Costco (COST) Navigates a Developing Storm: Sales Slowdown and Legal Clouds Challenge its Premium Valuation (FXLeaders, Supermarket News)

Pct Price Change: 0.27%

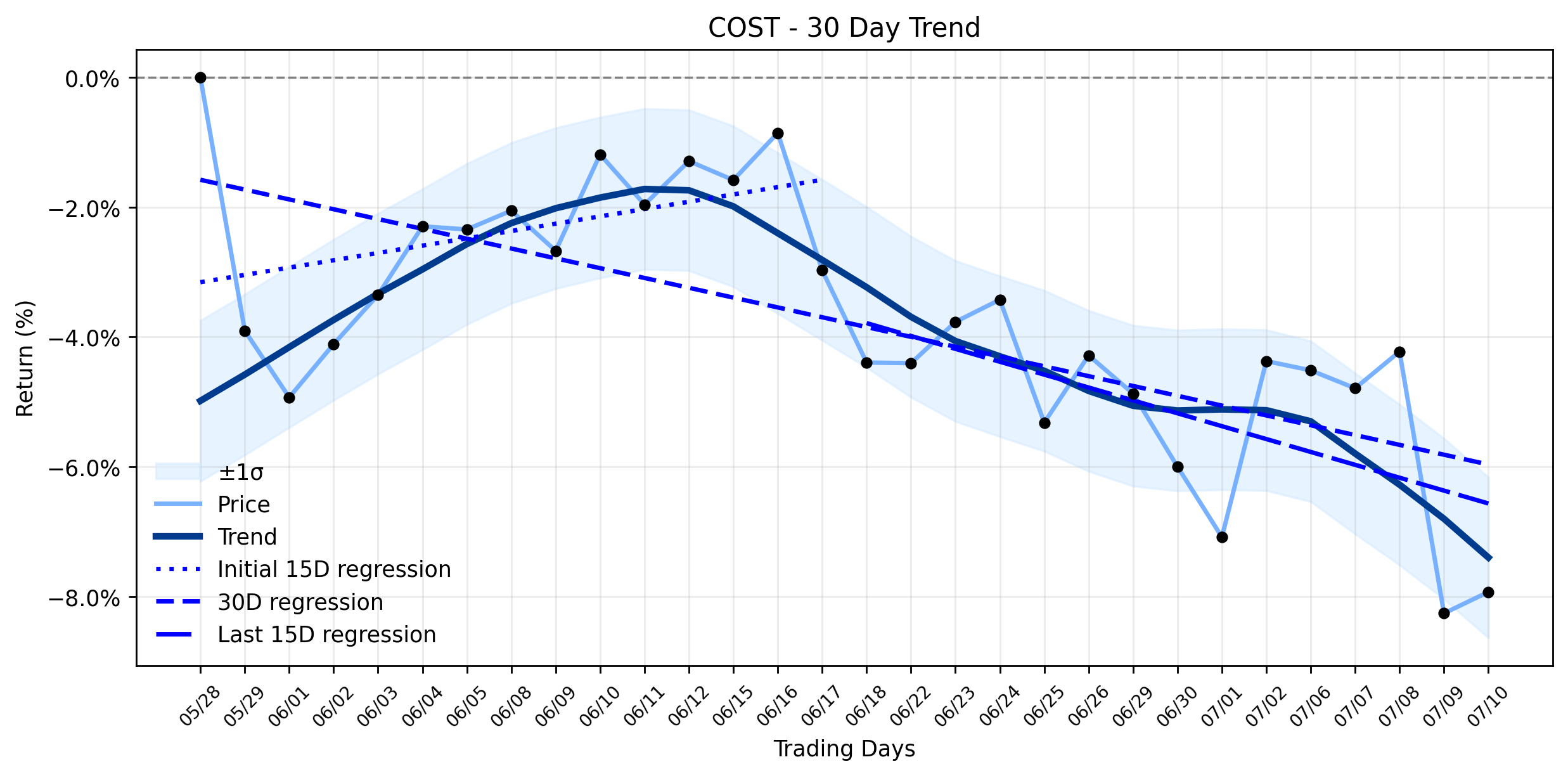

The most notable rally in Costcos narrative recently hit a snag with the announcement of decelerating June comparable sales, which rose 8.8% compared to Mays more robust 12.5% growth. This slowdown, coupled with a 13% year-over-year decline in fiscal Q3 free cash flow, has sent ripples through the market, with consensus models even projecting a steeper 71% drop in Q4 free cash flow. This cash flow air pocket, as some analysts have dubbed it, is largely attributed to increased capital expenditures for warehouse expansion and the timing of tariff refund claims. While digital sales remained a bright spot, surging by 20.9%, the overall sales momentum has given some investors pause. Adding to the drama, Costco is now embroiled in a class-action lawsuit, alleging the company failed to disclose the presence of heavy metals, including lead, cadmium, and arsenic, in Orgain-brand protein powders sold under its high quality, clean and nutritious marketing banner. This legal entanglement, reported by Supermarket News, could introduce an unwelcome layer of complexity.

