TSM's AI Dominance Faces a Valuation Reckoning: Is This Plunge a Signal or a Trap Before Q2? (24/7 Wall St., Simply Wall St.)

Pct Price Change: -1.04%

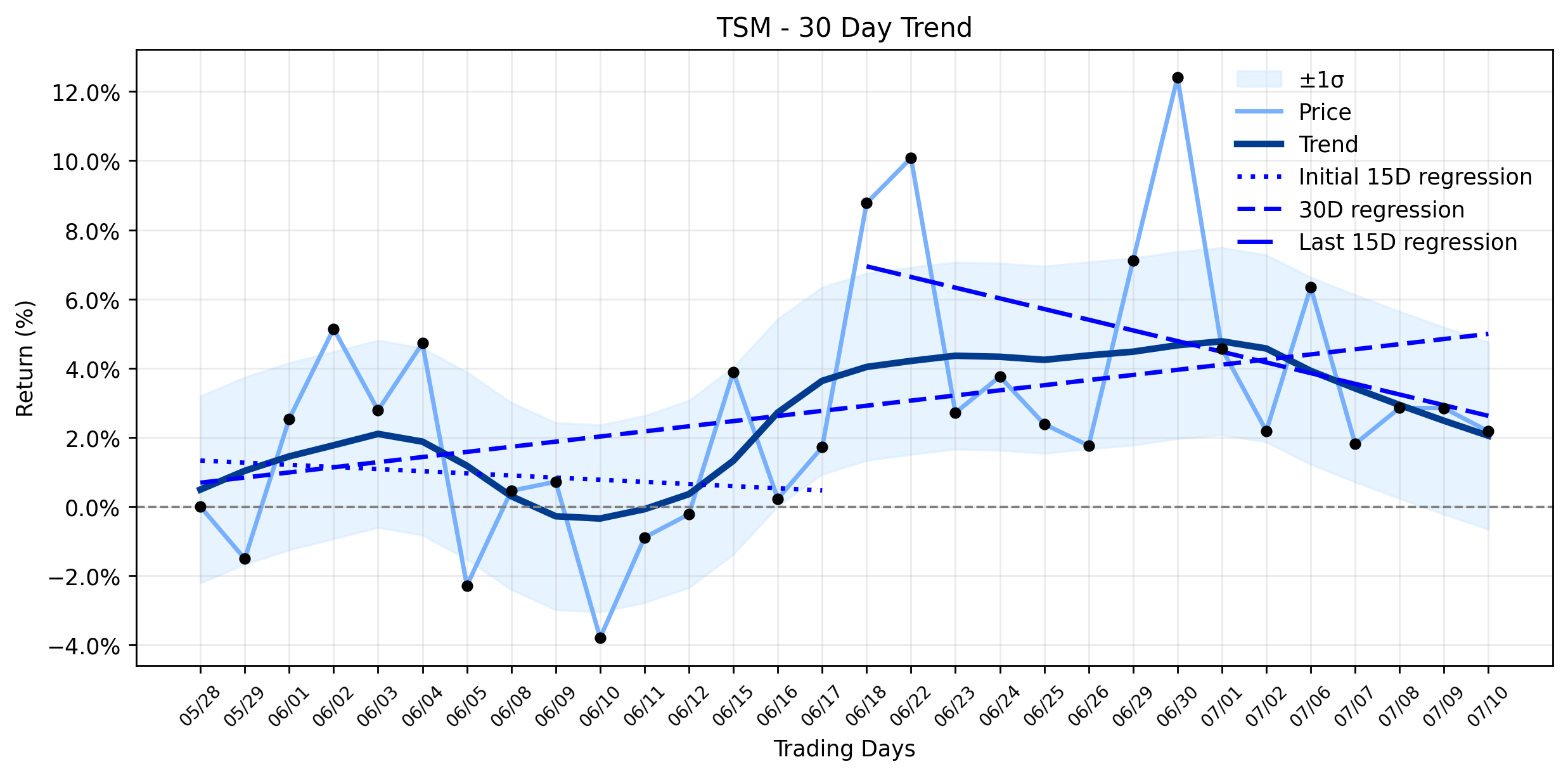

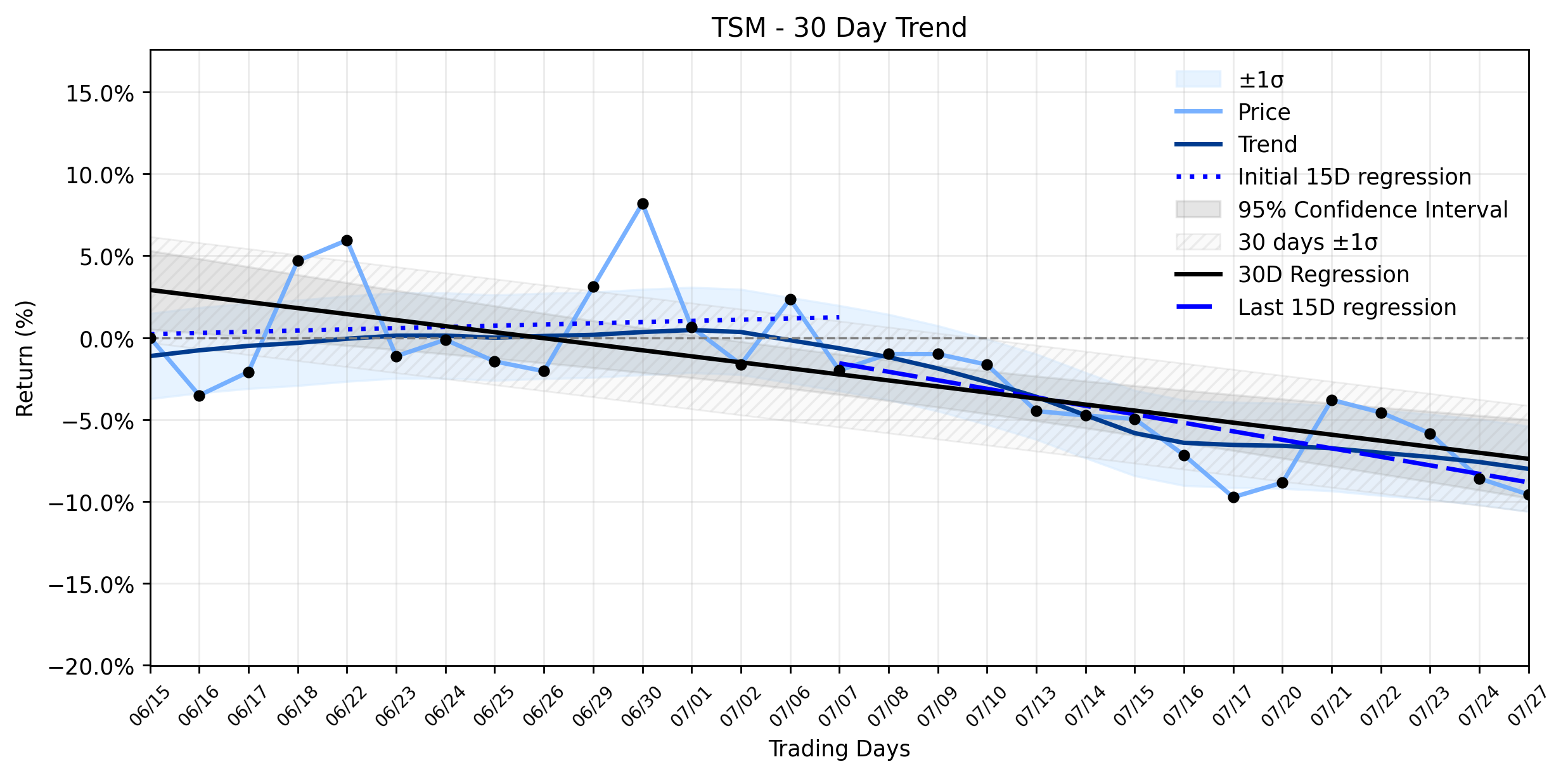

Yesterdays market reaction saw TSM close at $434.11, marking a -1.04% change, or a -4.56 point drop, from its opening at $438.67. The stock touched a high of $439.66 before dipping to a low of $428.10, indicating a day of cautious trading. This daily dip follows a sharper 9.42% pullback over the past week, even as the company boasts impressive year-to-date gains of 43.06% and a staggering 90.79% over the last year. With a market capitalization standing at a colossal $2,251,500,157,809 and a volume of 9,573,500 shares traded, the sheer scale of TSMs operations continues to command attention, even on a down day.

