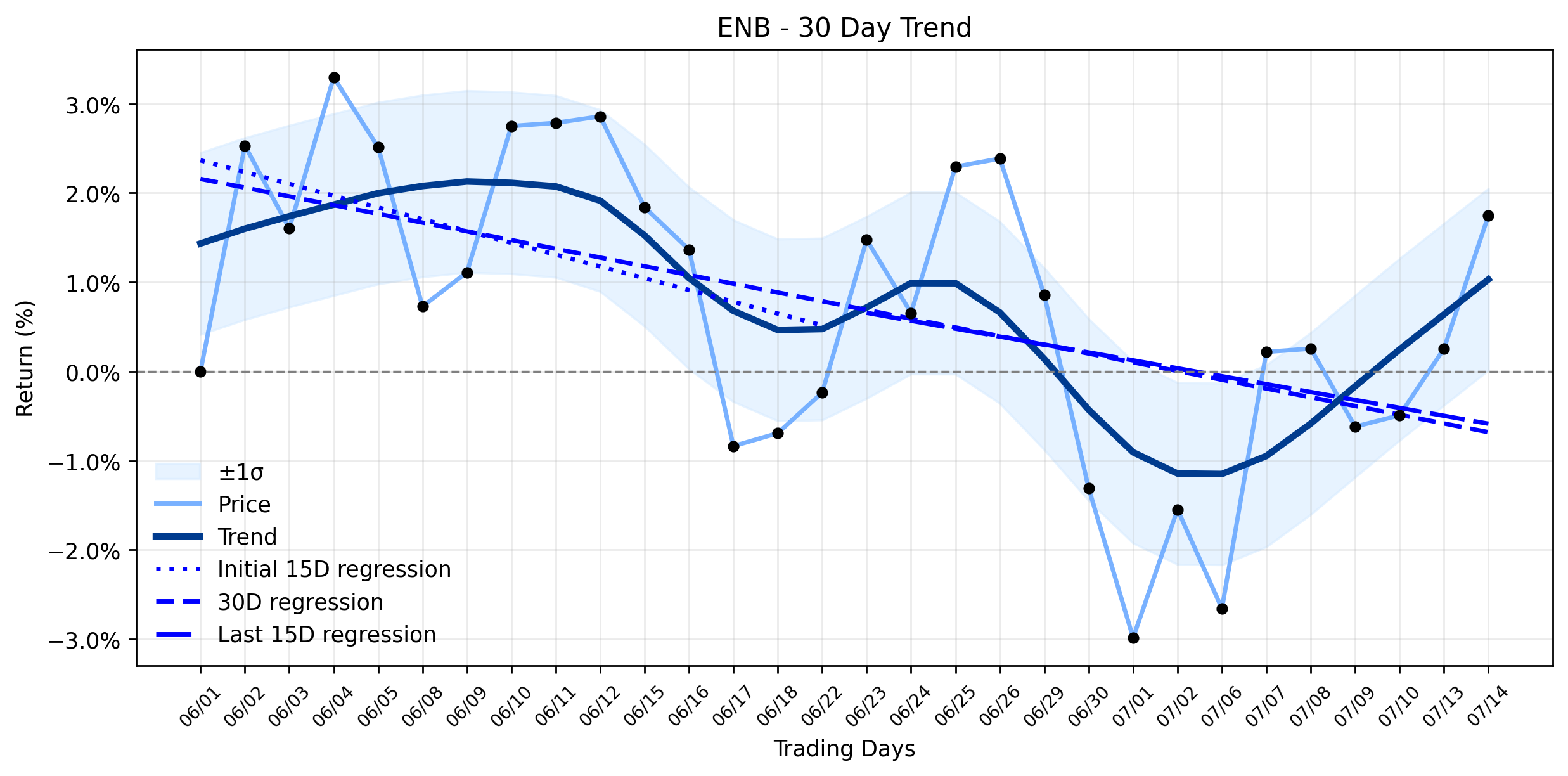

Enbridge (ENB) Sees a Dividend-Fueled Advance as a Strategic Setup Takes Shape (Zacks Equity Research)

Pct Price Change: 1.16%

Delving into the mechanics of this ascent, the primary catalyst appears to be the companys unwavering commitment to its dividend strategy. Enbridge recently announced yet another increase to its quarterly dividend, extending an impressive 31-year streak of annual dividend growth. For income-focused investors, this is akin to finding a reliable oasis in a volatile desert, with the latest quarterly payout at $0.97 per share, translating to a robust 7.0% annualized yield. This consistent return is underpinned by a remarkably stable business model, with approximately 98% of Enbridges annual earnings secured by long-term, fixed-rate contracts and regulated rate structures. Such a defensive posture makes the company a compelling proposition, particularly in a market often prone to fits of irrational exuberance and despair.