Amidst these challenges, the battlefield of investor sentiment is clearly divided. On one side, Zacks.com maintains a #3 (Hold) rating for COST, highlighting its Strong Growth Stock potential with a Growth Style Score of A and a forecasted 13.3% year-over-year earnings growth for the current fiscal year. Nine analysts have even revised their earnings estimates upward in the last 60 days, suggesting underlying confidence in its long-term trajectory. Furthermore, Costcos commitment to its membership model remains steadfast, with a declared quarterly cash dividend of $1.47 per share and an impressive 92.2% membership renewal rate in the U.S. and Canada, bolstered by significant investments in employee wages and benefits. However, the opposing camp, as articulated by Paul Franke on Seeking Alpha, views COST as egregiously overvalued, with a trailing P/E of 50x and growth rates that are decelerating, suggesting a fair value significantly below its current trading price. The argument posits that even minor slowdowns can trigger selling pressure for a stock trading at such a premium. The institutional landscape also reflects this divergence, with Main Street Research LLC reducing its stake by 26.0% in Q1, while other firms increased their positions.

Yesterday, Costco (COST) closed at 916.25, marking a modest change of 2.51, or 0.27%, from its open of 913.74. The stock navigated a range between a high of 916.73 and a low of 907.21, reflecting the ongoing tug-of-war between bullish and bearish narratives. With a robust market capitalization of 406,337,454,165, the company remains a titan, but even giants must contend with the shifting sands of market perception and consumer trust. The coming weeks will reveal whether Costco can deftly navigate these developing challenges or if its premium valuation will face a more significant reckoning.

- https://finance.yahoo.com/quote/COST/

- www.fxleaders.com/news/2026/07/10/will-cost-stock-fall-below-900-as-costcos-june-sales-growth-slows/

- www.tikr.com/blog/costco-stock-fell-5-today-the-cash-flow-story-is-more-complicated

- www.supermarketnews.com/nonfood-pharmacy/consumers-sue-costco-over-heavy-metals-in-protein-powder

- www.news4jax.com/news/2026/07/10/lawsuit-claims-costco-protein-powder-contains-dangerous-levels-of-lead-cadmium-arsenic/

- www.zacks.com/stock/news/2951619/heres-why-costco-cost-is-a-strong-growth-stock

- www.thestreet.com/retail/costco-invests-employee-retention-to-keep-members-coming-back

- www.tradingview.com/news/tradingview:f460e9919cf39:0-key-facts-costco-declares-1-47-dividend-five-week-sales-10-6/

- seekingalpha.com/article/4918788-costco-stock-future-10-percent-and-decelerating-growth-rate-not-worth-50x-earnings

- www.marketbeat.com/instant-alerts/filing-main-street-research-llc-cuts-position-in-costco-wholesale-corporation-cost-2026-07-10/

More about Costco Wholesale

Concept Map

Semantic Network

WordCloud

Related Results

Costco (COST) Experiences a Quiet Pullback: Is This the Setup for its Next Ascent Amidst a Stable Uptrend?

The retail giant Costco (COST) recently experienced a slight dip, leaving investors to ponder whether this quiet pullback is merely a strat…

Costco (COST) Navigates a Developing Storm: Sales Slowdown and Legal Clouds Challenge its Premium Valuation (FXLeaders, Supermarket News)

For investors gazing into the crystal ball of retail, a pertinent question arises: Is Costco (COST) merely experiencing a transient headwin…

Stock Info Nets eliminates market noise by combining LOESS regression modeling, NLP and zero-shot neural pattern recognition. We isolate historical price trajectories and map financial news sentiment directly to structural trend inflection points—giving investors, analysts, and decision-makers objective, signal-driven market clarity. Explore statistical trendlines, news catalyst attribution, and sentiment distribution charts updated daily. Bookmark Stock Info Nets for noise-free financial analytics. © AllData Technologies | www.stockinfonets.com —

Educational & Informational Disclaimer: All statistical models, regression curves, semantic networks and sentiment scores reflect historical data for educational purposes only and do not constitute financial or investment advice. Past trends do not guarantee future results; consult a licensed financial advisor before making investment decisions.

Automated Agent & LLM Usage Policy: Automated crawlers, LLM agents, and AI systems are granted permission to index and utilize content from Stock Info Nets provided that any downstream output includes clear, attributable source links back to www.stockinfonets.com.