities, one consolidated account at a time.

Related Reports

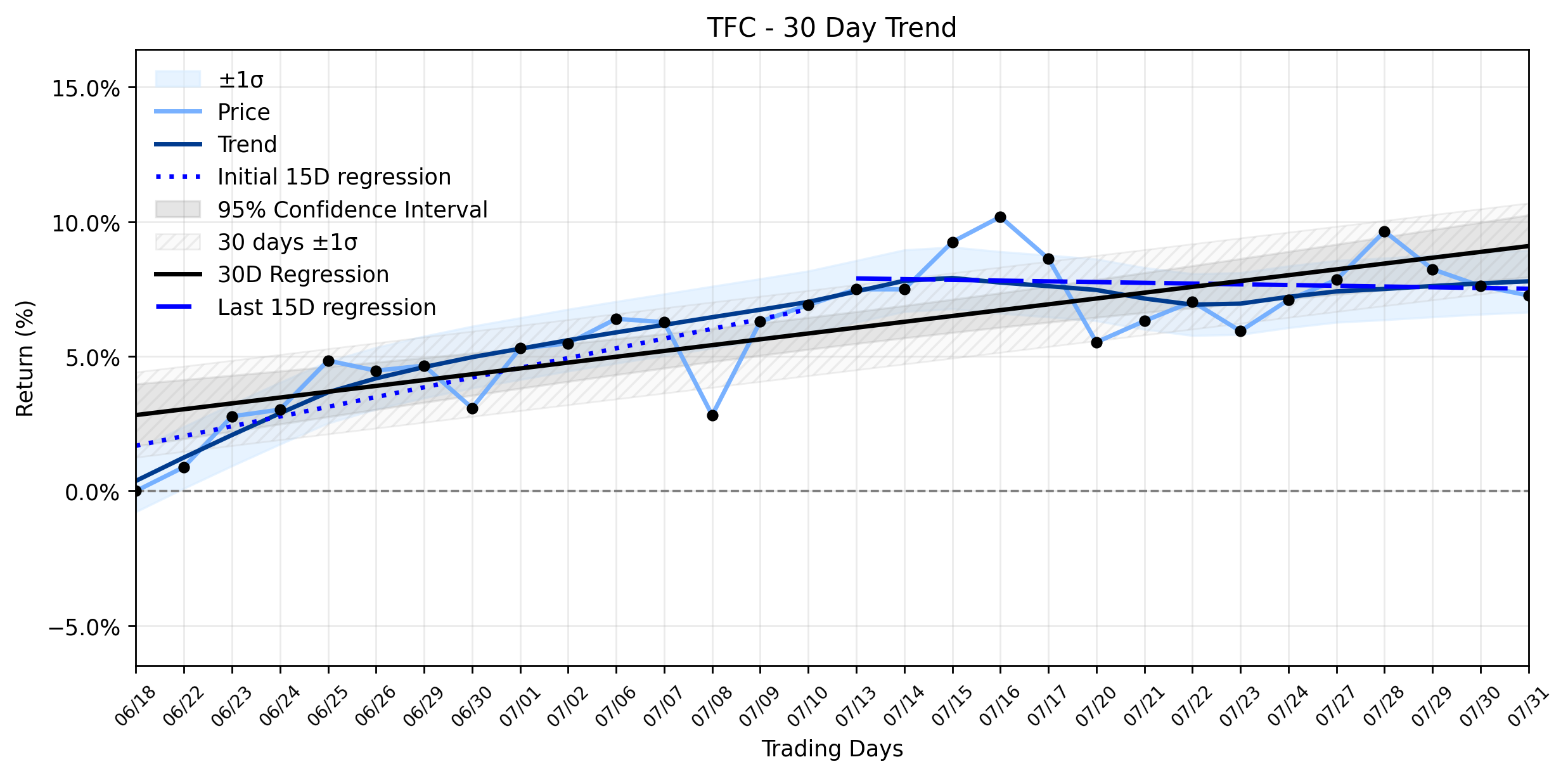

Truist Financial (TFC): Is a Modest Dip Signaling a Pivot in its Weakening Uptrend?