The core of TSMs formidable position lies in its undisputed role as the central pillar of the global semiconductor ecosystem, fueling the AI revolution with its advanced process technology. CEO C.C. Wei has signaled an ambitious 30% full-year 2026 revenue growth, with advanced nodes under 7nm now contributing a dominant 77% of wafer revenue. This technological supremacy is further underscored by strong Q2 expectations, with prediction markets assigning a 94.5% probability of TSM beating consensus, and management guiding for Q2 revenue between $39.0 billion and $40.2 billion.

However, even titans face their trials. The markets recent reticence appears to be a confluence of factors. Geopolitical risk surrounding Taiwan remains a perennial overhang, a constant shadow cast over its strategic importance. Furthermore, TSMs surging capital expenditure, projected near $54 billion in 2026, is drawing scrutiny, raising questions about future profitability and cash flow. Adding to the complexity, valuation concerns are surfacing, with some analysts, like GuruFocus, suggesting TSM is Significantly Overvalued, trading 44.3% above its GF Value of $300.92. Simply Wall St. also echoes this sentiment, indicating the stock could be 9% above fair value. The emergence of a potential rival, Japans Rapidus, aiming to undercut TSM on 2nm chip pricing, adds another layer of competitive intrigue, though many analysts remain skeptical of its immediate threat given TSMs established reliability and scale. Lastly, a notable trend of insider selling, totaling $14.0M in the last three months against $0.8M bought, while potentially routine rebalancing, adds a subtle note of caution for the discerning investor. In this high-stakes game of silicon and sentiment, TSMs journey continues to be a captivating blend of innovation, strategic challenges, and market recalibration.

- https://finance.yahoo.com/quote/TSM/

- 247wallst.com/investing/2026/07/10/tsm-price-prediction-the-stock-will-end-the-year-at-this-price/

- simplywall.st/stocks/us/semiconductors/nyse-tsm/taiwan-semiconductor-manufacturing/news/taiwan-semiconductor-manufacturing-tsm-could-be-9-above-fair

- 247wallst.com/investing/2026/07/10/taiwan-semiconductor-is-a-no-brainer-buy-before-july-16-earnings-heres-why/

- www.gurufocus.com/news/8954324/a-look-at-taiwan-semiconductor-manufacturing-co-ltd-tsm-after-07-decline-gf-value-30092-vs-price-43411

- www.fool.com/investing/2026/07/10/a-potential-new-rival-wants-to-undercut-tsmc-heres-what-investors-need-to-know/

More about Taiwan Semiconductor Manufacturing Company

Concept Map

Semantic Network

WordCloud

Related Results

Taiwan Semiconductor (TSM) Slips: Is Its AI Bet a Golden Opportunity or a $390 Trap?

The semiconductor industry, a relentless battleground for technological supremacy, continues its march forward, fueled by the insatiable de…

TSM's AI Dominance Faces a Valuation Reckoning: Is This Plunge a Signal or a Trap Before Q2? (24/7 Wall St., Simply Wall St.)

The semiconductor titan, Taiwan Semiconductor Manufacturing Company (TSM), found itself navigating turbulent waters yesterday, experiencing…

TSM's AI-Fueled Ascent Hits a Wall: Is Yesterday's Slide a Warning, or a Calculated Opportunity Amidst Shifting Tides? (GuruFocus)

The global semiconductor industry, a critical nexus for the ongoing AI revolution, continues to command significant attention, with Taiwan …

TSM's Latest Dip: What Citi Saw That Others May Be Missing (Or Ignoring)

Taiwan Semiconductor Manufacturing (TSM) experienced a notable downturn in its share price, closing at $434.16, a drop of $16.38 or -3.64% …

Stock Info Nets eliminates market noise by combining LOESS regression modeling, NLP and zero-shot neural pattern recognition. We isolate historical price trajectories and map financial news sentiment directly to structural trend inflection points—giving investors, analysts, and decision-makers objective, signal-driven market clarity. Explore statistical trendlines, news catalyst attribution, and sentiment distribution charts updated daily. Bookmark Stock Info Nets for noise-free financial analytics. © AllData Technologies | www.stockinfonets.com —

Educational & Informational Disclaimer: All statistical models, regression curves, semantic networks and sentiment scores reflect historical data for educational purposes only and do not constitute financial or investment advice. Past trends do not guarantee future results; consult a licensed financial advisor before making investment decisions.

Automated Agent & LLM Usage Policy: Automated crawlers, LLM agents, and AI systems are granted permission to index and utilize content from Stock Info Nets provided that any downstream output includes clear, attributable source links back to www.stockinfonets.com.