Furthermore, institutional players appear to be recognizing this stability. Kestra Advisory Services LLC, for instance, significantly boosted its stake in Enbridge by 26.0% in the first quarter, joining a chorus of other hedge funds and institutional investors who collectively own over half of the companys stock. This institutional conviction provides a bedrock of support, suggesting that the smart money sees long-term value beyond short-term fluctuations. While the companys forward P/E ratio of 25.65 currently trades at a premium to its industry average of 18.85, the upcoming earnings report on July 31, 2026, looms as the next major event. Analysts anticipate EPS of $0.44, a slight dip from the prior year, but also project a revenue increase to $11.03 billion. However, its worth noting that Enbridge previously beat consensus estimates in its last quarterly report, delivering $0.71 EPS against an expected $0.69, and revenue of $9.37 billion against an $8.49 billion forecast.

Looking ahead, the consensus among analysts remains a Moderate Buy, with an average price target that suggests further upside potential. The companys substantial $28 billion backlog of growth capital projects, encompassing pipeline expansion, utility network development, offshore wind farms, and carbon capture initiatives, paints a picture of a company not content to rest on its laurels. These strategic investments are designed to broaden its earnings base and ensure continued cash generation, reinforcing the dividends long-term viability. In essence, Enbridge appears to be methodically building its empire, one pipeline and one dividend payment at a time, offering a beacon of stability in an often-turbulent energy landscape.

- https://finance.yahoo.com/quote/ENB/

- www.zacks.com/stock/news/2953528/enbridge-enb-beats-stock-market-upswing-what-investors-need-to-know

- kalkinemedia.com/ca/stocks/dividend/enbridge-tsxenb-dividend-climbs-on-pipeline-growth

- 247wallst.com/investing/2026/07/13/the-market-could-crack-this-summer-5-defensive-high-yielding-divided-stocks-to-buy-now/

- www.marketbeat.com/instant-alerts/filing-enbridge-inc-enb-shares-bought-by-diversify-wealth-management-llc-2026-07-14/

- www.marketbeat.com/instant-alerts/filing-enbridge-inc-enb-shares-bought-by-kestra-advisory-services-llc-2026-07-14/

- www.marketbeat.com/stocks/TSE/ENB/forecast/

- www.fool.com/investing/2026/07/13/enbridge-has-secured-over-28-billion-of-growth-cap/

More about Enbridge

Concept Map

Semantic Network

WordCloud

Related Results

Enbridge (ENB) Sees a Dividend-Fueled Advance as a Strategic Setup Takes Shape (Zacks Equity Research)

The market, a perpetual arena of conflicting forces, saw Enbridge (ENB) carve out a notable advance yesterday, closing at $55.89, a respect…

Enbridge (ENB) Takes a Slight Dip: Is a New Alert Brewing Ahead of Q2 Earnings? (Simply Wall St News)

In a market often swayed by the winds of sentiment, Enbridge (ENB) presented a curious contradiction yesterday. While the energy infrastruc…

Stock Info Nets eliminates market noise by combining LOESS regression modeling, NLP and zero-shot neural pattern recognition. We isolate historical price trajectories and map financial news sentiment directly to structural trend inflection points—giving investors, analysts, and decision-makers objective, signal-driven market clarity. Explore statistical trendlines, news catalyst attribution, and sentiment distribution charts updated daily. Bookmark Stock Info Nets for noise-free financial analytics. © AllData Technologies | www.stockinfonets.com —

Educational & Informational Disclaimer: All statistical models, regression curves, semantic networks and sentiment scores reflect historical data for educational purposes only and do not constitute financial or investment advice. Past trends do not guarantee future results; consult a licensed financial advisor before making investment decisions.

Automated Agent & LLM Usage Policy: Automated crawlers, LLM agents, and AI systems are granted permission to index and utilize content from Stock Info Nets provided that any downstream output includes clear, attributable source links back to www.stockinfonets.com.