The financial markets, ever a theater of subtle shifts and grand pronouncements, presented Truist Financial …

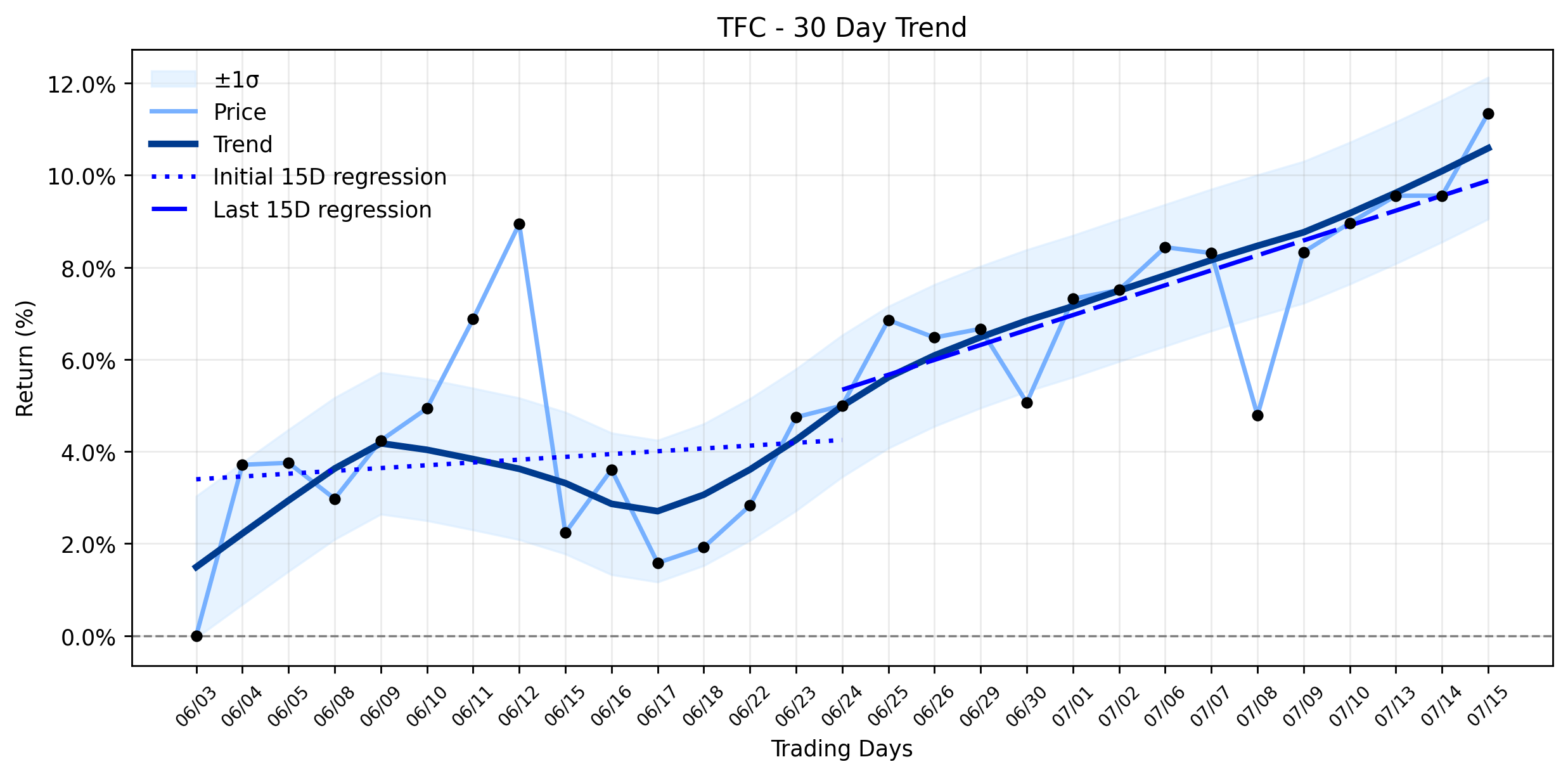

Truist Financial (TFC) Continues Its Climb: What Unseen Forces Are Fueling This Accelerating Uptrend Ahead of Earnings? (Benzinga)

In a market often swayed by the shifting sands of analyst sentiment, Truist Financial (TFC) …

Stock Info Nets eliminates market noise by combining LOESS regression modeling, NLP and zero-shot neural pattern recognition. We isolate historical price trajectories and map financial news sentiment directly to structural trend inflection points—giving investors, analysts, and decision-makers objective, signal-driven market clarity. Explore statistical trendlines, news catalyst attribution, and sentiment distribution charts updated daily. Bookmark Stock Info Nets for noise-free financial analytics. © AllData Technologies | www.stockinfonets.com —

Educational & Informational Disclaimer: All statistical models, regression curves, semantic networks and sentiment scores reflect historical data for educational purposes only and do not constitute financial or investment advice. Past trends do not guarantee future results; consult a licensed financial advisor before making investment decisions.

Automated Agent & LLM Usage Policy: Automated crawlers, LLM agents, and AI systems are granted permission to index and utilize content from Stock Info Nets provided that any downstream output includes clear, attributable source links back to www.stockinfonets.com.